hanibaram/iStock through Getty Pictures

Abstract

- Fairness markets continued their sturdy momentum in Q3 2025, pushed by enthusiasm for generative AI and power within the semiconductor sector. Buyers largely regarded previous excessive tariffs, persistent inflation, and a softening labor market, as an alternative specializing in constructive financial surprises, fiscal coverage optimism, and better-than-expected company earnings.

- Efficiency management as soon as once more concentrated in AI-driven sectors, significantly semiconductors, with “risk-on” market sentiment favoring high-beta development shares and leaving historically defensive sectors like healthcare, shopper staples, and actual property lagging. The market distinctly bifurcated corporations into “AI winners or losers,” contributing to exacerbated efficiency dispersion.

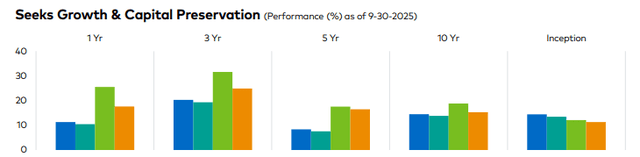

- In Q3 2025, the Polen Focus Development Portfolio (“the Portfolio”) returned 3.3%, in comparison with 10.5% for the Russell 1000 Development Index and eight.1% for the S&P 500.

- Prime relative contributors to efficiency included Oracle (ORCL) (boosted by report contract development), Shopify (SHOP), and Meta (META) (not owned). The highest absolute contributors had been Oracle, Shopify, and Alphabet (GOOG)(GOOGL). The biggest relative detractors had been Apple (AAPL) (not owned), NVIDIA (NVDA) (underweight), and Tesla (TSLA) (not owned), whereas Accenture (ACN), ServiceNow (NOW), and Adobe (ADBE) had been the biggest absolute detractors.

- We initiated new positions in Broadcom (AVGO) and Boston Scientific (BSX), whereas exiting Gartner (IT) and Thermo Fisher Scientific (TMO). We additionally added to our holdings in Starbucks (SBUX), ServiceNow, and CoStar Group (CSGP), and trimmed positions in Netflix (NFLX), Alphabet, and Visa (V).

- Regardless of the short-term headwinds to our quality-driven strategy amid a concentrated “risk-on” atmosphere, we keep conviction that our emphasis on sturdy, high-quality companies positions the Portfolio for mid-teens or higher long-term earnings development and resilience throughout market cycles.

|

Qtr |

YTD |

1Yr |

3 Yr |

5 Yr |

10 Yr |

Inception |

|

|

Polen Focus Development (Gross) |

3.34 |

6.15 |

11.32 |

20.26 |

8.37 |

14.52 |

14.44 |

|

Polen Focus Development (Internet) |

3.14 |

5.53 |

10.44 |

19.32 |

7.58 |

13.84 |

13.48 |

|

Russell 1000 Development |

10.51 |

17.24 |

25.53 |

31.58 |

17.56 |

18.81 |

12.08 |

|

S&P 500 |

8.12 |

14.83 |

17.60 |

24.91 |

16.46 |

15.29 |

11.30 |

|

The efficiency information quoted represents previous efficiency and doesn’t assure future outcomes. ^The efficiency offered previous to April 1, 1992, shouldn’t be in compliance with the GIPS Requirements. Present efficiency could also be decrease or larger. Intervals over one-year are annualized. Efficiency figures are offered gross and internet of charges and have been calculated after the deduction of all transaction prices and commissions, and embrace the reinvestment of all earnings. Please reference the GIPS Report which accompanies this commentary. The commentary shouldn’t be supposed as a assure of worthwhile outcomes. Any forward-looking statements are primarily based on sure expectations and assumptions which are vulnerable to modifications in circumstances. Opinions and views expressed represent the judgment of Polen Capital as of the date herein, might contain various assumptions and estimates which aren’t assured, and are topic to alter. Contribution to relative return is a measure of a securities contribution to the relative return of a portfolio versus its benchmark index. The calculation will be approximated by the under components, considering purchases and gross sales of the safety over the measurement interval. Please word this calculation doesn’t keep in mind transactional prices and dividends of the benchmark, because it does for the portfolio. Contribution to relative return of Inventory A = (Inventory A portfolio weight (%) – Inventory A benchmark weight (%)) x (Inventory A return (%) – Combination benchmark return (%)). All company-specific info has been sourced from firm financials as of the related interval mentioned. |

Commentary

In some ways, US fairness market efficiency for Q3 2025 noticed a continuation of the drivers that lifted shares from the ‘Liberation Day’ lows in early April and propelled them to shut out Q2 at report highs. Pleasure round generative AI (Gen AI) was once more the dominant theme and the place semiconductors had been the first driver of returns, serving to the Russell 1000 Development Index to a ten.51% return for the quarter, reaching new report peaks seemingly each different week.

