A pointy escalation in US-Iran hostilities in a single day rattled power markets and danger sentiment on Wednesday, driving crude oil firmly greater and snapping the S&P 500’s nine-session profitable streak.

A simultaneous wave of stronger-than-expected US financial releases, together with a considerably above-forecast ADP employment report and a strong ISM Companies PMI, strengthened the likelihood that the Federal Reserve might shift towards a extra hawkish coverage stance, pushing Treasury yields and the greenback broadly greater whereas weighing on gold and Bitcoin.

Take a look at the foreign exchange information and financial updates you’ll have missed within the newest buying and selling session!

Foreign exchange Information Headlines & Information:

- Japan S&P World Companies PMI Remaining for Might 2026: 50.0 (50.0 forecast; 51.0 earlier)

- Australia GDP Development Fee for Q1 2026: 0.3% q/q (0.5% q/q forecast; 0.8% q/q earlier)

- China RatingDog Companies PMI for Might 2026: 54.4 (52.5 forecast; 52.6 earlier)

- Germany S&P World Companies PMI Remaining for Might 2026: 48.1 (47.8 forecast; 46.9 earlier)

- Euro space S&P World Companies PMI Remaining for Might 2026: 47.7 (46.4 forecast; 47.6 earlier)

- U.Ok. S&P World Companies PMI Remaining for Might 2026: 49.3 (47.9 forecast; 52.7 earlier)

- Euro space PPI for April 2026: 0.6% m/m (1.9% m/m forecast; 3.4% m/m earlier)

- Germany New Automotive Registrations for Might 2026: 0.1% y/y (4.2% y/y forecast; 2.7% y/y earlier)

- U.S. MBA 30-12 months Mortgage Fee for Might 29, 2026: 6.57% (6.65% earlier)

- MBA Mortgage Functions for Might 29, 2026: -2.5% (-8.5% earlier)

- ADP Nationwide Employment Report for Might 2026: 122.0k (75.0k forecast; 109.0k earlier)

- Canada Labor Productiveness for Q1 2026: -0.5% q/q (0.5% q/q forecast; -0.1% q/q earlier)

- Canada S&P World Companies PMI for Might 2026: 50.6 (49.6 forecast; 49.2 earlier)

- U.S. S&P World Companies PMI Remaining for Might 2026: 50.7 (50.9 forecast; 51.0 earlier)

- ISM Companies PMI for Might 2026: 54.5 (53.0 forecast; 53.6 earlier)

- U.S. Manufacturing facility Orders for April 2026: 4.8% m/m (2.7% m/m forecast; 1.5% m/m earlier)

- U.S. EIA Crude Oil Shares Change for Might 29, 2026: -7.97M (-3.33M earlier)

Promotion: TradeZella is the highest journaling app within the business, and its new AI buying and selling associate characteristic can break down and analyze your trades & construct a recreation plan, releasing up time and power to deal with the subsequent strikes!

Begin Your Buying and selling Journey with Tradezella & use code “PIPS20” for 20% off your first buy!

Disclosure: To assist help our free every day content material, we might earn a fee from our companions in the event you enroll by our hyperlinks, at no further price to you.

Broad Market Value Motion:

