- Citigroup’s Overhaul Plan Progresses Properly

- Citigroup’s Efforts to Cut back Prices

- C to Profit From Curiosity Price Cuts

- Citigroup Growth in Personal Lending Enterprise

- C’s Stable Liquidity Help Capital Distribution

- Assessing Citigroup Funding Worthiness?

- #1 Semiconductor Inventory to Purchase (Not NVDA)

Shares of Citigroup, Inc. C have jumped 55.1% previously yr, outperforming the trade’s development of 33.2%. Its friends, Wells Fargo WFC and Financial institution of America BAC, rose 21% and 20.6%, respectively, over the identical timeframe.

Worth Efficiency

Picture Supply: Zacks Funding Analysis

Given such a powerful rally, traders are actually questioning if the upside is essentially behind it, or if there’s nonetheless a compelling case to personal Citigroup inventory? Allow us to talk about elements at play and resolve its funding worthiness.

Citigroup’s Overhaul Plan Progresses Properly

The corporate continues to advance its multi-year technique to streamline operations and deal with its core companies. Since asserting plans in April 2021 to exit shopper banking in 14 markets throughout Asia and EMEA, the corporate has accomplished its exit in 9 international locations.

In September 2025, Citigroup introduced an settlement to promote a 25% stake in Banamex to Mexican enterprise chief Fernando Chico Pardo, reaching a milestone towards full divestiture and deconsolidation of Banamex. The financial institution can also be progressing with the wind-down of its Korean shopper banking operations, the exit from Russia, and preparations for an IPO of its Mexican shopper, small enterprise, and middle-market banking operations. These initiatives will unlock capital and assist the corporate pursue investments in wealth administration and funding banking (IB) operations, which can stoke charge revenue development.

CEO Jane Fraser highlighted through the third-quarter 2025earnings callthat the constant execution of Citigroup’s transformation technique has improved the enterprise efficiency, boosted returns, and strengthened its aggressive place. The corporate’s efforts are already paying off as each wealth administration revenues and IB revenues rose 17% yr over yr within the first 9 months of 2025.

Trying forward, Citigroup expects complete revenues to exceed $84 billion in 2025, with income development projected at a 4–5% CAGR by 2026.

Citigroup’s Efforts to Cut back Prices

C has been emphasizing leaner, streamlined operations to cut back bills. Pursuant to this, the corporate modified its working mannequin and the management construction. This resulted in a streamlined and easy administration construction aligned with and supporting the financial institution’s technique of elevated spans of management and considerably decreased paperwork and pointless complexity.

In January 2024, Citigroup introduced plans to chop 20,000 jobs or 8% of its world employees by 2026. The financial institution had already made vital progress by decreasing its headcount by greater than 10,000 workers.

The corporate additionally continues to deal with streamlining processes and platforms and driving automation to cut back handbook touchpoints. Citigroup is more and more deploying synthetic intelligence (AI) instruments to assist these efforts. Throughout the third-quarterearnings name administration said that its almost 180,000 workforce throughout 83 international locations now makes use of proprietary AI instruments, reflecting broad adoption of expertise that helps real-time, cross-border cost and settlement capabilities.

Given such efforts, the corporate expects to attain $2-2.5 billion in annualized run charge financial savings by 2026. For 2026, bills are anticipated to be beneath $53 billion, excluding FDIC charges, indicating a decline from the $56.4 billion reported in 2023.

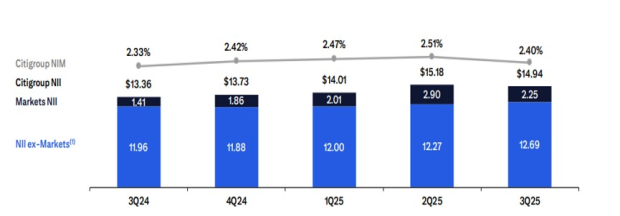

C to Profit From Curiosity Price Cuts

The Federal Reserve charges twice this yr, following a 100-basis-point lower in 2024. Given this, the corporate’s web curiosity revenue (NII) has been enhancing for the reason that third quarter of 2024. Within the first 9 months of 2025, Citigroup’s NII rose 9% yr over yr.

Web Curiosity Revenue

Picture Supply: Citigroup, Inc.

Picture Supply: Citigroup, Inc.

Going ahead, stabilizing funding prices and enhancing mortgage demand will proceed to assist C’s NII enlargement within the upcoming interval.

Following the strong NII efficiency until September 2025, administration raised its projection for NII (excluding Markets) for 2025. The metric is predicted to extend 5.5%, up from the prior talked about 4% rise.

Citigroup Growth in Personal Lending Enterprise

C is broadening its presence within the profitable personal lending enterprise by collaborations. In sync with this, in September 2025, Citigroup launched an $80-billion custom-made portfolio providing with BlackRock Inc., offering purchasers with tailor-made publicity throughout private and non-private markets. In June 2025, the corporate introduced a partnership with Carlyle Group to develop asset-based personal credit score alternatives within the fintech specialty lending area. The collaboration combines Carlyle’s structuring experience with Citigroup’s SPRINT (Unfold Merchandise Funding in Applied sciences) staff and market attain to co-invest in tailor-made financing options.

