- Efficiency and internet asset worth

- Worth traps versus “loss reserving” and danger dispersion

- Bolloré: €1.2billion of “sentiment” de-rating over twelve months

- Exor: assessing the personal holdings for a clue to the long run.

alexsl/iStock by way of Getty Pictures

Efficiency and internet asset worth

† in spite of everything ongoing and efficiency charges. Andrew Brown is making two displays on the Passive Investor Occasion in Dallas, TX hosted by Monetary Journey and Keith Blackborg on October 23rd & 24th passiveinvestorevent.com |

The Dynasty Belief NAV elevated by a modest 1.6% within the September quarter. We’re categoric that we are going to not preserve tempo with wider indices in markets the place surplus liquidity chases short-term concepts with minimal funding benefit. Not surprisingly, when such behaviour turned much more prevalent in September, the lags have been higher. We additionally don’t have any publicity to treasured steel producers.

Of the three firms mentioned on this quarterly, two have stellar long-term monitor data. Each have been destructive contributors within the quarter on account of a additional de-rating of the respective firm’s share value relative to our estimate of its intrinsic worth. Particularly, the 4 exposures within the Bolloré (OTCPK:BOIVF) group value over 1.1% to NAV over the quarter. We present that Bolloré itself has suffered an efficient €1.2billion de-rating versus our estimates of worth over a twelve-month interval, which we view as being symptomatic of the prevailing impatient surroundings. There are self-inflicted the explanation why the corporate and its satellites are struggling for investor consideration at current, however all are solvable. Likewise, the de-rating of Exor (OTCPK:EXXRF) regardless of exemplary capital administration is explainable, however excessive even when acknowledging extra bearish eventualities for the influence of US tariffs on two of their most vital investee firms, Stellantis and CNHI.

As beforehand famous in month-to-month releases, we exited Catapult Worldwide (OTCPK:CAZGF), Sportradar (SRAD), Harworth Group and Borr Drilling (BORR) over the quarter. We added a small Australian firm, DGL Group, which is a major chemical distribution firm, managed by its CEO, Simon Henry. The corporate IPO’d at A$1 in mid-2021 and have become a market-darling (amazingly) reaching over $4 by April 2022. This mirrored a newfound means for public-private arbitrage plus the advantage of being one in every of few Australian Adblue diesel additive suppliers throughout COVID (the product value elevated six-fold). The FY2025 yr noticed earnings (EBIT) some 60% under that peak FY22 peak yr as the corporate suffered a level of indigestion from acquisitions with duplicate CRM techniques and a loss-making lead battery recycling facility which has now been closed. Established in 1999, DGL is an actual founder-led enterprise which has arguably struggled to make the transition to public firm standing. Nonetheless, its {industry} positioning and chosen entry boundaries, value outs and debt discount recommend the shares at our acquisition value are value at under 10x P/E, 60% of tangible guide, and EV/EBITDA under 5x.

The key (>30bp) absolute contributors in Australian {dollars} to quarterly return are tabulated under; as a information solely, the person inventory returns are in native forex for the precise interval, not our holding interval. Power within the Australian greenback over the quarter decreased returns by ~80bp. (‡ September solely):

|

Constructive |

Damaging |

||||

|

contribution |

return |

contribution |

return |

||

|

Borr Drilling |

80bp |

47.3% |

Virtu Monetary (VIRT) |

-92bp |

-20.7% |

|

Carlyle Group (CG) |

70bp |

22.0% |

Novo Nordisk (NVO) |

-64bp |

-21.6% |

|

First Pacific Co. (OTCPK:FPAFF) |

50bp |

17.4% |

Cie de L’Odet |

-46bp |

-8.6% |

|

Viel et Cie (OTC:VIELF) |

39bp |

10.5% |

Bolloré (OTCPK:BOIVF) |

-37bp |

-9.6% |

|

HAL Belief (OTCPK:HALFF) |

38bp |

11.7% |

D’Ieteren Group (OTCPK:SIEVF) |

-36bp |

-12.7% |

|

DGL Group ‡ |

35bp |

21.6% |

Lagardère (OTCPK:LGDDF) |

-35bp |

-8.4% |

Dynasty Belief’s high twenty positions as of 30 September 2025 as a share of internet asset worth are:

