- KYMR Outperforms Trade, Sector & S&P 500 Index

- KYMR Inventory Surges on KT-621 Research Information

- KYMR’s Partnership With Gilead Brings Strategic Advantages

- KYMR’s Deal With Sanofi

- KYMR’s Valuation and Estimates

- Keep Invested in KYMR

- Zacks’ Analysis Chief Picks Inventory Most More likely to “At Least Double”

Kymera Therapeutics, Inc. KYMR has put up a stupendous efficiency over the previous yr. Shares of this clinical-stage biotechnology firm have surged 82.4% over the mentioned timeframe in contrast with the trade’s acquire of 17.3%. The inventory has additionally outperformed the sector and the S&P 500 Index throughout this era.

The rally could be attributed to optimistic pipeline and regulatory updates for lead pipeline candidate KT-621.

KYMR Outperforms Trade, Sector & S&P 500 Index

Picture Supply: Zacks Funding Analysis

Let’s look at KYMR’s fundamentals, progress potential, key challenges, and valuation to make an knowledgeable choice on this context.

KYMR Inventory Surges on KT-621 Research Information

Kymera is deploying focused protein degradation (TPD) to develop medication for crucial well being issues and it has superior the primary degrader into the clinic for immunological ailments.

KT-621 is an investigational, first-in-class, as soon as day by day, oral degrader of STAT6, the particular transcription issue accountable for IL-4/IL-13 signaling and the central driver of kind 2 irritation.

Final month, KYMR inventory surged after the corporate introduced optimistic knowledge from the section Ib BroADen research, which evaluated KT-621 for treating atopic dermatitis (AD), also referred to as eczema.

Information from the research confirmed that therapy with KT-621 led to deep STAT6 degradation in each the 100 mg and 200 mg doses, with median reductions of 94% within the pores and skin and 98% within the blood, displaying that the candidate’s results in wholesome volunteers translated properly to AD sufferers.

Remedy with KT-621 additionally led to sturdy reductions in disease-relevant kind 2 biomarkers in blood, together with Thymus and Activation-Regulated Chemokine (TARC) – median discount of 74% in sufferers with baseline TARC ranges corresponding to Sanofi’s SNY and Regeneron’s REGN Dupixent (dupilumab) research on AD, Eotaxin-3, IL-31, IgE, and in core kind 2 irritation and AD disease-relevant gene units in pores and skin lesions.

KT-621 demonstrated sturdy scientific exercise throughout all measured endpoints within the section Ib BroADen research, together with a imply 63% discount in Eczema Space and Severity Index (EASI) and a imply 40% discount in peak pruritus Numerical Ranking Scale (“NRS”).

Remedy with KT-621 was typically protected and well-tolerated, with no critical adversarial unintended effects noticed.

The optimistic section Ib BroADen outcomes spotlight KT-621’s potential as a first-in-class, once-daily oral remedy for kind 2 inflammatory ailments. Its week-4 outcomes had been corresponding to—and in some instances exceeded—printed knowledge for SNY/REGN’s blockbuster drug, Dupixent, which is authorized for a number of varieties of inflammatory ailments, together with moderate-to-severe AD.

The FDA additionally granted Quick Observe designation to pipeline candidate KT-621 for the therapy of average to extreme AD.

A section IIb research, BROADEN2, in average to extreme AD sufferers on KT-621 is ongoing, with knowledge anticipated to be launched by mid-2027. Kymera additionally plans to provoke a section IIb research, BREADTH, of KT-621 in bronchial asthma within the first quarter of 2026. These research intention to hurry KT-621’s growth and decide optimum dosing for upcoming subsequent parallel section III registration research in a number of kind 2 dermatology, gastroenterology and respiratory ailments.

KYMR’s Partnership With Gilead Brings Strategic Advantages

In June 2025, Kymera entered into an unique possibility and license settlement with Gilead Sciences, Inc. GILD to speed up the event and commercialization of a novel molecular glue degrader program focusing on cyclin-dependent kinase 2 (CDK2) with broad oncology therapy potential in breast most cancers and different stable tumors.

