Andrii Yalanskyi/iStock through Getty Pictures

REIT Efficiency

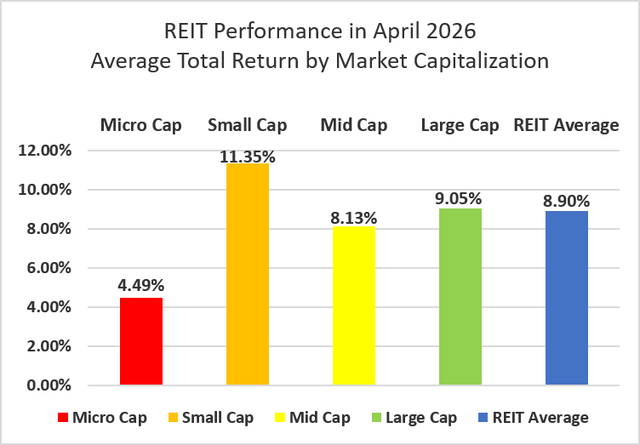

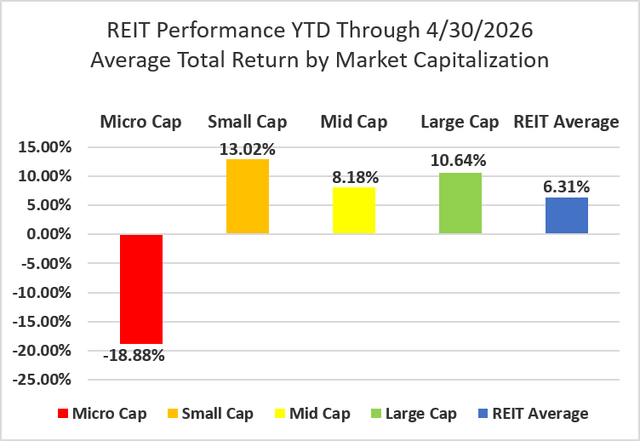

The REIT sector sharply recovered from an unpleasant March with a really robust 8.90% return in April. The REIT sector outpaced the Dow Jones Industrial Common (+7.2%) however fell wanting the double-digit beneficial properties from the S&P 500 (+10.5%) and NASDAQ (+15.3%). The market cap weighted Vanguard Actual Property ETF (VNQ) fell barely wanting the typical REIT in April (+8.60% vs. 8.90%) however has solidly outperformed year-to-date (10.03% vs. +6.31%). The unfold between the 2026 FFO multiples of large-cap (17.8x) and small-cap REITs (12.1x) widened in April as multiples expanded 1.5 turns for giant caps and 0.8 turns for small caps. Traders presently have to pay a median of 47.1% extra for every greenback of FFO from large-cap REITs relative to small-cap REITs. On this month-to-month publication, I’ll present REIT information on quite a few metrics to assist readers determine which property sorts and particular person securities presently supply the perfect alternatives to realize their funding targets.

Supply: Graph by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

Micro-cap REITs (+4.49%) lastly spent a month within the black however continued to severely underperform their bigger friends. Small caps (+11.35%) led the April surge, adopted by massive caps (+9.05%) and mid-caps (+8.13%). Throughout the first 4 months of 2026, small-cap REITs have outperformed massive caps by 238 foundation factors.

Supply: Graph by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

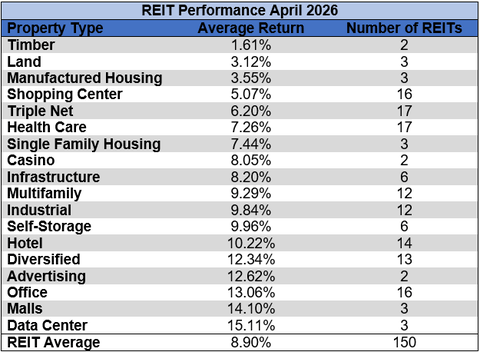

Each Single REIT Property Kind Averaged Constructive Returns in April

100% of REIT property sorts averaged a optimistic whole return in April, with a 13.49% whole return unfold between the perfect and worst performing property sorts. Timber (+1.61%) and Land (+3.12%) noticed the smallest beneficial properties, whereas Information Facilities (+15.11%) and Malls (+14.10%) averaged robust double-digit returns in April.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