|

Viel et Cie |

4.61% |

Exor NV (OTCPK:EXXRF) |

3.15% |

|

Avolta (OTCPK:DFRYF) |

4.19% |

First Pacific Firm |

3.03% |

|

Compagnie de L’Odet (OTCPK:FCODF) |

4.13% |

Avation PLC |

3.00% |

|

Carlyle Group |

4.04% |

Bolloré |

2.92% |

|

Lagardère |

3.89% |

Nelnet Inc (NNI) |

2.91% |

|

Virtu Monetary |

3.89% |

Douglas AG |

2.79% |

|

HAL Belief |

3.59% |

Vivendi (OTCPK:VVVNF) |

2.72% |

|

E-L Monetary Corp (OTCPK:ELFIF) |

3.45% |

AKER BP ASA (OTCQX:AKRBF) |

2.62% |

|

CK Hutchison (OTCPK:CKHUF) |

3.40% |

MFF Investments |

2.56% |

|

Fairfax Monetary Holdings (OTCPK:FRFHF) |

3.39% |

BOC Aviation (OTCPK:BCVVF) |

2.54% |

At quarter finish, we retained round a 6% internet money weighting in spite of everything accruals.

Worth traps versus “loss reserving” and danger dispersion

The three securities we talk about under – Bolloré (-21% in CY2025), Exor (-7%) and Swatch Group (-9.3%) – are hardly disasters however are regarded by some as worth traps; we have a look at them extra as “loss reserving” (see under for context) providing scope for future efficiency. All are run by patriarchs with a decidedly totally different and infrequently contrarian method. That’s why we wish to set the scene by discussing worth traps versus quick time period points.

Our analytical strategies unreservedly concentrate on “valuation” – ascribing a value vary inside which we’re joyful to buy fairness securities of the specified managed firm, primarily based on our outlook. Most completed worth investing practitioners are inclined to set the bar “low” with conservative assumptions to derive Klarman’s revered “margin of security” between value paid and worth derived[1]. However in its 257 pages, the phrase “lure” doesn’t seem as soon as (we used AI to verify…)

Each forward-looking investor should settle for the scope for error as industries and applied sciences change, administration make errors, and uncontrollable elements unravel the assumptions behind valuation. In fact, essentially the most irritating of all “errors” is the place the evaluation of the underlying enterprise is appropriate however by no means will get mirrored within the fairness value.

Not like many others, now we have two definitions of a price lure, which don’t essentially coalesce:

- The backward-looking evaluation; and

- Ahead-looking capital entrapment or misuse

The standard definition of a price lure comes about from screening by worth traders, utilizing backwards-looking metrics designed to isolate an fairness as “low-cost”. Low value/earnings ratio, excessive yield, low value to guide worth. These illusory metrics are normally accompanied by declining enterprise fundamentals, during which scenario, guide worth sometimes is overstated, with earnings and dividends unmaintainable. Buyers in “backwards” trying worth traps are sometimes in search of a turnaround resolution, which within the overwhelming majority of circumstances, fails to materialise.

In our view, that’s not likely a price lure – it’s inaccurate evaluation of the corporate’s (or {industry}’s) fundamentals. We stress that we try to construct “a portfolio of high quality companies, beneath the aegis of controlling shareholders”. IF our evaluation is not less than partly appropriate, we’d be screening out the normal dying or declining companies. We all know quite a few glorious traders who’re largely agnostic about enterprise high quality as a result of their evaluation focuses on the flexibility to grasp belongings in a near-immediate timeframe and yield excessive inside charges of return. Period is their enemy, which is why excluding distinctive circumstances, due to our desire for compounding, we don’t have a lot curiosity for these kinds of conditions. Nonetheless, the actual space of interrogation comes from understanding not simply the price-value hole however how the differential will likely be not less than partially eradicated.

Our opinion that worth traps characterize an ongoing portfolio danger has been enunciated each time we current. Our definition of a price lure is a safety which trades at a major {discount} to intrinsic worth however the place a controller has non-financial aspirations which prohibit this worth being realised for the advantage of different shareholders, and the place the intrinsic worth might consequently dissipate.