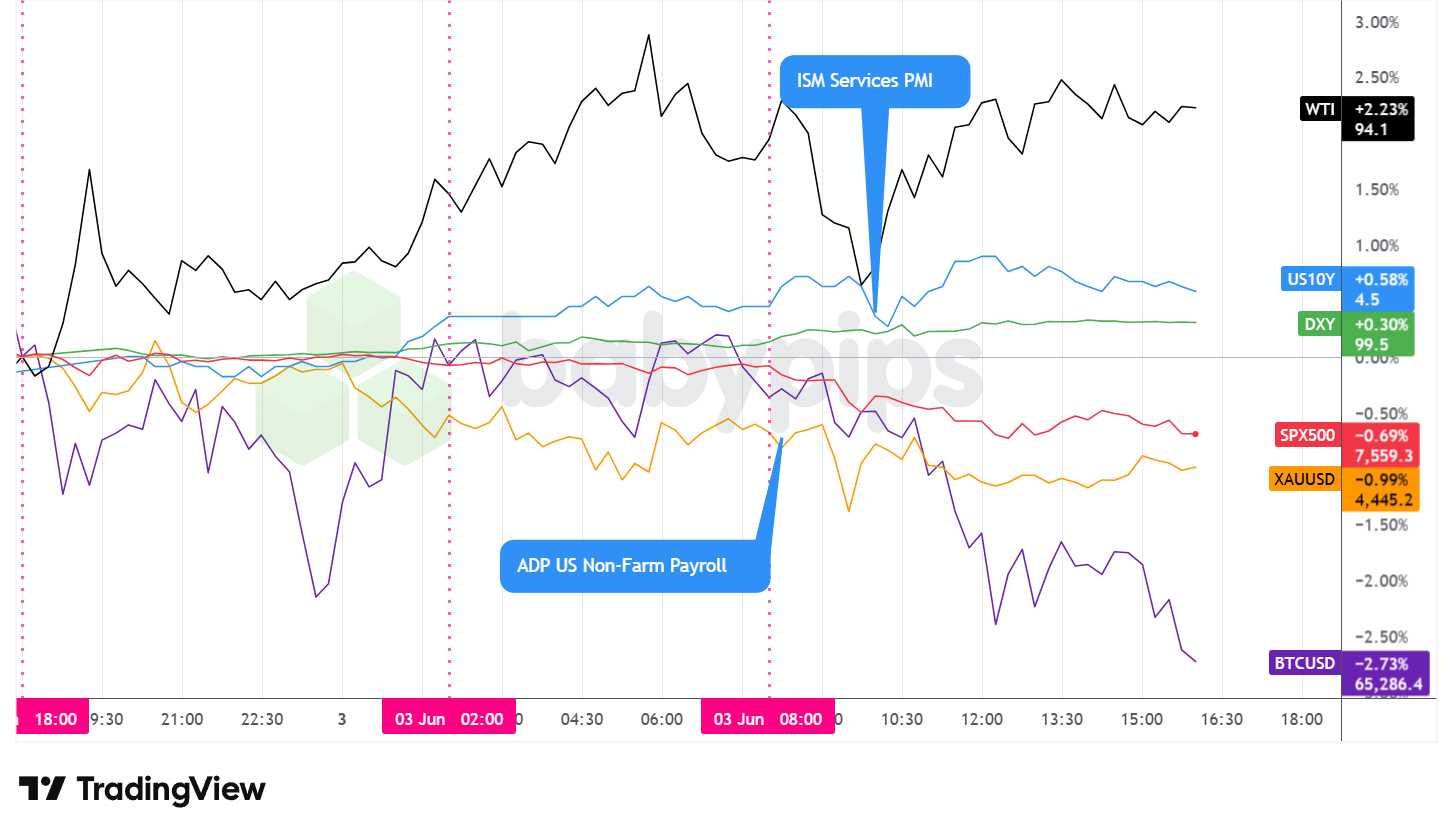

Greenback Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Sooner With TradingView

Wednesday’s session performed out alongside two competing fault strains: a geopolitical danger premium pushed by US-Iran navy exchanges throughout the Gulf, and a hawkish Federal Reserve repricing fueled by stronger-than-expected US financial information. In broad phrases, crude oil surged whereas equities retreated from file highs, valuable metals declined regardless of the battle backdrop, and Treasury yields moved greater.

WTI crude oil was the session’s strongest performer, rising roughly 2.23% to settle close to $94.10 per barrel. The advance started within the Asian session, coinciding with experiences of Iranian ballistic missile strikes on US navy installations in Kuwait and subsequent strikes extending to Bahrain, Saudi Arabia, and Dubai. The in a single day escalation injected a big supply-risk premium into power markets, with costs climbing sharply earlier than consolidating at elevated ranges by the US session. A bigger-than-expected EIA crude stock drawdown of practically 8 million barrels, properly above the prior week’s draw, might have supplied extra help close to the shut.

The S&P 500 snapped a nine-session profitable streak, declining roughly 0.69% to shut close to 7,559. The index traded broadly sideways by the in a single day and early European hours earlier than promoting stress constructed following the ADP employment report, which got here in properly above expectations. Losses appeared to increase additional after the ISM Companies PMI and its related sub-indexes printed considerably forward of forecasts, which the market might have interpreted as reinforcing the case for a higher-for-longer charge setting. Experiences indicated a software-sector ETF fell greater than 4% on the day, with know-how shares among the many harder-hit teams amid the broader risk-off tone.