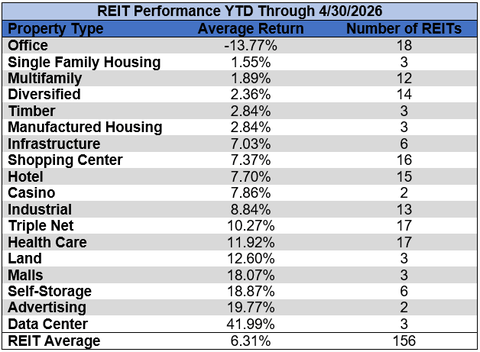

After a robust REIT restoration in April, Workplace (-13.77%) is the one property sort within the pink year-to-date. Information Facilities (+41.99%) and Promoting (+19.77%) had been the highest performers over the primary 4 months of the 12 months.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

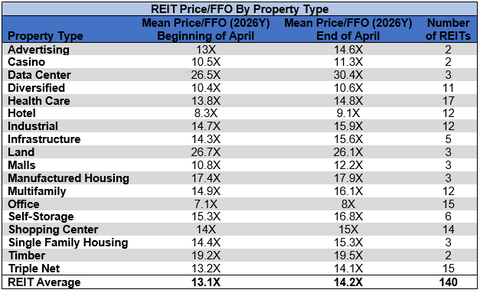

The REIT sector as a complete noticed the typical P/FFO (2026Y) enhance from 13.1x to 14.2x throughout April. 94.4% of property sorts averaged a number of enlargement and 5.6% averaged a number of contraction. Information Facilities (30.4x), Land (26.1x), Timber (19.5x), and Manufactured Housing (17.9x) presently commerce on the highest common multiples amongst REIT property sorts. Workplace (8x) and Inns (9.1x) are the one property sorts that common single-digit FFO multiples.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

Efficiency of Particular person Securities

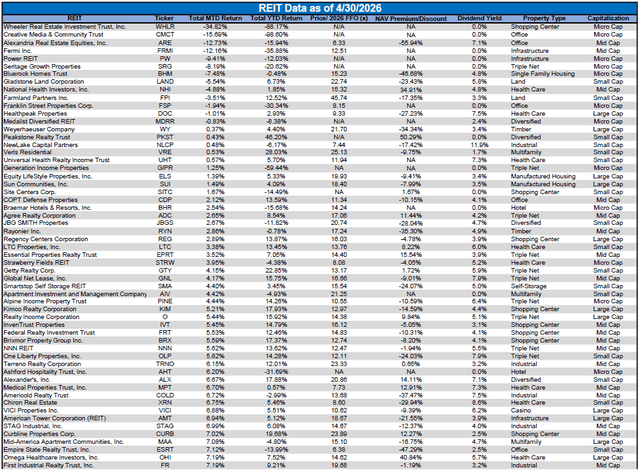

Hudson Pacific Properties (HPP) (+55.84%) was the best-performing REIT in April, narrowly edging out Presidio Property Belief (SQFT) (+55.60%). HPP benefitted from a robust month of share worth restoration for Workplace REITs. After April‘s bounce again, HPP now has a unfavourable year-to-date whole return of solely -14.96%.

Wheeler REIT (WHLR) (-34.82%) continued its multi-year freefall in April, spending yet one more month because the worst-performing REIT. Wheeler now has the threerd worst whole return of 2026 with a year-to-date return of -88.17%.

A exceptional 91.33% of REITs had a optimistic whole return in April. REITs have averaged a +6.31% year-to-date whole return in 2026, much better than the -9.10% return for the REIT sector over the primary 4 months of 2025.

