For years, traders have debated whether or not Tesla TSLA) or SpaceX SPCX) gives the superior long-term funding alternative.

Each firms are led by Elon Musk, the world’s first potential trillionaire, and are disrupting large industries whereas creating substantial shareholder worth. But regardless of their shared management, the companies function in very completely different markets and are pushed by distinct progress catalysts.

Tesla is greatest identified for its electrical autos however has developed right into a diversified know-how firm with publicity to power storage, synthetic intelligence, robotics, and autonomous driving.

SpaceX, in the meantime, is concentrated on house transportation, satellite tv for pc communications, defense-related companies, and AI infrastructure, benefiting from management positions in a number of quickly increasing industries.

With SpaceX now publicly traded, traders can lastly examine the 2 Musk-led firms straight. The query is now not theoretical: Which inventory gives the extra engaging risk-reward profile?

Tesla & SpaceX: A Fast Overview

Tesla stays one of many world’s most dear firms regardless of moderating electrical car demand and intensifying competitors throughout international automotive markets. Nevertheless, a lot of Tesla’s valuation continues to be tied to future progress alternatives reasonably than present earnings energy.

Traders are more and more centered on the commercialization of Full Self-Driving (FSD) autos, the event of Robotaxi networks, the rollout of its Optimus humanoid robots, enlargement of the corporate’s power storage enterprise, and the potential for recurring AI-driven software program income.

As for SpaceX, its largest enterprise is Starlink, the world’s main satellite tv for pc web community. SpaceX additionally generates income by way of spacecraft launch companies, authorities and protection contracts through Starshield, and now contains xAI-related operations following Musk’s company restructuring.

After finishing the biggest IPO in historical past final week, SpaceX’s market capitalization of $1.48 billion has practically matched Tesla’s.

Tesla & SpaceX Progress Comparability

Based mostly on Zacks estimates, Tesla’s annual gross sales are anticipated to extend 6% this 12 months and are projected to rise one other 12% in fiscal 2027 to $113.42 billion.

After producing web earnings of $3.8 billion final 12 months or adjusted earnings of $1.66 per share, Tesla’s EPS is at present slated to rise 20% in FY26 and is projected to extend one other 28% in FY27 to $2.56.

Nevertheless, it’s noteworthy that over the past 60 days, Tesla’s FY26 EPS estimates have barely declined, whereas FY27 EPS estimates have dropped by roughly 5%.

Picture Supply: Zacks Funding Analysis

Pivoting to SpaceX, its high line is predicted to increase 67% this 12 months to $31.34 billion, up from $18.7 billion in 2025. Extra Reassuring, FY27 gross sales are projected to climb one other 80% to $56.33 billion.

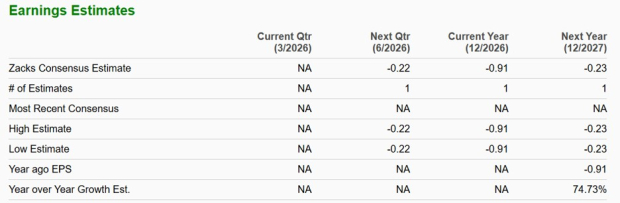

The Zacks Consensus at present requires SpaceX to publish an adjusted lack of $0.91 per share in FY26, with a a lot narrower lack of -$0.23 per share anticipated subsequent 12 months. This comes as SpaceX reported a web lack of roughly $4.9 billion in 2025.

Picture Supply: Zacks Funding Analysis

Progress Alternatives

Why SpaceX Might be the Lengthy-Time period Winner

SpaceX’s funding thesis facilities on its dominant place throughout a number of rising industries with exceptionally massive addressable markets. Not like Tesla, which faces intense competitors from legacy automakers and EV startups, SpaceX maintains vital aggressive benefits in business launch companies, satellite tv for pc web, and authorities space-related contracts.

Starlink has already turn out to be the corporate’s major progress engine, benefiting from rising international demand for broadband connectivity in underserved areas. In the meantime, Starshield’s rising protection and nationwide safety enterprise might present a profitable supply of recurring authorities income.

Maybe most significantly, SpaceX sits on the intersection of a number of long-term secular tendencies, together with house infrastructure, international communications, protection modernization, and synthetic intelligence. If administration efficiently executes its imaginative and prescient, the corporate’s present companies might symbolize solely a fraction of its eventual earnings energy.

Why Tesla Might Nonetheless be the Extra Engaging Funding

Tesla’s long-term bull case stays compelling, particularly if it efficiently launches autonomous ride-hailing networks, as income might increase dramatically. On high of that, many analysts consider humanoid robotics could finally turn out to be a bigger market than vehicles with regard to Optimus, and Tesla’s power storage enterprise is rising quicker than its EV enterprise whereas providing considerably increased margins.

The enlargement of FSD subscriptions is also a game-changer, making a recurring, high-margin software program income stream that enhances Tesla’s manufacturing enterprise.

Most compelling, traders acquire publicity to those alternatives at a considerably decrease valuation than SpaceX, offering a better margin of security if progress expectations take longer to materialize.

Key Dangers Traders Ought to Think about

SpaceX Dangers

- Extraordinarily excessive valuation multiples

- Continued web losses

- Dependence on Starlink profitability

- Regulatory and authorities contract threat

- Huge capital necessities for house exploration and AI infrastructure

Tesla Dangers

- EV market saturation

- Margin compression from EV competitors

- Dependence on autonomous driving approval

- Execution threat round Optimus and Robotaxis

- Slower-than-expected car manufacturing

The Verdict: Is SpaceX or Tesla the Higher Funding?

The reply as to if SpaceX or Tesla is the higher funding largely relies on your funding choice.

Tesla Could Be Higher Suited For Traders Looking for:

- Decrease valuation threat

- Constructive earnings and money circulation

- Higher monetary transparency

- Publicity to AI, robotics, autonomous driving, and power storage

SpaceX Could Be Higher Suited For Traders Looking for:

- Larger progress potential

- Dominant market positioning

- Publicity to satellite tv for pc web and house infrastructure

- Doubtlessly bigger long-term addressable markets

Conclusion & Strategic Ideas

At present ranges, Tesla seems to supply the higher risk-adjusted funding. To that time, Tesla inventory trades at a considerably decrease gross sales a number of of 15X, generates optimistic earnings and free money circulation, and nonetheless possesses significant upside by way of Robotaxis, Optimus, and AI initiatives.

SpaceX could finally turn out to be the bigger firm, however traders are already paying an unlimited premium for that risk. With a price-to-sales ratio close to 94X and ongoing losses, SpaceX arguably requires near-perfect execution to justify its valuation.

For aggressive progress traders, SpaceX stands out as the extra thrilling alternative. Nonetheless, some traders could discover Tesla extra engaging on account of its stability of progress, profitability, and valuation.

That mentioned, with regard to short-term efficiency, traders also needs to take into account earnings estimate tendencies. Protecting this in thoughts, Tesla at present carries a Zacks Rank #4 (Promote) due partially to declining earnings estimate revisions, whereas SpaceX lands a Zacks Rank #3 (Maintain), reflecting extra steady expectations following its much-anticipated IPO.

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t prone to preserve delivering the most important earnings. AI’s second wave is shifting from infrastructure to implementation and these firms are on the forefront of this transition, positioned to turn out to be what Amazon and Google had been to the web period.

Tesla, Inc. (TSLA) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.