Gold declined roughly 0.99% to shut close to $4,445, a considerably counterintuitive consequence given the depth of the geopolitical backdrop. Gold was regular through the Asian session earlier than trending steadily decrease by the European and US hours. The decline appeared to coincide most intently with the sturdy US information releases, presumably reflecting a hawkish repricing of actual yield expectations that outweighed the standard safe-haven demand the steel tends to draw in periods of geopolitical stress. It’s value noting that gold’s failure to maintain its earlier beneficial properties regardless of energetic navy exchanges within the Gulf suggests the market’s dominant concern on Wednesday might have been the inflation and Fed coverage implications of the US financial information reasonably than the battle itself.

Bitcoin prolonged its latest selloff, declining roughly 2.73% to commerce close to $65,286. The cryptocurrency drifted decrease by a lot of the session, with promoting accelerating within the afternoon US hours. No single identifiable catalyst was obvious, so the decline possible mirrored ongoing bearish sentiment sparked by Bitcoin ETF outflows and information of the Mt. Gox property transferred roughly 10,306 BTC from chilly storage.

U.S. 10-year Treasury yields rose roughly 0.58% in relative phrases, ending close to 4.50%. Yields trended greater by the session and moved most notably across the ADP and ISM Companies releases, corroborating the broader hawkish repricing narrative. The path of the transfer strengthened alerts that bond markets could also be reassessing the timeline for any near-term Federal Reserve coverage adjustment, with some market commentary noting that persistently sturdy information is reviving dialogue of a possible charge hike reasonably than a lower.

Have a strong buying and selling technique however lack the capital? FundedNext empowers disciplined merchants by offering simulated buying and selling accounts as much as $200K.

Not like different prop corporations, FundedNext imposes no synthetic deadlines on challenges. You even earn a novel 15% revenue share throughout your analysis! As soon as funded, you retain as much as a 95% revenue cut up with assured 24-hour payouts. Commerce CFDs or Futures your manner—even throughout main information occasions.

Be a part of over 400K merchants who’ve acquired $300M+ in payouts. Able to again your edge?

Be taught Extra About FundedNext! Restricted time provide: Use code BPFN for 47% off first 5 Futures FLEX challenges, 40% off of the sixth & past. T&C apply.Disclosure: We might earn a fee from our companions in the event you enroll by our hyperlinks, at no further price to you.