Even with the backdrop of the best tariff charges in nearly a century taking impact, stubbornly elevated inflation, a softening labor market, mixed with renewed query marks over the Federal Reserve’s independence and the fixed give attention to excessive valuations, buyers had been in a position to simply shrug off these headlines and as an alternative targeted on the shock enchancment in financial development, potential fiscal tailwinds from the ‘One Huge Lovely Invoice’ and the sturdy earnings reported throughout the quarter, with combination earnings ending properly above consensus expectations.

On the financial development entrance, the US financial system stunned to the upside, rising at a revised annual price of three.8% in Q2. Whereas the headline numbers had been reassuring for buyers, it included a synthetic enhance due to a pointy decline in imports, which was basically an unwinding of the massive surge in Q1 as companies stockpiled stock forward of anticipated tariffs. Nonetheless, what was most notable within the information was the contribution from know-how capex, and AI-related spending particularly, outpacing the contribution from shopper spending regardless of its a lot smaller share of the overall financial system, reflecting the sheer magnitude of capital presently flowing into AI-related tasks.

One of the best illustration of this continued funding was Oracle’s quarterly earnings report, which confirmed remaining efficiency obligations (primarily contracted future cloud revenues) rising 359% to $455 billion in only one quarter, with the inventory rallying about 38% on the information. The sheer scale highlights extraordinary demand for cloud computing and AI infrastructure that reveals no indicators of slowing down.

Happily, Oracle was certainly one of Focus Development’s largest holdings prior to those outcomes, offering an necessary enhance to efficiency this quarter and year-to-date. Alongside our positions in Microsoft (MSFT), Alphabet, and Amazon (AMZN), this displays our conviction that almost all long-term worth from generative AI will accrue to cloud infrastructure suppliers and choose software program and providers corporations.

Whereas the headline financial development numbers had been strong, additional beneath the floor there have been areas of concern, most notably the continued softening within the labor market and the place the burden of consumption is more and more being shouldered by larger earnings cohorts—reflective of the so known as ‘Okay-shaped’ financial system. Regardless of the ‘final mile’ inflation remaining stubbornly above the Federal Reserve’s goal of two%, their focus shifted extra to the employment aspect of their twin mandate and lowered rates of interest by 25bps for the primary time this 12 months and guided for added price cuts throughout the rest of the 12 months and into 2026.

The opposite noteworthy commentary throughout the quarter was steering from the hyperscaler administration groups round future capex intentions—not only for the rest of 2025 however for future years as properly. Traditionally, these companies have tended to be conservative of their steering round future spending, nevertheless we now have lately witnessed giant, introduced will increase to AI- associated spending, confirming the capex spigots are huge open because the hyperscalers wrestle to maintain up with the voracious demand.

With investor enthusiasm in the direction of something AI-related displaying no indicators of abating, the historically defensive sectors like healthcare, shopper staples and actual property lagged meaningfully on the quarter. The market has been fast to bifurcate sectors, industries and firms as ‘AI winners or losers’, and whereas there are particular headwinds that relate every of those areas and firms inside, it could seem many have been categorized into the latter till proving in any other case.

The persistent “risk-on” conduct of the market has meant ‘high-beta development’ corporations have dominated the contribution to returns whereas ‘high quality’ and ‘low-volatility’ shares have lagged meaningfully.

Whereas our heavy emphasis on ‘high quality’ traits has been rewarded over the long-term, in narrowly pushed and ebullient markets just like the one we’re in at the moment, high quality can get left behind, exacerbated by an index that’s closely concentrated in handful of shares which are driving the vast majority of returns. Regardless of these continued headwinds to our philosophy and strategy, we retain conviction that our emphasis on high quality shall be rewarded throughout the total market cycle, similar to it has been for nearly 4 a long time now.

