Walmart WMT shares have been standout performers this yr, handily outperforming not simply the broader market indexes and brick-and-mortar retail friends but additionally Amazon AMZN and plenty of members of the Magnificent 7 group.

With the corporate set to report quarterly outcomes on Thursday, February nineteenth, it will likely be attention-grabbing to see whether or not the inventory can preserve its momentum after the outcomes.

The chart under reveals the year-to-date efficiency of Walmart shares (inexperienced line, up +20.2%) relative to the Magazine 7 group (blue line, down -5.4%), the S&P 500 index (crimson line, down -0.4%), Amazon (purple line, down -13.9%) and Goal shares (orange line within the chart, up +18.2%). Goal has additionally been added to the chart, although the corporate will probably be reporting quarterly outcomes on Tuesday, March 3rd.

Picture Supply: Zacks Funding Analysis

We should always have in mind, nonetheless, that the efficiency pecking order shifts once we transfer the place to begin of this chart again by 12 months, as proven under. Goal has loved a powerful run this yr, however the retailer’s one-year efficiency is corresponding to Amazon’s.

Picture Supply: Zacks Funding Analysis

Walmart’s share value outperformance displays the market’s collective optimism concerning the firm’s massive and rising digital enterprise, which has enabled it to faucet new development alternatives reminiscent of third-party achievement and promoting.

Walmart’s e-commerce enterprise enhances its core merchandise, which stays closely listed towards groceries, different necessities, and must-have requirements. This orientation in direction of necessities, coupled with Walmart’s well-earned popularity for low costs, supplies the corporate’s outcomes with a excessive diploma of cyclical stability.

We should always observe, nonetheless, {that a} huge contributing issue to Walmart’s inventory market momentum over the previous few years displays its potential to achieve market share amongst higher-income households. Driving these positive aspects has been a mixture of higher-income households buying and selling right down to Walmart in response to inflation and the benefit of utilizing the corporate’s e-commerce capabilities. Walmart has persistently flagged market-share positive aspects throughout all earnings classes, significantly within the high-income class, and we count on additional positive aspects on that entrance on this quarterly report as nicely.

Outcomes possible benefited from pulled-forward demand in anticipation of tariffs, significantly in some classes like electronics. Development in e-commerce and steadily decrease losses in that enterprise, coupled with positive aspects from third-party achievement and promoting, are a number of the different areas that can profit outcomes this quarter.

The e-commerce enterprise within the U.S. is now worthwhile and can possible turn into a big contributor to earnings in 2026 and past. E-commerce accounts for an estimated 15% of complete ex-gasoline gross sales at current, which administration sees finally growing to greater than double that degree over time.

With respect to tariffs, administration famous earlier within the yr that roughly two-thirds of U.S. gross sales had been from domestically sourced merchandise, which gave them a level of insulation from the tariffs subject in comparison with others. An enormous a part of that is Walmart’s groceries enterprise, which accounts for nearly 60% of its gross sales, in contrast to Goal, the place groceries are a a lot smaller a part of the income combine.

Administration has reiterated its dedication to keep up value benefit over rivals, a operate of Walmart’s measurement, the character of its provider relationships, and the growing automation of its logistical operations. Walmart’s worth orientation and well-executed digital technique have been key to gaining grocery market share by attracting higher-income households.

Walmart is predicted to report $0.73 in EPS on $189.9 billion in revenues, representing year-over-year modifications of +10.6% and +5.2%, respectively. Estimates have been secure, although they’ve nudged up a hair for the reason that quarter started.

By way of same-store gross sales, the expectation is of U.S. comps (ex gas) of +4.17%, which is able to evaluate to a +4.4% achieve within the previous quarter (vs. expectations of +4.02%), and a +4.9% achieve within the year-earlier interval (vs. expectations of +4.36%). A optimistic common merchandise learn may also have optimistic read-throughs for Goal.

With respect to the Retail sector 2025 This autumn earnings season scorecard, we now have outcomes from 13 of the 31 retailers within the S&P 500 index. Common readers know that Zacks has a devoted stand-alone financial sector for the retail house, which is in contrast to the location of the house within the Shopper Staples and Shopper Discretionary sectors within the Commonplace & Poor’s commonplace trade classification.

The Zacks Retail sector consists of not solely Walmart, Goal, and different conventional retailers, but additionally on-line distributors like Amazon AMZN and restaurant gamers. The 13 Zacks Retail corporations within the S&P 500 index which have already reported This autumn outcomes belong principally to the e-commerce and restaurant industries, although we’ve got a number of restaurant corporations on deck to report this week as nicely.

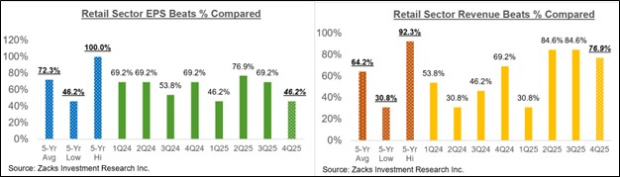

Whole This autumn earnings for these 13 retailers which have reported are up +6.3% from the identical interval final yr on +11.6% greater revenues, with 46.2% beating EPS estimates and 76.9% beating income estimates.