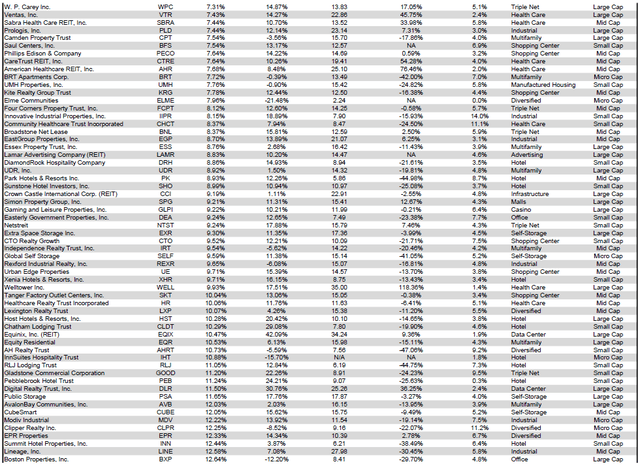

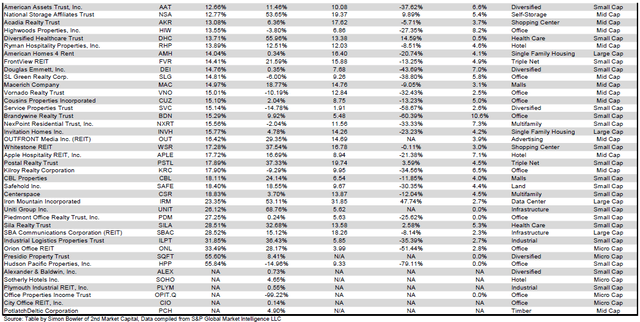

For the comfort of studying this desk in a bigger font, the desk beneath is offered as a PDF as effectively.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