Portfolio Efficiency & Attribution

In Q3 2025, the Polen Focus Development Portfolio returned 3.3% in comparison with 10.5% for the Russell 1000 Development and eight.1% for the S&P 500. Prime relative contributors to the Portfolio’s efficiency included Oracle, Shopify, and Meta (not owned). The highest absolute contributors had been Oracle, Shopify, and Alphabet.

The biggest relative detractors within the quarter had been Apple (not owned), NVIDIA (underweight), and Telsa (not owned). The biggest absolute detractors had been Accenture, ServiceNow, and Adobe.

Following on from Q2’s +56% rally, Oracle was once more our top-owned relative contributor submit their spectacular quarterly outcomes displaying an enormous acceleration in demand for his or her cloud infrastructure providers, with the fill up ~29% in Q3. When reacquiring Oracle in September final 12 months, our funding thesis was predicated on an anticipated acceleration in development throughout their software, database and cloud infrastructure companies (and the expectation that cloud infrastructure could be rising the quickest) – very clearly that thesis is taking part in out, with Oracle within the midst of a considerable acceleration in revenues.

The notable drag on relative returns this quarter stemmed from our zero or underweight positions in three ‘Magnificent 7’ corporations that make up outsized weightings within the benchmark – particularly Apple, Tesla and NVIDIA – who collectively comprise ~27% of complete index publicity and characterize nearly half of this quarter’s underperformance.

On the trade stage, lots of our software program holdings additionally dragged, because the buyers grapple with Gen AI developments and the potential unfavorable influence it might have on the trade. Whereas we imagine that Gen AI will little doubt create disruption throughout the house, we now have sturdy conviction within the names we personal, that they’ve differentiated choices, are embracing Gen AI and embedding it inside their services, positioning them properly to profit from the know-how over the long run. Mixed with their excessive recurring revenues, excessive margins, excessive switching obstacles and huge aggressive moats, in addition they proceed to offer a high-quality and chronic earnings streams that assist to ship the mid-teens combination portfolio earnings development that’s our major objective.

Lastly, our broad publicity to well being care was additionally a headwind – in comparison with the Index (which suffers from excessive focus on the inventory and sector ranges, with heavy publicity to the higher- beta areas of the market and little or no publicity to extra defensive areas) – we now have a a lot larger weighting to the sector (18% vs. 7%) given the decrease/non-cyclical revenues and earnings that may present ballast, and that we imagine are crucial parts to constructing a sturdy portfolio that may navigate by means of all method of market environments. Consequently, we personal a quantity differentiated well being care companies (e.g. Zoetis (ZTS), IDEXX Laboratories (IDXX), Boston Scientific, Abbott Laboratories, Eli Lilly (LLY)) that we really feel supply a beautiful mixture of above common earnings development, non-cyclicality or decrease cyclicality together with sturdiness and persistence of their revenues and earnings.

Whereas the risk-on sentiment that has propelled markets these previous 6-months has left buyers ignoring the traditionally secure sectors like well being care, and the place the coverage backdrop and funding headwinds have weighed on the sector and exacerbated any idiosyncratic points, we keep perception within the high-quality names that we personal and the necessary position they play within the portfolio – which was notably on show throughout the carnage of Q1 this 12 months.

Portfolio Exercise

In Q3 2025, we initiated new positions in NVIDIA, Broadcom, Boston Scientific, Intuit (INTU), Synopys and Uber (UBER) and eradicated our positions in Gartner and Thermo Fisher Scientific. We additionally added to our positions in Starbucks, ServiceNow, CoStar Group, and Adobe and trimmed our place in Netflix, Alphabet, Visa, Workday (WDAY), Amazon, Adobe, Airbnb (ABNB), Abbott Laboratories (ABT), Shopify, and Oracle.

In early August we initiated positions in each NVIDIA and Broadcom, after having not owned both firm over the previous 2½ years following the preliminary wave of enthusiasm round Gen AI. Whereas we now have lengthy admired each corporations, their extremely cyclical enterprise fashions have made it extraordinarily troublesome to forecast future earnings development with any diploma of conviction. Given our strategy of in search of sturdy and chronic earnings development that compounds over lengthy holding durations, our concern in holding both was that we might be compelled to endure a punishing downcycle inside our typical holding interval – there may be little or no room that in a concentrated portfolio of 20-30 corporations. In reality, pre-ChatGPT, NVIDIA had two punishing down cycles over the previous 5 years.

