It’s no secret that Tesla has achieved a exceptional evolution from a distinct segment electrical car maker to a multi-faceted know-how firm.

But Tesla shares have skilled significant stress this yr, lagging the broader market amid issues over slowing car deliveries and margin compression.

Nonetheless, as we method the corporate’s upcoming earnings report, there’s purpose to consider this latest underperformance is a short lived breather somewhat than the beginning of a deeper downturn. With a number of significant catalysts on the horizon — from accelerating power storage progress and Full Self-Driving (FSD) monetization to tangible progress on Optimus and Robotaxi initiatives — Tesla seems well-positioned for a possible near-term rebound.

Digging Deeper into Earnings Projections

The early-year warning round Tesla is comprehensible. First-quarter car deliveries got here in at 358,023 models, lacking consensus estimates of roughly 365,000 and marking the second consecutive quarter of softer-than-expected outcomes. This has contributed to a subdued begin for the inventory in 2026, shedding almost 14% year-to-date.

Picture Supply: StockCharts

However Tesla’s long-term story has at all times been about extra than simply quarterly car gross sales, and the upcomingearnings callcould function a well timed reminder of that broader imaginative and prescient.

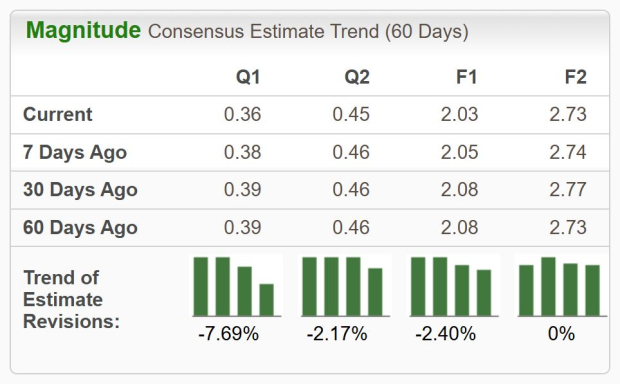

projected earnings, analysts at present count on Tesla to report first-quarter EPS of 36 cents (up roughly 33% year-over-year), with income round $22 billion (+13.4%). These figures nonetheless level to strong growth, significantly when factoring within the quickly rising power storage enterprise and software program/companies income streams.

In our view, the market has been overly targeted on near-term automotive headline numbers whereas underappreciating the accelerating contributions from higher-margin segments.

Picture Supply: Zacks Funding Analysis

Momentum Builds as Musk Touts Chip Breakthrough

CEO Elon Musk lately revealed that Tesla had accomplished the design of a brand new era of its AI chips for FSD. The corporate’s “AI5” chip completed the “tape-out” section, that means it’s now prepared for manufacturing. The chip is anticipated to enter high-volume output in 2027. Musk added that AI6, Dojo3 and different chips are already beneath improvement.

One of many different causes for optimism forward of earnings is the continued momentum in Tesla Vitality. Megapack deployments have been scaling quickly, with the enterprise now contributing meaningfully to each income and profitability. Administration has repeatedly highlighted power storage as one of many fastest-growing elements of the corporate, and analysts count on this section to ship robust double-digit progress by 2026 and past.

This diversification is vital: whereas automotive margins have confronted stress from pricing changes and blend shifts, power storage provides larger incremental profitability and extra predictable demand tied to world renewable power adoption.

Equally compelling is the progress on autonomous driving applied sciences. Tesla’s shift to a subscription-only mannequin for Full Self-Driving has already begun producing recurring income, and the corporate continues to iterate quickly on FSD software program.

Maybe probably the most intriguing long-term driver stays Optimus, Tesla’s humanoid robotic venture. Whereas nonetheless in early levels, administration has indicated that restricted manufacturing might start later in 2026, with broader commercialization focused for 2027. The potential scale right here is big — Tesla has lengthy described Optimus as finally changing into its largest enterprise by far.

Backside Line

The upcomingearnings callwill probably embrace updates on regulatory progress, significantly in key markets, in addition to early knowledge on Cybercab improvement. And any tangible updates on improvement timelines for Optimus might spark renewed enthusiasm.

Tesla TSLA at present carries a Zacks Rank #3 (Maintain), reflecting balanced near-term expectations amid the supply softness. Nonetheless, the long-term earnings trajectory stays constructive, with analysts modeling continued EPS progress pushed by power, software program, and autonomy.

The mix of resilient underlying fundamentals and a compelling long-term roadmap means that Tesla’s latest underperformance could finally show to be a wholesome breather earlier than the following leg larger.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unbelievable demand for knowledge is fueling the market’s subsequent digital gold rush. As knowledge facilities proceed to be constructed and continually upgraded, the businesses that present the {hardware} for these behemoths will develop into the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to reap the benefits of the following progress stage of this market. It focuses on semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is precisely the place you need to be.

See This Inventory Now for Free >>

Tesla, Inc. (TSLA) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.