Such controllers have different aspirations resembling:

- An emotional attachment to an actual asset – normally a historic property (J.W. Mays is a traditional on this respect with its Brooklyn constructing) – or enterprise;

- Being joyful to earn under affordable returns from the belongings in pursuit of a life-style firm (MAYS once more, maybe); or

- Derivation of energy, affect and standing – normally seen in media and sports activities.

There are quite a few examples in media of controllers failing to liberate as soon as sturdy money circulate for shareholder profit after which seeing these rivers of gold dissipate as technological change diverts them moderately than forming a shareholder tributary. The simplest illustration -conceptually and numerically – of a price lure is a listed sports activities staff[2].

On the product degree, sports activities groups are amongst essentially the most enviable companies. The purchasers are extremely loyal, even when the product delivered is very faulty however can’t be returned, and when the worth of mentioned product rises inexorably yearly. With these sentiments in thoughts, let’s have fast have a look at Manchester United PLC (MANU) the well-known English Premier League staff, managed by the US primarily based Glazer household, which has an fairness market capitalisation of £2.086billion, and internet debt of £640million, excluding commitments to pay for bought gamers.

Over the previous eight years, the membership has endured COVID-reduced attendances, a change of controlling personnel on the soccer facet, and gained solely two trophies – each home English knock-out competitions (League Cup 2022/23 and FA Cup 2023/24). The staff has been within the profitable UEFA Champions League in 5 of the eight years however won’t be in any UEFA competitors within the yr to 30 June 2026.

Manchester United PLC: chosen monetary statistics

|

£million y/finish June |

Income |

Op Money circulate |

Capex |

Internet participant spend |

PRE FINANCING CASH FLOW |

|

2018 |

589.8 |

119.6 |

(13.2) |

(108.1) |

(1.7) |

|

2019 |

627.2 |

263.6 |

(13.7) |

(135.2) |

114.7 |

|

2020 |

509.0 |

17.6 |

(21.3) |

(85.1) |

(88.8) |

|

2021 |

494.1 |

137.8 |

(6.2) |

(133.6) |

(2.0) |

|

2022 |

583.2 |

121.7 |

(8.3) |

(191.6) |

(78.2) |

|

2023 |

648.4 |

128.9 |

(15.6) |

(124.6) |

(11.3) |

|

2024 |

661.8 |

117.5 |

(17.5) |

(153.7) |

(53.7) |

|

2025 |

666.5 |

107.5 |

(44.7) |

(229.9) |

(167.1) |

The desk above strips away the financing construction which might in any other case obscure the evaluation, and tax paid has not been a consideration, so we are able to merely have a look at working money circulate, much less capex (services) much less funds for the acquisition of participant contracts minus the proceeds from participant contract gross sales.

The general public firm, regardless of persevering with to have profitable broadcasting contracts and sponsorship offers, has lived in a fantasy-world with:

- excessive prices – OCF doesn’t develop with income because of excessive wages;

- low/no spend on the shopper expertise or participant facility seen in low capex which now has to play catch-up with a latest £50million coaching floor overhaul; and

- outlandish internet spend on switch charges which has yielded no on-field success.

Consequently, shares in MANU are under their ranges of early 2013, internet debt is up by £185million (excluding commitments) and market capitalisation has grown solely due to new share points.

Readers who’ve adopted our progress over practically three years will recall that in mid-2023, we held a place in MANU when the financials regarded much better than they do now and it was clear there can be a contest for management of the corporate being run by the Florida-based controllers. Sadly, in fact, moderately than accepting the alleged highest 100% bid from Sheikh Jassim[3], they took the choice to carry on and settle for new fairness from Sir Jim Ratcliffe. Ratcliffe ended up buying present inventory (25% of every holders’ shares) and new funding at US$33/share or a £4.5billion valuation of MANU fairness – over twice the prevailing pricing of ~£2.1billion. The Glazers publicly mentioned they believed the membership valuation might double to £10billion over time. By no means say by no means…

Of all worth traps, MANU is essentially the most troublesome to rationally clarify since there seems little profit to the controllers, even in an emotional sense, since, within the creator’s view, the vast majority of membership supporters don’t particularly just like the Glazers given the latest monitor document. Emotion might dictate an excellent higher value than that allegedly provided for full management by Sheikh Jassim however given the capital expenditure required – on stadia and gamers – in addition to luck to return to the place simply two years in the past – the rejection of such a hefty value was weird on the time and the extra so now.