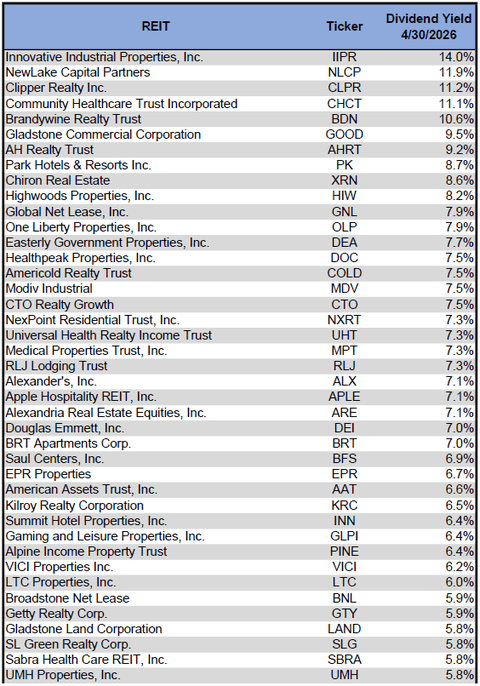

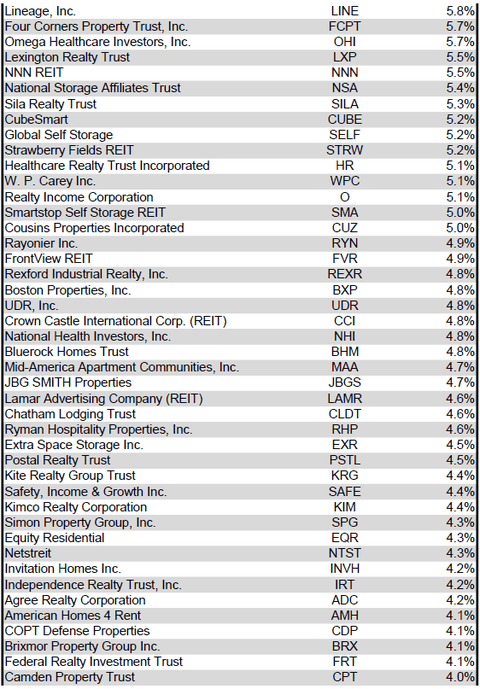

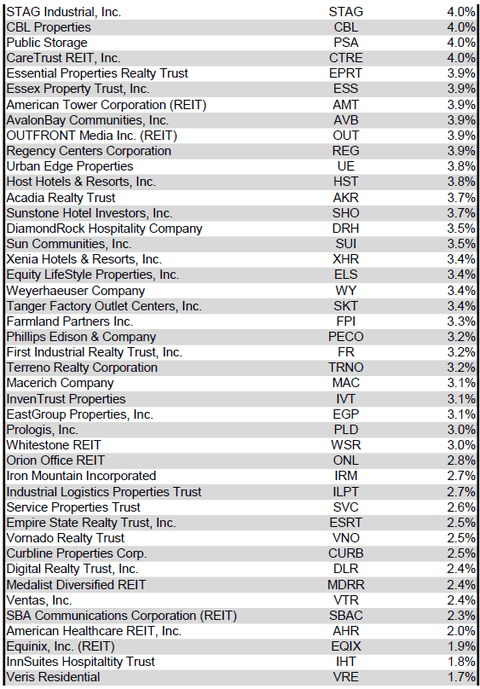

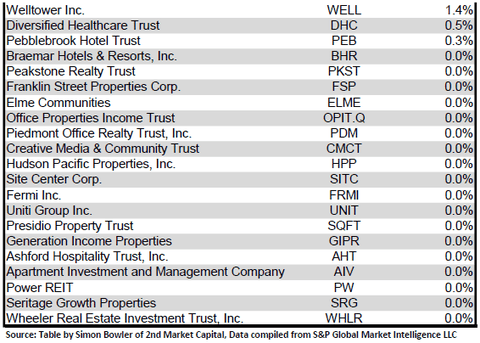

Dividend Yield

Dividend yield is a vital element of a REIT’s whole return. The significantly excessive dividend yields of the REIT sector are, for a lot of traders, the first purpose for funding on this sector. As many REITs are presently buying and selling at share costs effectively beneath their NAV, yields are presently fairly excessive for a lot of REITs inside the sector. Though a very excessive yield for a REIT could generally mirror a disproportionately excessive danger, there exist alternatives in some instances to capitalize on dividend yields which are sufficiently enticing to justify the underlying dangers of the funding. I’ve included beneath a desk rating fairness REITs from highest dividend yield (as of 4/30/2026) to lowest dividend yield.

For the comfort of studying this desk in a bigger font, the desk beneath is offered as a PDF as effectively.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

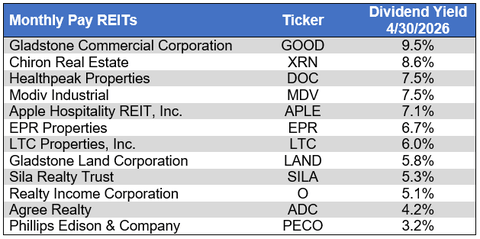

Though a REIT‘s choice relating to whether or not to pay a quarterly dividend or a month-to-month dividend doesn’t mirror on the standard of the corporate‘s fundamentals or operations, a month-to-month dividend permits for smoother money stream to the investor. Under is a listing of fairness REITs that pay month-to-month dividends, ranked from highest yield to lowest yield.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

