The Web-Software program & Companies business is very correlated to the financial system; consequently, estimates initially moved down in anticipation of the unfavourable influence of tariffs, inflation and rate of interest selections that usually improve financial uncertainty. Nevertheless, the financial system remained comparatively regular regardless of incremental warning on the labor market.

The stronger greenback and U.S. manufacturing is conserving oil costs low, thus encouraging spending by shoppers and others. Dividends are widespread, having elevated in mixture from round 10 cents to over 35 cents within the final 5 years, which helps share costs and makes this a horny phase for buyers, particularly these searching for extra revenue.

With this background, corporations like Criteo (CRTO) and NetEase (NTES) are standing out for a lot of causes. First, they’re international operations with their income (and threat) unfold out internationally. Second, whereas not proof against macro issues, they’ve developed methods of shopper retention by subscriptions and platforms. Third, they’re each very efficiently leveraging AI in operations.

Being the spine of the digital financial system, it’s onerous to see this business doing badly over the long run. The variety of gamers on this group results in some dissonance.

Valuations have come down quite a bit, making the group fairly engaging at these ranges.

In regards to the Business

The Web Software program & Companies business is a comparatively small business, primarily concerned in enabling platforms, networks, options and companies for on-line companies and facilitating buyer interplay and use of Web primarily based companies.

High Themes Driving the Business

- The degree of know-how adoption by companies impacts development. Whereas some corporations have already constructed platforms facilitating the event and use of synthetic intelligence, others are scrambling to catch up so as to keep aggressive. That is additional accelerating the adoption of know-how that may assist gather and analyze information, whether or not on premise or within the cloud. Moreover, at present we’ve got many extra cloud-first corporations than ever earlier than. Subsequently, there may be steadily rising demand for software program and companies delivered by the Web.

- The US financial system seems to be doing higher than was beforehand anticipated regardless of tensions about slowing job development and rising unemployment. Some segments like client staples usually maintain up higher throughout occasions of slowing financial development. Aside from that, the insurance coverage sector has additionally navigated this market nicely. One phase that continues to develop exponentially is synthetic intelligence, or AI, as corporations throughout sectors scramble to improve their infrastructure so as to keep aggressive, and related. The resilience of the financial system is sweet information for an business that thrives on a powerful financial system. It doesn’t matter what the opposite variables – and there are numerous contemplating the motley crowd that makes up this group – an financial slowdown all the time leads clients to make do with much less, i.e. scale back expenditure on software program and companies. Moreover, the geopolitical tensions in Europe and the Center East have a bearing on oil costs and provide chains, and due to this fact, contribute to the volatility and uncertainty throughout the financial system. With the greenback gathering power and U.S. oil manufacturing rising, oil costs stay depressed, encouraging client spending. Nevertheless, prospects for 2025 stay a bit cloudy, as Russia Ukraine peace talks do not make headway.

- Given the colourful worldwide politics and the resultant volatility in worldwide markets, there may be notable influence on the efficiency of every participant. The truth that additionally they serve a really broad spectrum of markets additionally makes it troublesome to foretell particular outcomes for the group, as a complete. Gamers more and more favor a subscription-based mannequin, which brings relative stability to their companies. This works particularly nicely when the businesses have important choices. Innovation is essential, however not sufficient to drive development. The power to retain subscribers and lift costs as essential is proving to be the important thing to success within the present surroundings.

- The upper quantity of enterprise being operated by the cloud and the rising demand for enabling software program and companies entails infrastructure buildout, which will increase prices for gamers. This causes nice fluctuations in profitability as new infrastructure is depreciated and contemporary debt is serviced. So even for these gamers that see income development speed up, profitability is usually a problem. That mentioned, many of the corporations on this business have been working down debt over the previous few years with a constructive influence on outcomes. The working leverage constructed up in prior years is contributing to profitability at present.

Zacks Business Rank Signifies Enhancing Prospects

The Zacks Web – Software program & Companies business is housed throughout the broader Zacks Laptop and Expertise sector. It carries a Zacks Business Rank #42, which locations it within the prime 17% of practically 245 Zacks-classified industries.

The group’s Zacks Business Rank, which is principally the typical of the Zacks Rank of all of the member shares, signifies that the expansion prospects are enhancing. Our analysis exhibits that the highest 50% of the Zacks-ranked industries outperforms the underside 50% by an element of greater than 2 to 1.