On this context, the place we maintain seemingly inert securities buying and selling at low-cost valuations, the advantages of holding them and smart portfolio diversification are sometimes not seen till fairness markets hit a velocity bump. US cash printing, deficit funding and a perception that AI transformation is a panacea for every part regardless of near-term dilution of return on invested capital have created an surroundings the place liquidity is plentiful. In the meanwhile. In such a milieu, capital inevitably flows to areas offering substandard future returns – traders simply demand or not it’s put to work. The lust for fast returns ensures that many securities buying and selling at monumental reductions to intrinsic worth are discarded as having “no catalyst” or ones the place a number of months therefore is perceived as “too far off”.

In fact, some firms don’t possess redeeming options and are greatest averted by all.

One of many benefits of getting an insurance coverage background is direct information of the advantages of conservative loss reserving. Not incomes outsized returns at instances of excessive premiums and seemingly low loss ratios however “smoothing” and stacking revenue away for a “wet day”. It’s assuring at instances like these that our complete portfolio doesn’t commerce at multi-year highs and that now we have a variety of sleepers which haven’t contributed – nor meaningfully detracted – from absolute return. These holdings could be assessed as our “surplus loss reserves” which is able to contribute to future return at a time when fairness market returns could also be extra problematic than at current.

Bolloré: €1.2billion of “sentiment” de-rating over twelve months

Vincent Bolloré have to be considering that “2025 shouldn’t be a yr on which he shall look again with undiluted pleasure. Within the phrases of one in every of his extra sympathetic correspondents, it has turned out to be an Annus Horribilis”[4]

A yr in the past (QR#7) we assessed the company construction of Bolloré to determine the bona fides of rolling the self-control loop up not less than two tiers and its influence on household management. On the time. Bolloré shares have been buying and selling just under €6 with the Vivendi break up nonetheless to come back, however the full acquisition of the Rivaud firms[5] beneath approach.

Since then:

- the Vivendi break up has taken place however reconstituting the corporate by including the buying and selling costs of the spun-out autos Canal+, Louis Hachette Group and Havas to Vivendi provides a “worth” of €8.91 towards €10.30 a yr in the past – a “diminution” value about €420million (€0.38 per Bolloré share[6])

- the expropriation of the Rivaud entities was cancelled amidst regulatory motion after points with the independence of 1 skilled and the methodologies utilized by their substitute

- Profitable litigation has taken place towards Bolloré forcing an AMF mandated takeover provide[7] for the “minority” 70% of Vivendi since Bolloré has been deemed to have managed Vivendi on the time of its break up; Bolloré is interesting this determination within the French Supreme Court docket in late November 2025 and

- Left wing celebration assist required to take care of the ruling French Authorities are pushing for a 2percentpa wealth tax which is clouding the outlook for French firms, particularly these beneath household management.

Over the previous yr, Bolloré shares have fallen 19.5% giving up €1.3billion of capitalisation (assuming elimination of self-control loop – henceforth SCL) regardless of the one main mark-to-market destructive being the €420million pro-forma in Vivendi. While disappointing, the biggest fairness funding – 338milion Common Music Group shares value ~€8.3billion have barely moved in worth, however are literally up €360million, not fairly offsetting the diminution in Vivendi[8]. The Group has spent cash on buybacks and, while marginal to valuation, the vitality distribution enterprise has improved.

We estimate that Bolloré has suffered round €1.2billion of “ranking” decline since 30 September 2024 moderately than attributable mark to market loss from declining share costs. The diminution in ranking, exhibited by a widening {discount} to NAV, now up at 40-70% (see under) in our view may be attributed to investor unease over the company errors over the interval, supplemented by:

- the completely ludicrous Louis Hachette Group construction the place the possession of the important thing asset, Lagardère, is break up between 4 events – Louis Hachette Group (AHLG.PA) with 66.5%, Vivendi (13.3%), Qatar Funding Holding (11.5%) and minorities (8.7%)

- this has a direct influence on Lagardère (flat over one yr) being de-rated towards the key cohort inventory, Avolta (AVOL.SW) which has appreciated 20% (CHF 35.80 to CHF43.06) regardless of each firms performing properly in a useful journey retail surroundings