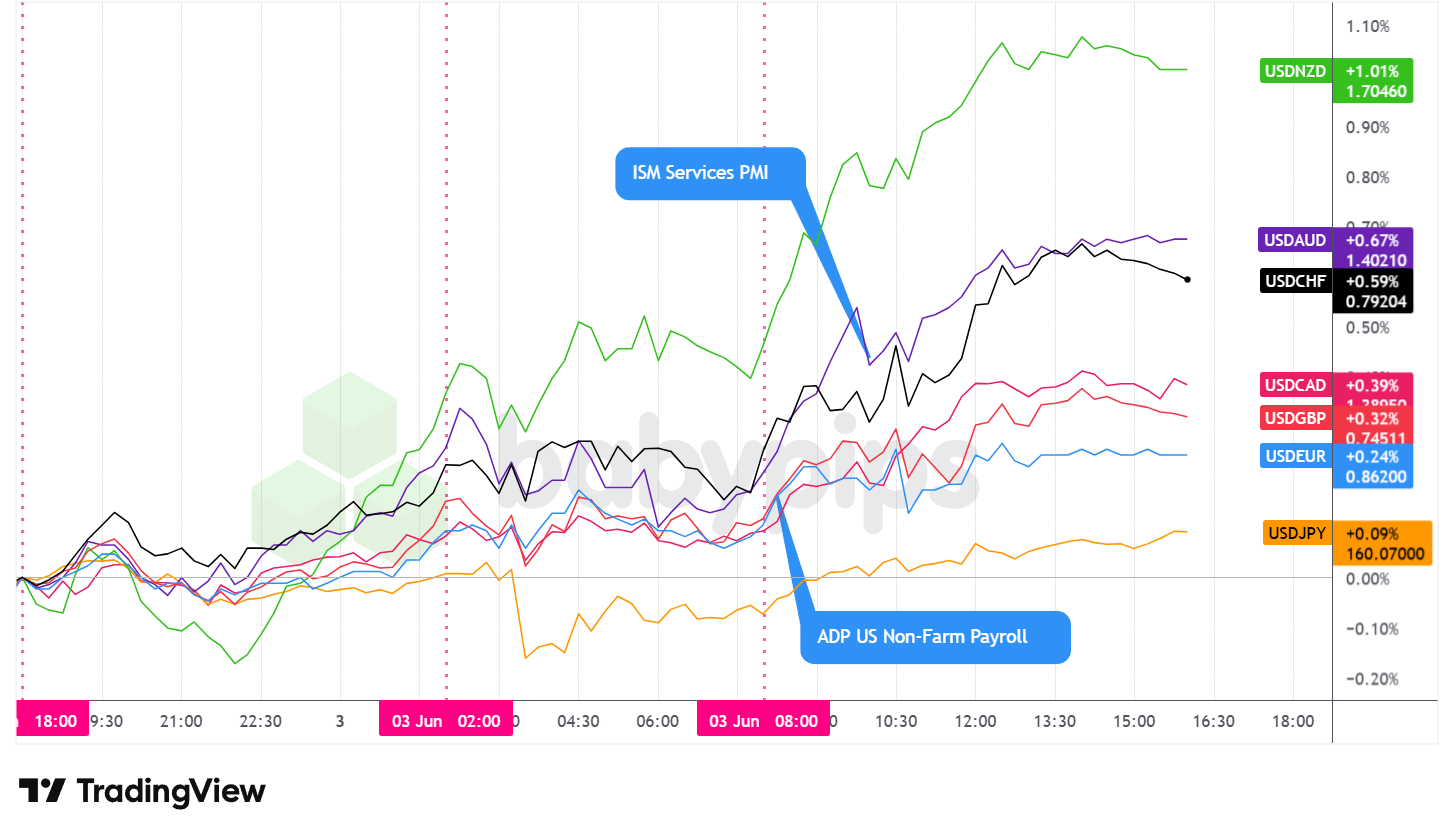

FX Market Conduct: U.S. Greenback vs. Majors

Overlay of USD vs. Majors – Chart Sooner With TradingView

The U.S. greenback traded blended however broadly web greater in opposition to main currencies from the Asia open by the tip of the US session, closing Wednesday because the best-performing main forex every day. The DXY completed with a achieve of roughly 0.30%, buying and selling close to 99.5.

In the course of the Asian session, the greenback drifted web greater in opposition to most main friends, although strikes had been comparatively contained within the early hours. The Iranian missile strikes on Gulf navy installations supplied a probably supportive backdrop for the buck, as safe-haven flows in periods of geopolitical stress have traditionally supplied some help for the greenback. A notable growth for forex markets was USD/JPY approaching the 160.00 degree, the edge at which Japan spent closely on forex intervention in 2024. Finance Minister Katayama deployed a verbal warning, stating Tokyo stood prepared to reply appropriately as wanted. The greenback’s advance within the pair paused close to that degree as merchants grew cautious about urgent the yen additional, limiting what may in any other case have been a extra pronounced transfer.

In the course of the London session, the greenback maintained its modest upward lean as European PMI ultimate readings got here in above preliminary estimates however remained broadly in contractionary territory. Germany’s companies PMI ultimate for Might printed at 48.1, beating the 47.8 preliminary determine. The eurozone companies PMI ultimate got here in at 47.7, above the 46.4 forecast.

The UK’s ultimate companies PMI registered 49.3, a significant enchancment from the 47.9 preliminary studying. Regardless of the upside revisions, the underlying information nonetheless pointed to contraction throughout a lot of European companies exercise, which can have saved modest draw back stress on European currencies relative to the greenback. BOJ Governor Ueda’s reaffirmation of the BoJ’s rate-hiking bias possible supplied some restraint on USD/JPY’s advance by this era, one doable clarification for the yen’s relative resilience in contrast with different main counterparts.

In the course of the U.S. session, the greenback’s upward momentum grew to become extra pronounced as a sequence of sturdy home information releases broadened the efficiency hole between the US financial system and its friends. The ADP Nationwide Employment Report confirmed private-sector payrolls elevated by 122k in Might, properly above the 75k consensus and the strongest studying since January 2025.

The ISM Companies PMI adopted, printing at 54.5 in opposition to a 53.0 forecast, with new orders surging to 57.3 and enterprise exercise reaching 57.7. Manufacturing facility orders additionally got here in considerably above expectations, rising 4.8% month-on-month. The collective energy of the US information strengthened a story of resilient financial momentum alongside persistently elevated service costs, which appeared to drive a hawkish reassessment of Federal Reserve coverage expectations and prolonged the greenback’s beneficial properties in opposition to most main counterparts. The Fed Beige Guide, launched later within the session, famous broadly secure employment and rising inflation pushed by elevated power prices, including additional weight to the image of financial resilience.