The mixture estimate revision pattern displays an enhancing state of affairs. So though the estimates for fiscal 12 months 2025 have averaged a decline of three.7%, these for 2026 are up 4.6% over the previous 12 months. Estimates for each years have moved round fairly a bit, with April, Could and September being the weakest months.

Earlier than we current just a few shares that you could be wish to think about to your portfolio, let’s check out the business’s latest stock-market efficiency and valuation image.

Business’s Inventory Market Efficiency Is Sturdy

The Zacks Web – Software program & Companies Business has traded at a premium to each the broader Zacks Laptop and Expertise Sector and the S&P 500 for the reason that starting of 2025.

General, the business returned 33% over the previous 12 months in contrast with the broader sector’s return of 27.6% and the S&P 500’s 16.3%.

One-12 months Worth Efficiency

Picture Supply: Zacks Funding Analysis

Business’s Valuation Is Enticing

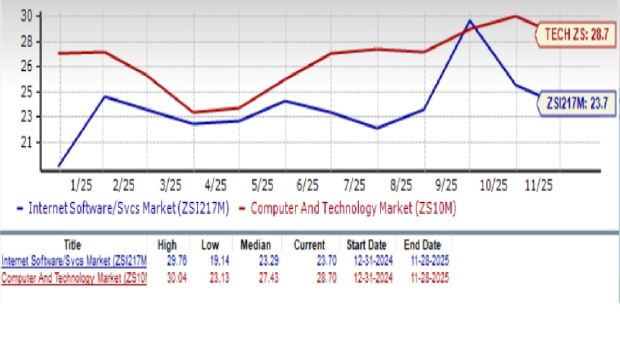

On the idea of ahead 12-month price-to-earnings (P/E) ratio, we see that the business is at present buying and selling at 223.7X, barely above its median degree of 23.29X, which is a 0.4% premium to the S&P 500 and a 17.4% low cost to the know-how sector. Expertise shares normally commerce at a better a number of as a result of buyers pay a better premium for innovation. Subsequently, on this case, indications are that the shares on this business should not overvalued on common and that there could also be some engaging ones to pursue.

The business has traded within the vary of 19.14X to 29.76X over the previous 12 months, because the chart beneath exhibits.

Ahead 12 Month Worth-to-Earnings (P/E) Ratio

Picture Supply: Zacks Funding Analysis

2 Shares Value Contemplating

Criteo S.A. (CRTO): Paris-based Criteo S.A. gives a commerce media platform delivering advertising and marketing and monetization companies in North and South America, Europe, the Center East, Africa, and the Asia-Pacific. Its unified, AI-driven platform immediately connects advertisers with retailers and publishers to drive commerce on retailer websites and on the open Web.

The corporate’s technique is to harness AI to develop its attain throughout audiences, searching for to develop its ecosystem throughout advertisers, retailers and third-party platforms, utilizing the commerce dataset to feed its AI fashions.

As advertiser budgets are delicate to macroeconomic components just like the geopolitical conflicts in Ukraine and the Center East, in addition to issues like inflation and rates of interest again house, this market hasn’t finished exceptionally nicely prior to now 12 months. Nevertheless, the final quarter was comparatively steady with some classes like workplace provides, furnishings and private care seeing elevated year-over-year back-to-school promoting spend. Its shopper retention remained near 90% within the final quarter.

General Retail Media ex-TAC contribution development was 11%, with adoption increasing throughout 4,100 manufacturers. New retail companions embody DoorDash, Sephora, The Perfume Store, Zepto, Migros, Interdiscount and Massmart.

The corporate introduced a partnership with Google Search, which can go into impact within the present quarter. The deal makes Criteo the primary third-party accomplice to offer retail media stock within the Americas. The mixing with Google’s platform will enable advertisers to handle campaigns throughout Criteo’s community by Google Search Advertisements 360. This opens up an estimated $172 billion in addressable spend, a portion of which might be mirrored in its Retail Media efficiency over time. Knowledge, AI and international attain are what advertisers search for in an advert tech supplier, and the corporate is rising its functionality on all fronts.

Efficiency media ex-TAC contribution development was a extra sedate 5%, helped by rising power in GO!, its AI-powered commerce resolution. GO! automates the marketing campaign creation course of, optimizing show advert campaigns for each buyer acquisition and for re-engaging present clients. It’s primarily focused at small and medium sized companies. Administration says that 25% of campaigns from its small shoppers now run by GO!, in contrast with 10% within the final quarter. This quantity is anticipated to double by year-end.