- lack of latest buybacks by Bolloré itself and

- the time required to conclude the Canal+ acquisition of MultiChoice in South Africa – this example and the ridiculous Hachette construction suggests a degree of injudicious impatience not beforehand noticed inside Bolloré.

|

at 30 Sep 2025 |

shares |

value |

Worth €mn |

Worth 30/9/24 |

|

|

Canal+ |

302 |

€2.80 |

817 |

} 3,110 } } |

Canal+ £2.45 |

|

Louis Hachette |

302 |

€1.54 |

465 |

||

|

Havas (OTC:HAVSF) |

302 |

€1.57 |

474 |

||

|

Vivendi |

302 |

€3.00 |

906 |

||

|

UMG |

338 |

€24.56 |

8,301 |

7943 |

|

|

Rubis (OTCPK:RUBSF) |

6.2 |

€31.78 |

197 |

152 |

|

|

LISTED |

11,160 |

11,206 |

|||

|

Vitality |

492 |

492 |

9.1x EV/EBITA |

||

|

Bigben |

10 |

10 |

|||

|

Socfin |

290 |

290 |

|||

|

TOTAL |

11,952 |

11,998 |

|||

|

Money |

5,530 |

5,763 |

Purchase again, purchases FMONC, ARTO |

||

|

Company |

(700) |

(700) |

€70mn at 10x |

||

|

NET VALUE |

16,782 |

17,061 |

|||

|

Shares |

1,115 |

1,135 |

|||

|

€15.05 |

€15.03 |

||||

|

Sofibol construction |

4,688 |

4,035 |

Reinstate self-control loop |

||

|

TOTAL |

21,470 |

21,096 |

|||

|

Shares |

2,804 |

2,836 |

|||

|

€7.66 |

€7.44 |

Permitting for share purchase backs totalling €177million (€115million Bolloré, ~€62m FMONC and ARTO) we consider “worth” has fallen by solely round €100million over the yr, towards a SCL adjusted decline in market capitalisation of €1.3billion (€1.17/share) – a de-rating of ~€1.2billion.

Progress at Bolloré is more likely to be gradual forward of a 25 November 2025 French Supreme Court docket date the place Bolloré will enchantment the AMF’s determination on 18 July 2025 to implement a Paris Court docket of Attraction ruling that it managed Vivendi and mandate a takeover provide inside six months.

Probably the most weird facet of the authorized case is the motivation of the unique plaintiff, CIAM, a so-called “activist” fund supervisor with a small estimated 3.3mn share stake in Vivendi on the time of the break-up. We are able to’t see any “shareholder worth creation” though CAIM’s lead counsel appears to have scored himself a profitable new job[9]– possibly that was the motivation?

Within the occasion Bolloré loses its enchantment and is required to make a money provide for Vivendi, primarily based on our tough evaluation of Vivendi NAV (€4.20) Bolloré can be up for ~€3.4billion (~704million shares) and assume €1.77billion of Vivendi debt, taking an enlarged Bolloré right down to ~€400million in internet money. Furthermore, Bolloré would have monumental €12.4billion direct publicity to UMG, which we consider, from previous feedback, is a place with which they might be immensely uncomfortable and search to mitigate. The blowout in {discount} to NAV clearly displays the distinction between investor view of money and an excellent bigger assortment of strategic positions. We keep our place, with an apparent “hedge” in Vivendi.

Exor: assessing the personal holdings for a clue to the long run.

Exor is the Amsterdam-listed holding firm of the Agnelli household, who personal 55.2% of the financial curiosity, however management over 85% of the voting rights. Their personal possession automobile, Giovanni Agnelli BV (GABV) has round 100 shareholder-descendants of the eponymous Fiat[10] founder, who died in 1945. The household have been absent from Fiat’s management for twenty-years between 1943 – 1963 till the return of Giovanni’s grandson, Gianni as President from 1966. Upon Gianni’s retirement, in 1997, the son of his of daughter Margherita, from her first marriage, John Elkann, was chosen as inheritor to the household fortune. Elkann owns 60% of an intermediate firm, Dicembre, along with his siblings Lapo and Ginevra (20% every)[11]. In flip, Dicembre owns 40% of GABV having purchased out numerous members of the broader household.

