Howmet Aerospace Inc. HWM has been experiencing persistent weak point in its business transportation market. In third-quarter 2025, revenues from the business transportation market declined 3% on a year-over-year foundation, following 14% and 4% declines within the first and second quarters, respectively.

Decrease business truck builds, given tariff-related and financial uncertainty in North America, have been impacting the corporate’s near-term efficiency. Demand within the business transportation markets served by the Cast Wheels section is anticipated to stay smooth within the close to time period as a consequence of decrease OEM builds. Additionally, rising uncooked materials prices, significantly aluminum, and stringent emission rules are regarding for the section.

As a world participant, Howmet Aerospace stays susceptible to supply-chain volatility, which has already led to delays and better prices in recent times. These supply-chain challenges within the transportation and aerospace sectors would possibly proceed affecting the corporate’s capability to ship completed merchandise to prospects inside the stipulated time.

Regardless of troublesome situations within the business transportation market, Howmet Aerospace’s efficiency is being bolstered by sustained energy within the business and protection aerospace markets. Robust demand for engine spares for the F-35 program, aerospace fastening programs and airframe structural parts additional contributes to a promising outlook for the corporate.

Phase Snapshot of HWM’s Friends

ITT Inc.’s ITT Movement Applied sciences section is witnessing sturdy demand for brake parts and specialised sealing options, shock absorbers and damping applied sciences in OEM and rail transportation markets. The section’s natural revenues rose 1.4% yr over yr within the first 9 months. For 2025, ITT expects its general natural gross sales to extend 3-5% from the year-ago stage.

Kennametal Inc.’s KMT Steel Reducing section is benefiting from stable momentum throughout its a number of finish markets. This consists of a rise in aerospace authentic tools producer construct charges within the Americas area, easing supply-chain pressures and strong U.S. and worldwide protection spending volumes. Kennametal’s Steel Reducing section’s natural revenues elevated 3% yr over yr within the first three months of fiscal 2026.

HWM’s Value Efficiency, Valuation and Estimates

Shares of Howmet Aerospace have surged 84.7% up to now yr in contrast with the trade’s development of 36.1%.

Picture Supply: Zacks Funding Analysis

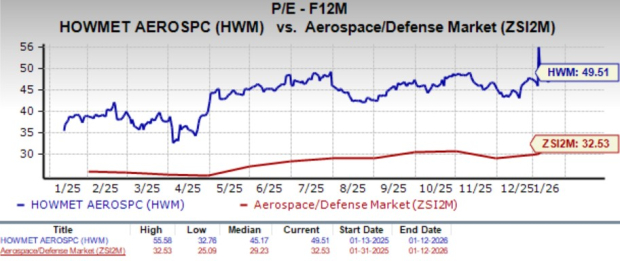

From a valuation standpoint, HWM is buying and selling at a ahead price-to-earnings ratio of 49.51X, above the trade’s common of 32.53X. Howmet Aerospace carries a Worth Rating of D.

Picture Supply: Zacks Funding Analysis

The Zacks Consensus Estimate for HWM’s earnings has been steady over the previous 60 days.

Picture Supply: Zacks Funding Analysis

Howmet Aerospace at present carries a Zacks Rank #3 (Maintain). You’ll be able to see the entire record of right now’s Zacks #1 Rank (Robust Purchase) shares right here.

Zacks’ Analysis Chief Names “Inventory Most Prone to Double”

Our group of consultants has simply launched the 5 shares with the best chance of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This prime choose is a little-known satellite-based communications agency. Area is projected to develop into a trillion greenback trade, and this firm’s buyer base is rising quick. Analysts have forecasted a serious income breakout in 2025. In fact, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our High Inventory And 4 Runners Up

ITT Inc. (ITT) : Free Inventory Evaluation Report

Kennametal Inc. (KMT) : Free Inventory Evaluation Report

Howmet Aerospace Inc. (HWM) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.