A serious week of earnings outcomes is upon us, with a number of hyperscalers – Meta Platforms META and Microsoft MSFT – on the docket. Each shares have underperformed the S&P 500 by a notable margin during the last three months, as proven beneath.

Picture Supply: Zacks Funding Analysis

Whereas the efficiency has been visibly weak, among the draw back can probably be attributed to scrutiny of all of the AI spend, which has exploded for each over the previous 12 months.

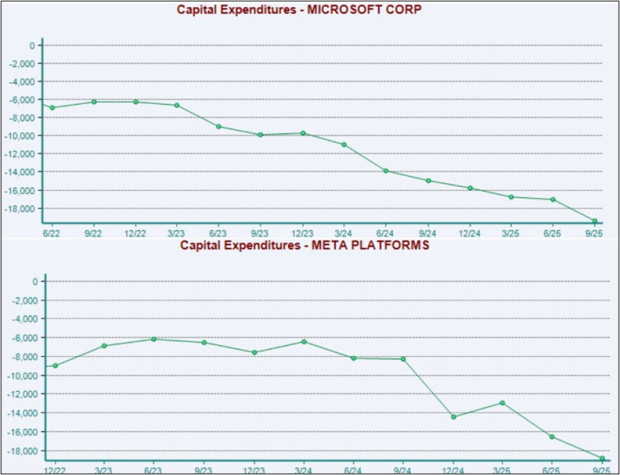

Under is a chart illustrating the capital expenditures of each over the previous a number of years, with a transparent acceleration seen all through 2024 and 2025. Please notice that the chart beneath treats CapEx as an expense, explaining the unfavorable values.

Picture Supply: Zacks Funding Analysis

Anticipate each corporations to spend the vast majority of their calls discussing the AI outlook, a theme we received’t be getting away from anytime quickly.

Are Analysts Bullish?

Each EPS and gross sales revisions for META and MSFT haven’t budged a lot over the previous few months, largely reflecting stability. Each are nonetheless forecasted to see development, with META’s earnings anticipated to be up 1.6% and MSFT anticipated to see a a lot stronger 20% development fee. Regarding gross sales, MSFT is predicted to see 15% greater revenues, whereas META’s revenues are anticipated to develop 20.7% year-over-year.

Whereas analysts haven’t raised their expectations in a transparent bullish means, the steadiness of each EPS and gross sales revisions for the duo stays a optimistic takeaway. Destructive revisions heading into the discharge would warrant some warning, which we simply haven’t seen over latest months. Understand that MSFT can be presently a Zacks Rank #2 (Purchase), with optimistic revisions for different intervals maintaining its total earnings outlook sturdy.

Watch These Metrics

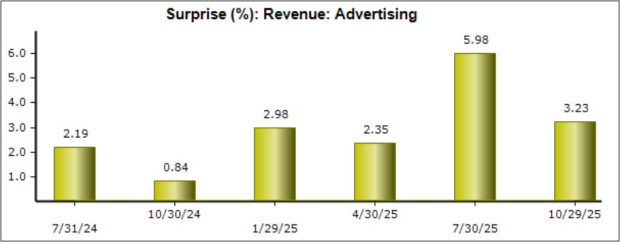

Promoting outcomes are typically the most important metric traders watch closely for META, accounting for the majority of the tech titan’s income. AI implementations have enabled the corporate to ship extra related advertisements to shoppers, boosting efficiency considerably over latest intervals.

We anticipate Meta Platforms to submit $56.8 billion in advert income, reflecting a large 21% bounce year-over-year. The corporate has recurrently blown away our consensus expectations on the metric, with the beats rising in measurement. The YoY development fee right here can be largely according to latest intervals, a key hurdle that traders might be watching.

Under is a chart illustrating META’s advert income outcomes relative to our consensus expectations, expressed as a share.

Picture Supply: Zacks Funding Analysis

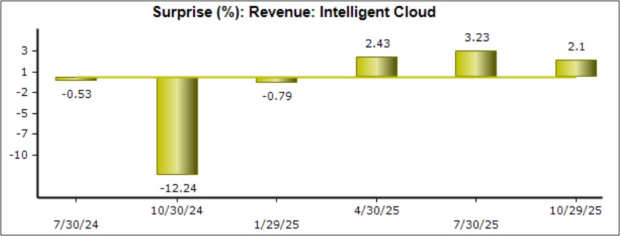

Regarding MSFT, cloud income might be a serious focus. Its Clever Cloud outcomes embody Azure, the cloud platform that gives the computing energy and infrastructure that AI wants. The buildout and enlargement of the platform are the first drivers behind its giant CapEx will increase, that are anticipated to repay in an enormous means.

Our consensus estimate for MSFT’s Clever Cloud income stands at $32.4 billion, reflecting a powerful 27% YoY enchancment. The corporate has seen an acceleration within the metric, with any additional enchancment more likely to impress traders in an enormous means.

MSFT has strung collectively three consecutive beats on the metric relative to our expectations, as proven beneath.

Picture Supply: Zacks Funding Analysis

Placing Every little thing Collectively

Stability in gross sales and EPS revisions for each corporations positions them effectively heading into their releases, although traders will definitely be laser-focused on capital expenditures and every thing else associated to the broader AI frenzy.

It’s additionally price noting that Microsoft MSFT shares have been big-time laggards over the previous two years relative to each Meta Platforms META and the S&P 500. The efficiency disparity might simply start to vary post-earnings if MSFT continues its favorable cloud outcomes, with its present Zacks Rank #2 (Purchase) additionally an enormous tailwind.

Zacks Names #1 Semiconductor Inventory

This under-the-radar firm focuses on semiconductor merchandise that titans like NVIDIA do not construct. It is uniquely positioned to benefit from the following development stage of this market. And it is simply starting to enter the highlight, which is precisely the place you wish to be.

With sturdy earnings development and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. World semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $971 billion by 2028.

See This Inventory Now for Free >>

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.