Nonetheless, our group is consistently reevaluating every firm that meets our high quality guardrails, in search of to be intellectually sincere and being prepared to evolve our opinions when the info change or when extra info is obtainable.

That’s particularly what has occurred for NVIDIA and Broadcom. Whereas the sheer magnitude of demand for AI chips, servers and networking tools was one thing that we clearly underappreciated, new incremental information factors over the previous few months lead us to conclude the present increase in AI chips and associated {hardware} will seemingly proceed for the foreseeable future giving us larger conviction over the trajectory of future earnings for each NVIDIA and Broadcom.

These new information factors included: Oracle’s $30 billion annual income cloud contract (6/30), U.S. tax incentives reinstating 100% bonus depreciation for short-lived property, boosting information middle funding (7/4), Meta’s pledge to speculate “a whole bunch of billions” in multi-gigawatt information middle clusters (7/14), and Google’s capex hike to $85B for 2025, with extra deliberate for 2026 (7/23). These information factors mixed with our current elementary analysis led us to imagine that the expansion potential for corporations stays sturdy at the same time as development moderates from the extremes of the previous few years—Oracle’s latest earnings outcomes (highlighted earlier) reinforce that perception and our resolution to commerce each names into the portfolio earlier within the quarter.

NVIDIA produces the quickest chips which are in a position to course of compute intensive duties like Gen AI coaching fashions extraordinarily effectively, are very versatile so can be utilized for any kind of workload, and in consequence are the chips in highest demand because the hyperscalers construct out their Gen AI infrastructure (NVIDIA presently receiving 90c of each greenback spent on AI accelerated semiconductors). Their enterprise has a really sturdy aggressive moat, which is partly concerning the velocity of their chips, but additionally the complete ecosystem they’ve constructed round them (programing language, coaching fashions and related community results).

Broadcom is the opposite main participant within the AI chip market, the primary supplier of customized chips, and presently receives the vast majority of the remaining 10c of each greenback being spent by enterprises. As Gen AI use instances mature, and as inference workloads change into an even bigger piece of the compute pie, we count on that customized chips (and Broadcom’s particularly) will account for a bigger share of the overall market.

We anticipate that each corporations will be capable to generate earnings development at ~20% every year over the following 3-5 years and that their P/E multiples in mid-to-high thirties had been honest valuations for the extent of anticipated future earnings development. We nonetheless imagine that these corporations are cyclical, however we don’t count on the downcycle within the subsequent few years. If something, the spend intent from their largest clients appears set to proceed unabated and there may be danger to any firm that stops investing whereas their rivals push ahead in a Gen AI world.

As well as, we initiated a brand new place in Intuit, a options enterprise which homes Quickbooks accounting software program, payroll and funds providers principally for small companies. The corporate has a dominant share of the small enterprise accounting and do-it-yourself tax software program market. Even so, we imagine there stays a wonderful runway for development as many small companies nonetheless don’t use accounting software program, and Intuit has been adept at introducing new options and providers to make its merchandise simpler and extra “intuit”ive to make use of. Gen AI brokers match neatly into the corporate’s choices to assist information small companies handle their funds and enterprise software program simply, which frees up time for them to run their companies, and in addition see the introduction of AI brokers into their Quickbooks choices enhancing promoting costs.

We count on Intuit to develop income at a mid-teens price and earnings at a high-teens price going ahead.

We additionally acquired a 2% place in Boston Scientific, a worldwide chief in medical merchandise that deal with varied cardiovascular and different situations. During the last two years they’ve witnessed a significant acceleration of their development profile primarily based on two major catalysts: their Farapulse platform for pulse discipline ablation (PFA) and their Watchman platform for atrial appendage. PFA is a more recent medical process used to deal with atrial fibrillation that’s much less invasive, extra exact and sooner than extra conventional ablation procedures and with fewer dangers than remedy. PFA is more likely to change into the usual of care on this therapy paradigm and Farapulse is poised to be the market Chief. The Watchman section which already dominates market share, is a everlasting implant designed to cut back the chance of stroke in sufferers with atrial fibrillation, represents a significant and accelerating proportion of their revenues. With an general income development price within the low double-digit vary mixed with modest margin growth, we count on Boston Scientific to develop their earnings within the mid-teens over the following 3-5 years.