Kymera is advancing preclinical actions for its CDK2 molecular glue program geared toward treating breast most cancers and stable tumors. If Gilead workout routines its possibility, which incorporates an possibility cost to Kymera, it could assume all growth, manufacturing and commercialization duties for any merchandise ensuing from the collaboration.

KYMR’s Deal With Sanofi

Kymera additionally has a collaboration with Sanofi to advance its pipeline. Nevertheless, in June 2025, Sanofi knowledgeable Kymera that it has chosen KT-485/SAR447971, an oral, extremely potent and selective growth candidate focusing on IRAK4 for immuno-inflammatory ailments, to advance into scientific research.

The candidate was found by Kymera. KT-485 is being prioritized for growth beneath the businesses’ current IRAK4 collaboration following in depth preclinical work supporting its sturdy growth potential. The candidate is predicted to advance into early-stage testing subsequent yr.

Consequently, Sanofi discontinued the event of KT-474, which was being evaluated for the therapy of hidradenitis suppurativa and AD in two section IIb dose-ranging research.

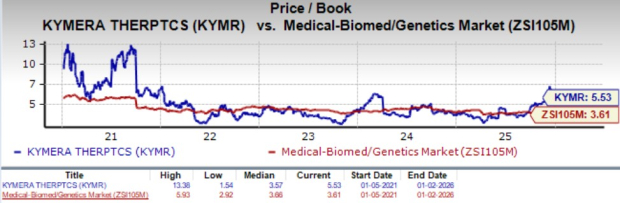

KYMR’s Valuation and Estimates

From a valuation perspective, KYMR is overvalued. Going by the value/e-book ratio, KYMR’s shares presently commerce at 5.53X, increased than 3.61X for the biotech trade and the corporate’s imply of three.57X.

Picture Supply: Zacks Funding Analysis

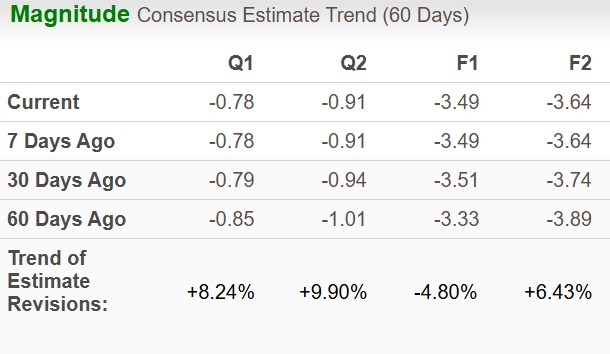

The Zacks Consensus Estimate for 2025 loss per share has widened over the previous 60 days whereas that for 2026 loss has narrowed to $3.64 in the identical timeframe.

Picture Supply: Zacks Funding Analysis

Keep Invested in KYMR

Kymera’s novel TPD method is promising, and the pipeline progress is encouraging.

Further optimistic pipeline updates on KT-621 will likely be a major increase for the inventory. Therefore, we suggest current traders to carry the inventory for now.

Nevertheless, potential traders ought to look forward to a greater entry level. Though the oncology take care of GILD seems promising and the ensuing inflow of money is encouraging, there may be nonetheless an extended solution to go.

Sanofi’s choice to advance preclinical IRAK4 degrader KT-485 somewhat than advancing KT-474 delayed milestone funds for Kymera that might have been achieved on the approval of KT-474, which had moved to section IIb research in late 2023.

KYMR presently carries a Zacks Rank #3 (Maintain). You possibly can see the entire record of as we speak’s Zacks #1 Rank (Sturdy Purchase) shares right here.

Zacks’ Analysis Chief Picks Inventory Most More likely to “At Least Double”

Our consultants have revealed their High 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. After all, all our picks aren’t winners however this one might far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our High Inventory to Double (Plus 4 Runners Up) >>

Regeneron Prescribed drugs, Inc. (REGN) : Free Inventory Evaluation Report

Sanofi (SNY) : Free Inventory Evaluation Report

Gilead Sciences, Inc. (GILD) : Free Inventory Evaluation Report

Kymera Therapeutics, Inc. (KYMR) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.