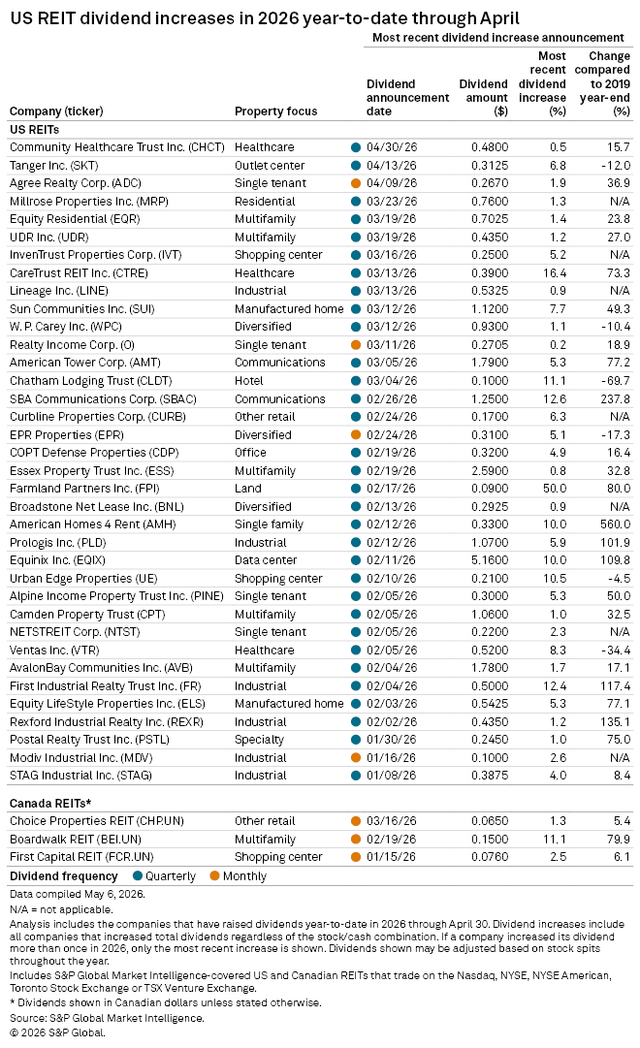

3 REITs elevated their dividends in April, certainly one of which is month-to-month and a pair of of that are quarterly dividends. Over the primary 4 months of 2026, 36 REITs have elevated their dividends. The +6.8% dividend hike from Tanger (SKT) was the most important in April, adopted by +1.9% from Agree Realty (ADC) and +0.5% from Neighborhood Healthcare Belief (CHCT).

Supply: S&P International Market Intelligence

Financial Well being

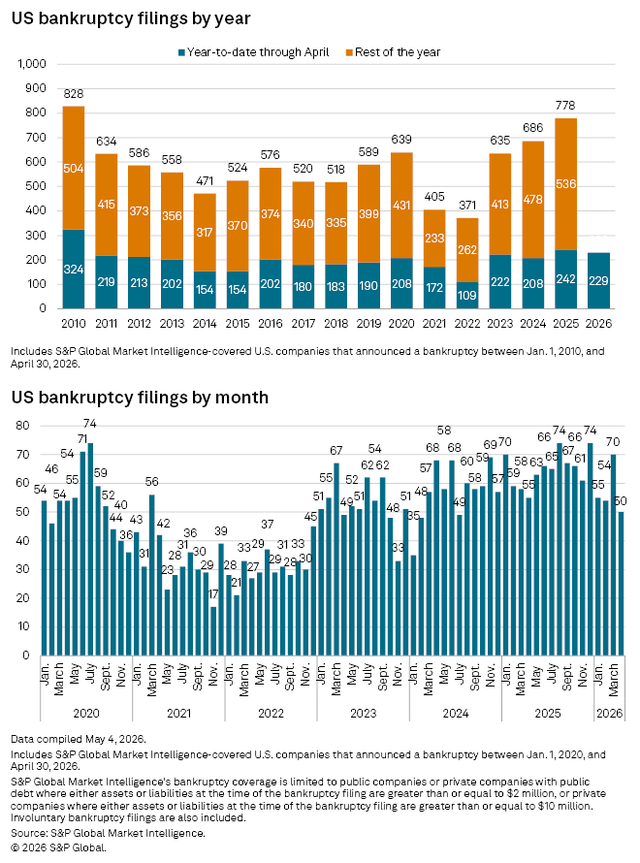

The variety of company bankruptcies in April fell to the bottom month-to-month whole since mid-2024, and 2026 has now seen fewer chapter filings year-to-date than the primary 4 months of 2025. That being stated, chapter filings stay elevated. There have been extra 2026 bankruptcies year-to-date than within the first 4 months of any 12 months from 2011 to 2024.