Promoted: The Technique is Half the Battle; Your Mindset is the Relaxation.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ opinions on Amazon) Jack Schwager interviews profitable merchants to disclose a typical reality: their edge isn’t simply information or expertise—it’s their psychological resilience and inflexible danger management. Whether or not you’re navigating shifting geopolitical themes or high tier financial information, find out how the “wizards” keep medical when the remainder of the market is emotional.

Grasp Your Buying and selling Mindset with Market Wizards!

Disclosure: We might earn a fee from our companions in the event you enroll by our hyperlinks, at no further price to you.

Upcoming Potential Catalysts on the Financial Calendar

- Australia Steadiness of Commerce for April 2026 at 1:30 am GMT

- Australia RBA Gov Bullock Speech at 5:00 am GMT

- Australia RBA Kent Speech at 5:00 am GMT

- Swiss Inflation Fee for Might 2026 at 6:30 am GMT

- Swiss Unemployment Fee for Might 2026 at 7:00 am GMT

- European Central Financial institution President Lagarde Speech at 8:00 am GMT

- U.Ok. New Automotive Gross sales for Might 2026 at 8:00 am GMT

- Euro space Retail Gross sales for April 2026 at 9:00 am GMT

- U.S. Challenger Job Cuts for Might 2026 at 9:30 am GMT

- U.S. Nonfarm Productiveness Remaining for March 31, 2026 at 12:30 pm GMT

- U.S. Unit Labor Prices for March 31, 2026 at 12:30 pm GMT

- U.S. Fed Barkin Speech at 12:30 pm GMT

- U.S. Preliminary Jobless Claims for Might 30, 2026 at 12:30 pm GMT

- Financial institution of England Gov Bailey Speech at 3:40 pm GMT

- U.S. Fed Daly Speech at 5:10 pm GMT

Thursday’s calendar is anchored by the US labor market information cluster at 12:30 pm GMT. Preliminary Jobless Claims for the week ending Might 30 arrive in the future forward of Friday’s Nonfarm Payrolls report, making them an early indicator of whether or not the labor market resilience advised by Wednesday’s ADP beat is extending into the brand new month. Nonfarm Productiveness and Unit Labor Prices for Q1 2026 launch on the similar time, probably including nuance to the inflation and labor price image that markets spent a lot of Wednesday repricing round. Fed Governor Barkin’s speech on the similar hour will draw specific consideration, as any commentary addressing the edge for a coverage shift might transfer the greenback and Treasury market meaningfully given the hawkish repricing already underway.

Within the European session, ECB President Lagarde’s speech at 8:00 am GMT can be watched for her evaluation of inflation danger within the context of the continuing Center East battle, following ECB Govt Board member Elderson’s feedback Wednesday {that a} extended struggle raises the chance of second-round results. Euro space Retail Gross sales for April at 9:00 am GMT will add to the information image of European client well being, related context forward of any ECB coverage sign. BoE Governor Bailey’s speech at 3:40 pm GMT can be monitored for any shift within the Financial institution of England’s tone given the elevated inflation backdrop.

For Australian greenback merchants, RBA Governor Bullock and RBA Kent communicate at 5:00 am GMT within the wake of Wednesday’s softer Q1 GDP print, and their remarks can be parsed for any recalibration of the RBA’s development or charge outlook. The Australian Commerce Steadiness for April at 1:30 am GMT will provide an early have a look at exterior sector situations forward of these appearances.

Keep frosty on the market, foreign exchange mates!

Wednesday’s market noticed conflicting alerts: geopolitical danger within the Gulf, but gold fell. Robust US information, but equities bought off. Oil surged whereas valuable metals declined. Understanding why property moved the way in which they did requires greater than watching one chart at a time. Premium members can learn our lesson:

📖 What Is Intermarket Evaluation?

Studying this helps you perceive how asset courses join to one another, why gold’s failure to maintain beneficial properties regardless of battle reveals the market’s true concern, and the way the connection between oil, bonds, equities, and currencies tells you what merchants are literally apprehensive about.

And in the event you’re not a Premium subscriber but, now is an effective time to hitch.

With Babypips Premium, you get full entry to College of Pipsology classes that assist you to perceive the hidden relationships between markets, so that you’re studying what the market truly cares about reasonably than simply reacting to headlines.

👉 Subscribe to Babypips Premium

{kind=link}