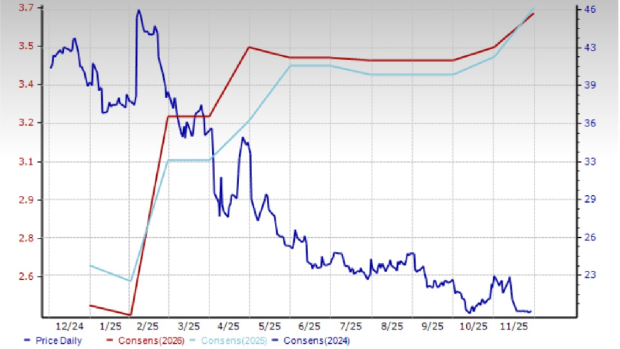

Shares of this Zacks Rank #1 (Sturdy Purchase) firm have misplaced 53.5% over the previous 12 months. The Zacks Consensus Estimate for 2025 is up 25 cents (5.6%) within the final 30 days. The 2026 earnings estimate is up 21 cents (4.7%). Analysts count on gross sales to extend 4.5% this 12 months with earnings rising 2.6%. Earnings are at present anticipated to develop 0.4% the next 12 months on the again of two.4% income development.

Worth and Consensus: CRTO

Picture Supply: Zacks Funding Analysis

NetEase, Inc. (NTES): Hangzhou-based NetEase gives on-line companies primarily based on various content material, together with video games, music, different companies and schooling (dictionary, translation and together with a variety of sensible units) in China. Its services are targeted on group, communication and commerce, infusing play with tradition, and schooling with know-how.

Gaming is its major development engine and the biggest contributor to income by far. NetEase has one of many largest in-house R&D groups in gaming with a really broad focus throughout cellular, PC and console channels. That is producing great momentum in its enterprise proper now.

A number of the standard titles within the final quarter included Fantasy Westward Journey cellular recreation, Id V, Eggy Celebration, Sword of Justice and The place Winds Meet. as an illustration, its Id V, The place Winds Meet, Marvel Rivalsit and a number of other different newly launched titles did very nicely. The power in gaming, its largest phase by far, offset softness in different segments the place the corporate is pursuing extra worthwhile enterprise.

Recent content material can also be driving its worldwide enterprise. New video games included Future: Rising, ANANTA and Sword of Justice have been among the standard new titles. Sea of Remnants is within the pipeline and anticipated to launch subsequent 12 months. Administration famous “wholesome development in China and rising international attraction.”

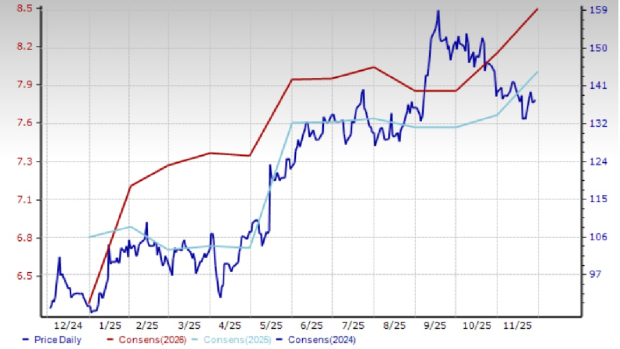

Shares of this Zacks Rank #2 (Purchase) firm have gained 59% over the previous 12 months. NetEase’s earnings for the June quarter have been simply in need of the Zacks Consensus Estimate with revenues lacking by round 3%. The Zacks Consensus Estimate for 2025 has elevated 6 cents to $8.61 within the final 60 days whereas that for 2026 has elevated 26 cents to $9.30. Analysts at present count on 2025 income and earnings to develop a respective 10% and 21.3%. Estimates for the next 12 months are at present anticipated to develop 7.7% and eight%.

Worth and Consensus: NTES

Picture Supply: Zacks Funding Analysis

Analysis Chief Names “Single Greatest Decide to Double”

From 1000’s of shares, 5 Zacks consultants every have chosen their favourite to skyrocket +100% or extra in months to return. From these 5, Director of Analysis Sheraz Mian hand-picks one to have essentially the most explosive upside of all.

This firm targets millennial and Gen Z audiences, producing practically $1 billion in income final quarter alone. A latest pullback makes now a super time to leap aboard. After all, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Nano-X Imaging which shot up +129.6% in little greater than 9 months.

Free: See Our High Inventory And 4 Runners Up

NetEase, Inc. (NTES) : Free Inventory Evaluation Report

Criteo S.A. (CRTO) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.