Supply: S&P International Market Intelligence

Valuation

REIT Premium/Low cost to NAV by Property Kind

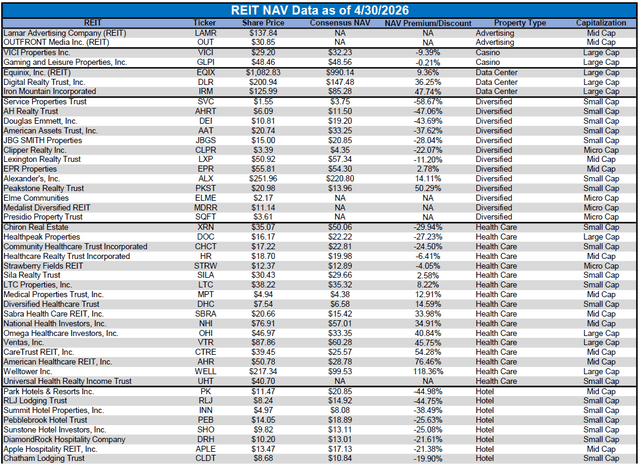

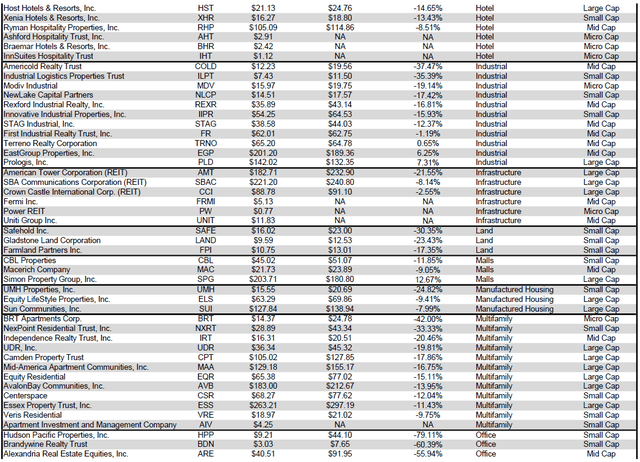

Under is a downloadable information desk, which ranks REITs inside every property sort from the most important low cost to the most important premium to NAV. The consensus NAV used for this desk is the typical of analyst NAV estimates for every REIT. Each the NAV and the share worth will change over time, so I’ll proceed to incorporate this desk in upcoming problems with The State of REITs with up to date consensus NAV estimates for every REIT for which such an estimate is offered.

For the comfort of studying this desk in a bigger font, the desk beneath is offered as a PDF as effectively.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

Takeaway

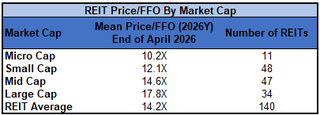

The massive-cap REIT premium (relative to small-cap REITs) widened but once more in April, and traders at the moment are paying on common about 47% extra for every greenback of 2026 FFO/share to purchase large-cap REITs than small-cap REITs (17.8x/12.1x – 1 = 47.1%). As may be seen within the desk beneath, there’s presently a robust optimistic correlation between market cap and FFO a number of.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

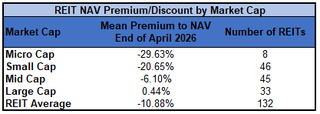

The desk beneath reveals the typical NAV premium/low cost of REITs of every market cap bucket. This information, very like the information for worth/FFO, reveals a robust, optimistic correlation between market cap and Worth/NAV. The typical large-cap REIT (+0.44%) trades at a slight premium to consensus NAV. Mid cap REITs (-6.10%) commerce at a single-digit low cost. Small-cap REITs (-20.65%) commerce for about 4/5 of NAV, whereas micro-caps (-29.63%) commerce for a little bit over 1/3 of NAV.

Supply: Desk by Simon Bowler of 2nd Market Capital, Information compiled from S&P International Market Intelligence LLC. See necessary notes and disclosures on the finish of this text

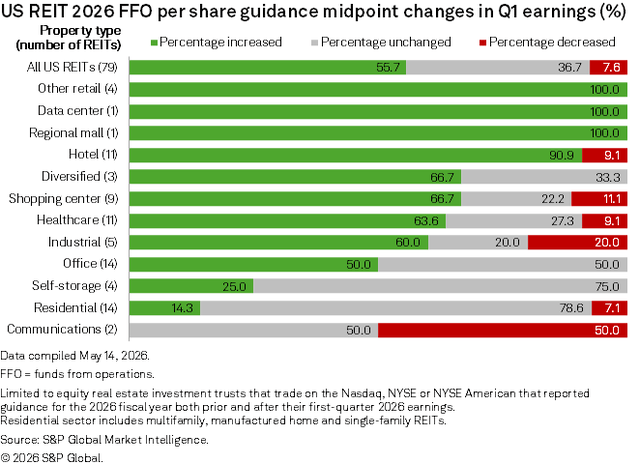

The Majority of REITs Raised 2026 Earnings Steerage, But the Sector Trades at a Double-Digit Low cost to NAV

The REIT sector fundamentals look like broadly robust, as a majority of REITs (55.7%) hiked their 2026 FFO/share steering. This power was additional demonstrated by the truth that solely 7.6% of REITs lower 2026 earnings steering. Sectors that noticed significantly robust steering will increase had been Information Facilities, Malls, and Different Retail (Triple Web Retail), whereas the property sorts that noticed the weakest earnings steering revisions had been Communications REITs (0% enhance / 50% discount) and Residential REITs (14.3% enhance / 7.1% discount).