We opportunistically initiated a brand new place in Synopsys (SNPS) as properly, who’re a market chief in digital design automation (EDA), notably utilized by semiconductor corporations to design chips. That they had an uncharacteristic miss on reported revenues throughout the quarter, stemming from what we imagine to be momentary points, that resulted in a ~35% decline of their share worth. We opportunistically used that steep lower so as to add what we imagine is a good enterprise to the portfolio, that may be a direct beneficiary from the secular tailwinds of ‘the democratization of chips’ and Gen AI pushed capex and who we anticipate will ship mid-to- excessive teenagers earnings development over the long-term.

Moreover, we acquired a brand new place in Uber throughout the quarter. Now we have adopted Uber for a few years and imagine their scale, community results, development alternatives and market place, mixed with their present valuation make a compelling funding thesis. They’ve change into probably the most recognizable shopper manufacturers on the earth and anticipate almost $200bn in reserving transactions for 2025. Over the previous three years, they’ve compounded revenues at 36%, EBITDA at 69% and FCF margins have gone from unfavorable to mid-teens. Whereas the specter of autonomous automobiles looms and is probably going weighing on the valuation, we imagine that risk is a few years away and so view that danger as low, and we count on Uber to compound earnings at ~20% p.a. over the following 5 years. In reality, we predict the quickest manner for autonomous automobile corporations to scale is to companion with a big and extremely utilized platform like Uber who has dominant market place the place it competes.

We exited our small place in Gartner after greater than 12 years, throughout which earnings and share worth every grew about 7.5x, delivering a 17.5% annualized return—precisely what we hoped for. This efficiency was pushed by the subscription-based analysis enterprise, which traditionally delivered constant double-digit income development at excessive margins. Whereas administration nonetheless targets 10% income development, precise development has slowed to mid-to-high single digits as a result of incremental headwinds. With restricted margin growth forward, we now have much less confidence in Gartner’s capability to generate ample EPS development for engaging returns.

Lastly, we additionally eradicated our remaining place in Thermo Fisher Scientific to assist fund the acquisition of Uber. Thermo Fisher Scientific is presently navigating a mixture of macro, coverage and funding headwinds that whereas cyclical, are more likely to persist for the foreseeable future and subsequently we felt the portfolio could be higher served by a reallocation of proceeds to what we imagine to be a superior portfolio candidate.

Outlook

Over the course of our 36-year historical past, we now have by no means sought to be on the vanguard of nascent, rising traits in markets, as an alternative, ready for proof of sturdiness and persistence in revenues and earnings earlier than embarking on our supposed long-term journey— and this strategy has usually served us properly for over three a long time. We acknowledge that the timing of our latest acquisitions of NVIDIA and Broadcom are after the costs for each have appreciated materially, nevertheless it’s our perception that we’re nonetheless within the early innings of this Gen AI infrastructure buildout and so count on these new additions will ship necessary contributions to the earnings development and complete return of the portfolio. Mixed with the opposite extremely competitively advantaged companies we personal, we anticipate mid-teens or higher earnings development over the long run and count on that the portfolio’s returns will converge with the underlying earnings profile in time.

Whereas the Magnificent 7 corporations—a homogeneous grouping we imagine oversimplifies the variations amongst these companies— continues to seize the headlines and drive market efficiency, we now have additionally seen rising divergence among the many constituents to date this 12 months which could recommend that their heterogeneity is changing into extra outstanding. Mixed with the superior efficiency of companies outdoors of this group (e.g. Oracle, Broadcom) it might be that we’re lastly seeing a broadening of market efficiency away from this grouping, which we imagine bodes properly for our portfolio of nice development companies that span the spectrum of sturdy development alternatives throughout sectors and industries.

Thanks on your curiosity in Polen Capital and the Focus Development technique. Please be at liberty to contact us with any questions or feedback.

Sincerely,

Dan Davidowitz and Damon Ficklin

Authentic Publish

Editor’s Notice: The abstract bullets for this text had been chosen by In search of Alpha editors.