Whereas many shares can seem cheaper after a sell-off, the very best long-term alternatives are sometimes present in firms that constantly generate robust returns on invested capital (ROIC), a key measure of how effectively administration converts capital into income.

Amongst large-cap software program firms, Microsoft MSFT) and Adobe ADBE) stand out as two companies with distinctive economics, sturdy aggressive benefits, and an extended historical past of producing spectacular ROIC.

With Microsoft and Adobe inventory buying and selling practically 30% and 50% from their 52-week highs, respectively, buyers could also be questioning which software program chief is the very best buy-the-dip goal.

Picture Supply: Zacks Funding Analysis

Why ROIC Issues for Lengthy-Time period Traders

ROIC measures how successfully an organization generates working income from the capital invested in its enterprise. Corporations with constantly excessive ROIC usually possess aggressive benefits similar to robust manufacturers, community results, or proprietary expertise, and excessive switching prices (The bills or boundaries a buyer faces when altering from one services or products to a different, influencing loyalty and enterprise technique).

Over lengthy durations, shares of companies that earn excessive returns on capital are inclined to outperform as a result of they’ll reinvest income at enticing charges, generate substantial free money circulation, and create vital shareholder worth.

Traders usually view a ROIC of 20% or greater as an indication of an distinctive enterprise, though the suitable benchmark varies by {industry}, capital depth, and price of capital.

Throughout the expertise sector, software program firms usually generate greater ROIC than {hardware} producers because of their greater margins, recurring income streams, and asset-light enterprise fashions. In contrast to {hardware} firms, which require vital funding in manufacturing, stock, and provide chains, software program companies can scale their merchandise with comparatively little incremental capital.

Microsoft: An AI Chief With Stellar Capital Effectivity

Microsoft has developed far past its Home windows roots to grow to be one of many world’s most diversified software program and cloud computing firms. The corporate’s enterprise spans productiveness software program, cloud infrastructure, cybersecurity, gaming, and synthetic intelligence.

Microsoft’s Azure platform stays one of many fastest-growing cloud companies globally, whereas Microsoft 365 continues to learn from excessive buyer retention and recurring subscription income. The tech big’s partnership with OpenAI has additionally made it a key participant within the quickly evolving AI panorama.

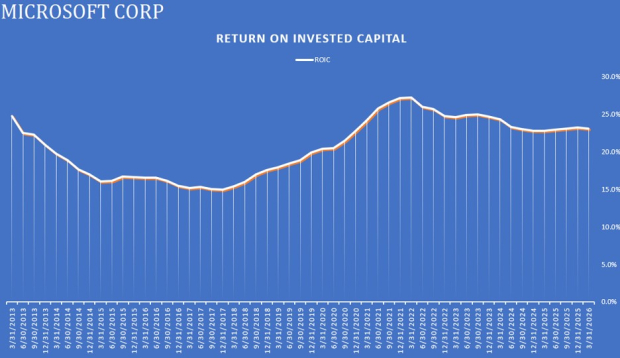

What makes Microsoft notably enticing is its skill to generate huge income whereas requiring comparatively modest capital. For the time being, Microsoft’s ROIC continues to be at a really respectable 23%, reflecting the energy of its software program ecosystem and pricing energy.

Plus, Microsoft’s huge put in base creates vital switching prices for enterprise prospects. As soon as companies construct workflows round Microsoft merchandise, altering distributors will be costly and disruptive. This aggressive moat helps assist regular income progress and industry-leading profitability.

For buyers searching for a high-quality compounder, Microsoft stays one of many strongest companies out there.

Picture Supply: Zacks Funding Analysis

Adobe: A Dominant Franchise Buying and selling at a Extra Engaging Valuation

Adobe might not obtain the identical degree of consideration as AI-focused tech giants, however its enterprise high quality stays distinctive.

To that time, Adobe dominates inventive software program via flagship merchandise similar to Photoshop, Illustrator, Premiere Professional, and Acrobat. These purposes have grow to be {industry} requirements throughout design, advertising, publishing, and digital content material creation.

Adobe’s subscription-based enterprise mannequin generates extremely predictable recurring income whereas supporting robust margins and money circulation technology. Adobe additionally advantages from excessive buyer retention, as professionals usually spend years mastering the corporate’s software program ecosystem.

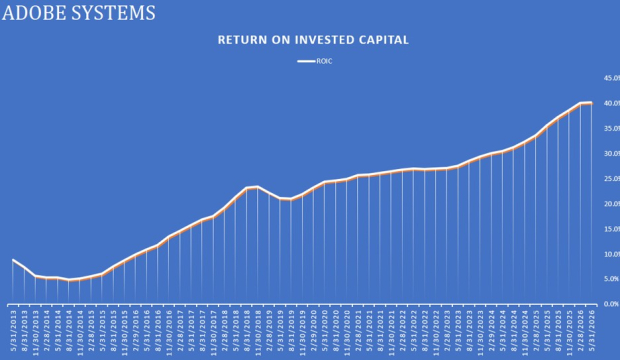

Extra importantly, Adobe has traditionally generated wonderful ROIC with a present mark of 40%, demonstrating its skill to transform income progress into significant shareholder worth.

Picture Supply: Zacks Funding Analysis

Regardless of these strengths, Adobe shares have confronted strain in recent times amid considerations that generative AI instruments might disrupt components of the inventive software program market. Nevertheless, Adobe has aggressively built-in AI capabilities into its product suite via its conversational AI software Firefly, amongst different initiatives.

Retaining this in thoughts, buyers have a chance to think about a world-class software program franchise at a valuation that may be very affordable in comparison with historic ranges, with Adobe inventory buying and selling at simply 10X ahead earnings in comparison with Microsoft’s 23X.

Moreover, ADBE is buying and selling at a 75% low cost to its decade-long median of 41X ahead earnings and is vastly beneath its excessive of 65X throughout this era.

Picture Supply: Zacks Funding Analysis

Conclusion & Strategic Ideas

Traders who prioritize stability and AI-driven progress might desire shopping for Microsoft inventory on the dip, whereas these searching for a probably undervalued software program chief might discover Adobe notably enticing at present ranges.

That mentioned, if you happen to’re seeking to construct wealth over the long run, proudly owning firms with sturdy aggressive benefits and constantly excessive ROIC has traditionally been a successful technique — and Microsoft and Adobe stay among the many strongest examples within the software program {industry}.

Zacks’ Analysis Chief Names “Inventory Most More likely to Double”

Our staff of specialists has simply launched the 5 shares with the best chance of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This high choose is a little-known satellite-based communications agency. Area is projected to grow to be a trillion greenback {industry}, and this firm’s buyer base is rising quick. Analysts have forecasted a significant income breakout in 2025. After all, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our High Inventory And 4 Runners Up

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Adobe Inc. (ADBE) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.