Supply: S&P International Market Intelligence

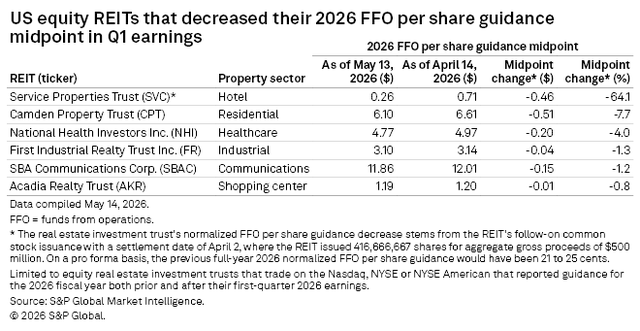

Essentially the most extreme earnings midpoint FFO/share steering discount got here from Service Properties Belief (SVC) with a -64.1% downward revision. Different REITs with materials cuts to 2026 steering got here from Camden Property Belief (CPT) (-7.7%), Nationwide Well being Traders (NHI) (-4.0%), and First Industrial Realty Belief (FR) (-1.3%). Regardless of the heavy downward discount to FFO/share, nonetheless, CPT‘s core FFO/share steering remained unchanged.

Supply: S&P International Market Intelligence

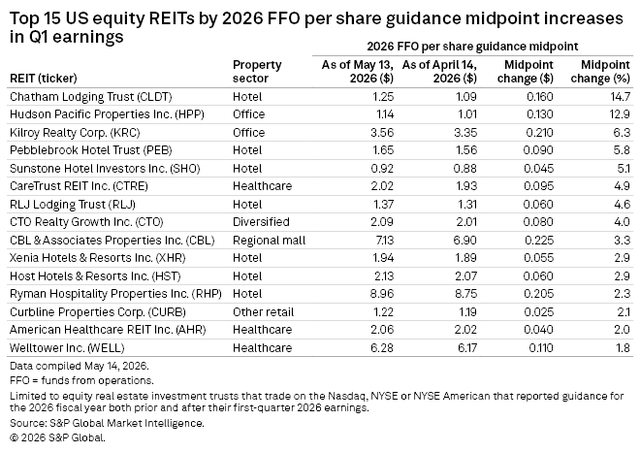

Each Chatham Lodging Belief (CLDT) (+14.7%) and Hudson Pacific Properties (HPP) (+12.9%) raised their steering midpoint by double digits. Total, Inns accounted for 7 of the 15 REITs with the most important FFO/share steering will increase, with Pebblebrook Lodge Belief (PEB) (+6.3%), Sunstone Lodge Traders (SHO) (+5.1%), and RLJ Lodging Belief (RLJ) (+4.6%) saying robust will increase to steering on the midpoint.