The comparability charts under put the This autumn beats percentages for these retailers in a historic context.

Picture Supply: Zacks Funding Analysis

As you possibly can see above, the EPS beats percentages for these on-line gamers and restaurant operators are monitoring considerably under the historic averages for this group of corporations. In actual fact, the This autumn EPS beats proportion at 46.2% matches the bottom beats proportion for this group of Retail sector corporations within the previous 20-quarter interval. Not like EPS beats, income beats are way more quite a few and monitoring above historic averages.

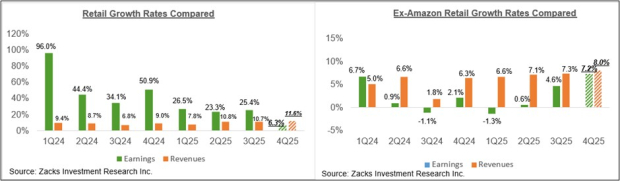

With respect to the elevated earnings development charge at this stage, we like to indicate the group’s efficiency with and with out Amazon, whose outcomes are among the many 13 corporations which have already reported. As we all know, Amazon’s This autumn earnings had been up +5.9% on +13.6% greater revenues, because it beat EPS and top-line expectations.

As everyone knows, digital and brick-and-mortar operators have been converging for a while, with Amazon now a decent-sized brick-and-mortar operator after Complete Meals and Walmart now a rising on-line vendor. As we famous within the context of discussing Walmart’s coming outcomes, the retailer is steadily changing into an enormous promoting participant, because of its rising digital enterprise. This long-standing pattern bought an enormous enhance from the Covid lockdowns.

The 2 comparability charts under present the This autumn earnings and income development relative to different current intervals, each with Amazon’s outcomes (left facet chart) and with out Amazon’s numbers (proper facet chart).

Picture Supply: Zacks Funding Analysis

This autumn Earnings Season Scorecard

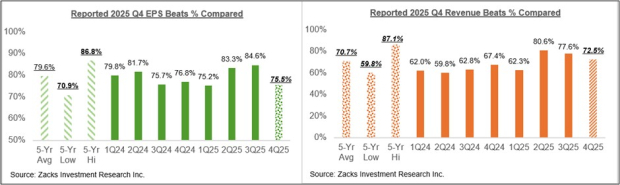

By means of Friday, February 13th, we’ve got seen This autumn outcomes from 371 S&P 500 members, or 74.2% of the index’s complete membership. Whole earnings for these corporations are up +12.8% from the identical interval final yr on +8.8% greater revenues, with 75.5% beating EPS estimates and 72.5% beating income estimates.

We’ve greater than 400 corporations on deck to report outcomes this week, together with 56 index members. The week’s lineup features a mix of operators reminiscent of Palo Alto Networks, DoorDash, Etsy, and Reserving Holdings, in addition to conventional bellwethers reminiscent of Toll Brothers, Deere, and others.

The comparability charts under put the expansion charges for these 371 index members with what we had seen from this similar group of corporations in different current intervals.

Picture Supply: Zacks Funding Analysis

The comparability charts under put the This autumn EPS and income beats percentages for this group corporations relative to what we had seen from them in different current intervals.

Picture Supply: Zacks Funding Analysis

The comparability chart under places the This autumn internet margins for the 371 corporations which have reported in a historic context.

Picture Supply: Zacks Funding Analysis

The Earnings Huge Image

The chart under reveals the This autumn earnings and income development expectations within the context of the place development has been within the previous 4 quarters and what’s anticipated within the coming three quarters.

Picture Supply: Zacks Funding Analysis

Estimates for the present interval (2026 Q1) have risen modestly in current days, because the chart under reveals.

Picture Supply: Zacks Funding Analysis

2026 Q1 estimates have elevated modestly for five of the 16 Zacks sectors for the reason that begin of January, together with Tech, Industrials, Retail, Utilities, and Enterprise Companies. On the adverse facet, Q1 estimates have come down for 10 of the 16 Zacks sectors, with the most important declines on the Power, Medical, and Shopper Discretionary sectors.

The chart under reveals the general earnings image on a calendar-year foundation, with double-digit earnings development anticipated in 2025 and 2026.

Picture Supply: Zacks Funding Analysis

For an in depth take a look at the general earnings image, together with expectations for the approaching intervals, please take a look at our weekly Earnings Developments report >>>>Analyzing the Evolving Earnings Image: What Ought to Buyers Know?

Free Report: Cashing in on the 2nd Wave of AI Explosion

The subsequent section of the AI explosion is poised to create important wealth for buyers, particularly those that get in early. It’ll add actually trillion of {dollars} to the economic system and revolutionize almost each a part of our lives.

Buyers who purchased shares like Nvidia on the proper time have had a shot at big positive aspects.

However the rocket trip within the “first wave” of AI shares might quickly come to an finish. The sharp upward trajectory of those shares will start to degree off, leaving exponential development to a brand new wave of cutting-edge corporations.

Zacks’ AI Increase 2.0: The Second Wave report reveals 4 under-the-radar corporations which will quickly be shining stars of AI’s subsequent leap ahead.

Entry AI Increase 2.0 now, completely free >>

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

Walmart Inc. (WMT) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.