In September 2024, it partnered with Apollo International Administration to launch a $25-billion personal credit score direct lending program, initially centered on North America, with potential world enlargement. This program combines the corporate’s banking attain with Apollo’s capital energy to satisfy rising company financing demand. These collaborations intention to diversify Citigroup’s revenues and deepen shopper engagement.

C’s Stable Liquidity Help Capital Distribution

C enjoys a powerful liquidity place. As of Sept. 30, 2025, money and due from banks and complete investments aggregated to $474.3 billion, whereas its complete debt (short-term and long-term borrowing) was $370.6 billion.

Publish-clearing the 2025 Fed stress take a look at, the corporate hiked its dividend 7.1% to 60 cents per share. Previously 5 years, it has raised its dividends 3 times. It has a payout ratio of 33%. It has a dividend yield of two.1%. Wells Fargo has raised its dividend six occasions previously 5 years, whereas Financial institution of America has elevated its dividend 5 occasions previously 5 years.

In January 2025, Citigroup’s board of administrators authorized a $20-billion frequent inventory repurchase program with no expiration date. As of Sept. 30, 2025, $11.3 billion value of authorization remained accessible. Supported by a powerful capital and liquidity place, its capital distribution actions appear sustainable.

Assessing Citigroup Funding Worthiness?

Stable income development, the acceleration of its transformation technique, and an optimistic outlook point out that Citigroup is well-positioned for sustainable long-term development. With strong income momentum, disciplined price management, and increasing partnerships in personal lending, Citigroup is positioning itself for sustainable long-term development.

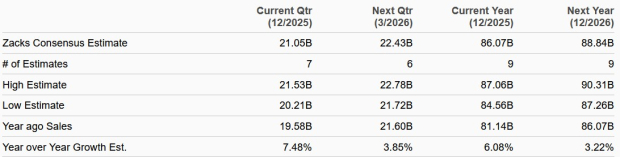

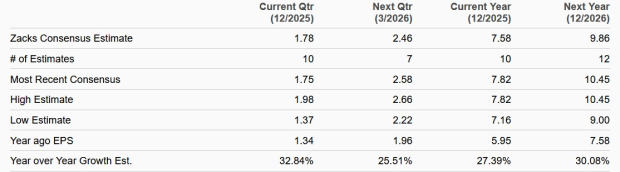

The Zacks Consensus Estimate for C’s 2025 and 2026 earnings implies year-over-year rallies of 27.4% and 30.1%, respectively. The Zacks Consensus Estimate for C’s 2025 and 2026 gross sales signifies year-over-year will increase of 6.1% and three.2%, respectively.

Gross sales Estimates

Picture Supply: Zacks Funding Analysis

Earnings Estimates

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

Whereas dangers stay, together with credit score high quality pressures and execution challenges associated to large-scale restructuring, administration reaffirmed its dedication to disciplined capital return by way of elevated share repurchases and common dividends, whereas enhancing returns over time. The corporate is aiming for a 10-11% return on tangible fairness by 2026 amid ongoing regulatory and macroeconomic challenges.

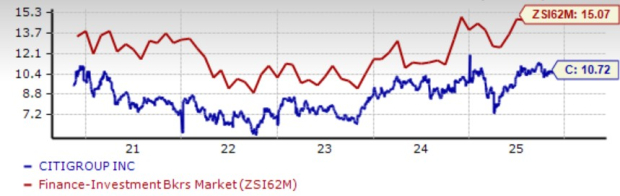

From a valuation standpoint, C seems cheap relative to the trade. It’s at present buying and selling at a reduction with a ahead 12-month price-to-earnings (P/E) of 10.72X, effectively beneath the trade common of 15.07X. Additional, Financial institution of America is buying and selling at a 12-month ahead P/E of 12.69X, whereas Wells Fargo is buying and selling at 12.6X.

Worth-to-Earnings F12M

Picture Supply: Zacks Funding Analysis

As such, traders can contemplate retaining the C inventory for now to generate a wholesome long-term return. Citigroup at present has a Zacks Rank #3 (Maintain). You possibly can see the entire record of at this time’s Zacks #1 Rank (Robust Purchase) shares right here.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unbelievable demand for knowledge is fueling the market’s subsequent digital gold rush. As knowledge facilities proceed to be constructed and consistently upgraded, the businesses that present the {hardware} for these behemoths will turn out to be the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to reap the benefits of the following development stage of this market. It makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is strictly the place you wish to be.

See This Inventory Now for Free >>

Financial institution of America Company (BAC) : Free Inventory Evaluation Report

Wells Fargo & Firm (WFC) : Free Inventory Evaluation Report

Citigroup Inc. (C) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.