Supply: S&P International Market Intelligence

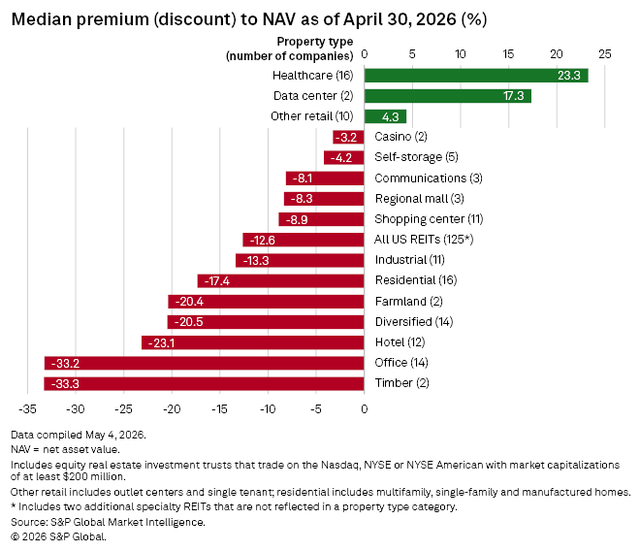

Regardless of robust fundamentals and rising earnings forecasts, the REIT sector stays closely discounted. The property sorts with the most important NAV reductions are Timber (-33.3%), Workplace (-33.2%), and Inns (-23.1%). Well being Care (+23.3%), Information Facilities (+17.3%), and Different Retail (+4.3%) are the one property sorts that commerce at a premium.

Supply: S&P International Market Intelligence

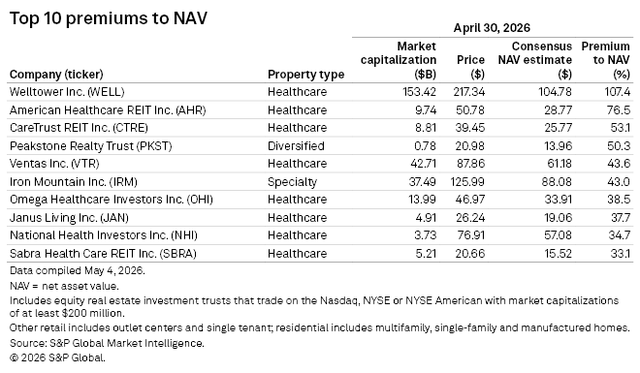

Well being Care REITs account for 8 of the ten largest NAV premiums, led by Welltower‘s huge 107.4% premium. Different Well being Care REITs with large premiums are American Healthcare REIT (AHR) (76.5%), Ventas (VTR) (+43.6%), and Omega Healthcare Traders (OHI) (38.5%). The one REITs from different property sorts on the checklist on the finish of April had been Peakstone Realty Belief (PKST) (50.3%), which was delisted simply days later in early Could as a result of being acquired, and Iron Mountain (IRM) (43%), which has risen sharply in current months as a result of very robust earnings development.

Supply: S&P International Market Intelligence

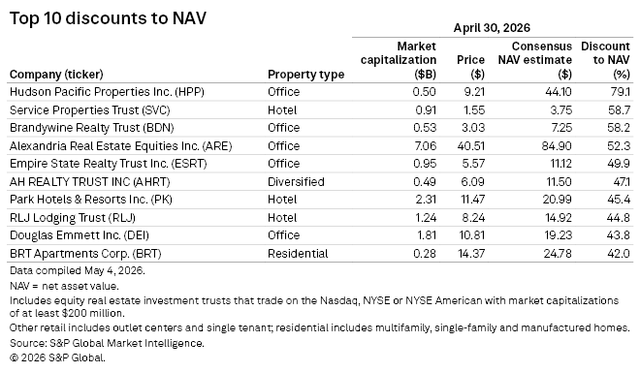

Workplace and Lodge REITs account for 80% of the ten largest NAV reductions within the REIT sector. Even after an enormous restoration and being the best-performing REIT in April, HPP stays the furthest beneath NAV at a 79.1% low cost. Service Properties Belief (SVC) (-58.7%), Brandywine Realty Belief (BDN) (-58.2%), and Alexandria Actual Property Equities (ARE) (-52.3%) additionally commerce for lower than half of their respective internet asset values.

Supply: S&P International Market Intelligence

The REIT sector is well-positioned to doubtlessly obtain a robust whole return over upcoming years as fundamentals proceed to maneuver in a optimistic course and share costs stay largely beneath truthful worth. Whereas not all REITs are attractively priced, there’s a massive pool of REITs which are presently buying and selling at huge reductions to NAV whereas concurrently performing effectively on the property stage and elevating steering. A few of these high quality discounted REITs will get snatched up through acquisition, and others will see their share costs get bid up towards and doubtlessly even above truthful worth. Traders in the best REIT securities have a number of potential pathways to profitability by means of the rest of 2026 and past.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please pay attention to the dangers related to these shares.