Exor SA was an asset-rich French holding firm managed by the French-Greek Mentzelopoulos household. Exor itself managed 35.5% of Supply Perrier, the water model, the well-known Château Margaux vineyards plus an array of French workplace properties. Having acquired a core stake from the Mentzelopoulos household, Agnelli’s IFI Worldwide (IFINT) funding automobile in November 1991 moved to take management, and the 2 firms merged in 1993 to create Exor Group, listed on Luxembourg Inventory Trade. The intervening interval was one in every of nice company battles with Nestlé for management of Perrier, then scandalised by benzene contamination, however finally ceded by Exor SA in March 1992 for a US$960million payday (and US$200million revenue).[12]

In November 1998, the predecessor of GABV launched a takeover provide for Exor Group, successfully leaving the corporate as 90.4% Agnelli’s (by means of totally different autos) and 9.6% Corinne Mentzelopoulos. In March 2003, Exor Group offered its 75% of Château Margaux to Mentzelopoulos.in alternate for her holding in Exor Group ($440million value on the time)[13]. IFI reorganized the sale of its Exor Group shares in March 2006.

In September 2008, the Agnelli’s commenced a undertaking to merge the assorted funding arms of the household: IFI – the last word holding firm – and its 62% subsidiary IFIL (holding monetary belongings) – was duly consummated on 1 March 2009, beneath a brand new holding firm: Exor SpA, the third iteration of the Exor title, which turned Exor NV on the transfer to Netherlands in 2022.

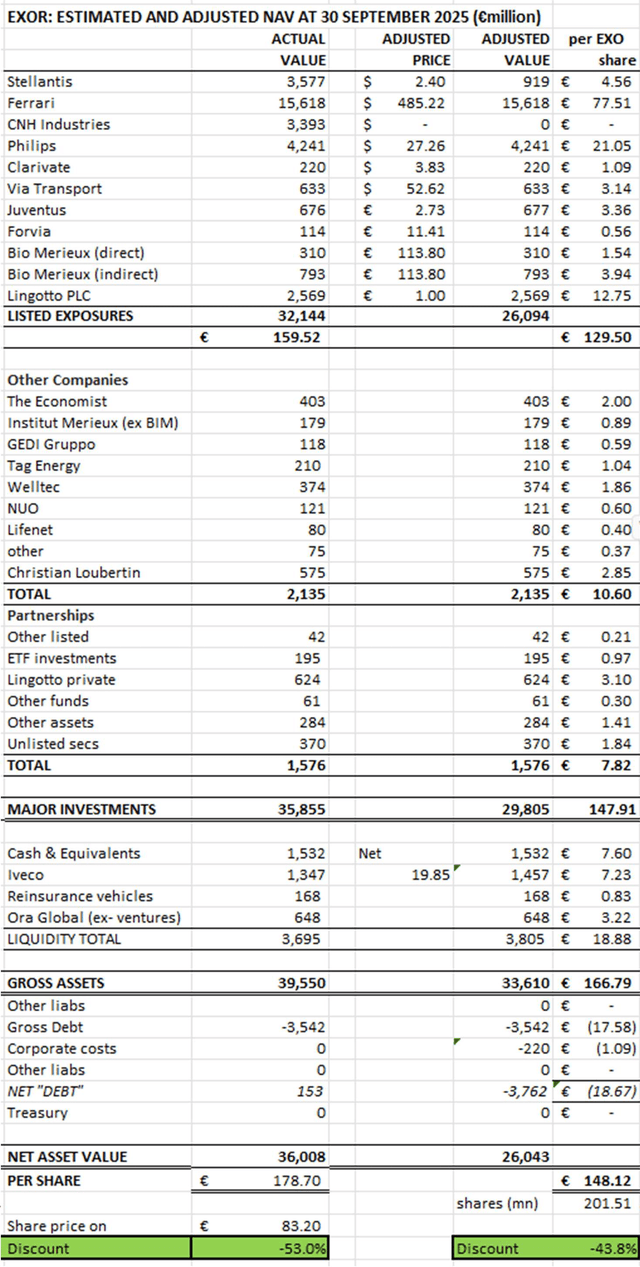

Elkann’s totally admirable tradition of capital administration, compliance and disclosure – and funding expertise – have produced exemplary long-term efficiency: 17.1% compound progress in NAV for simply over 16.5 years. Taking account of dividends, and our personal estimated NAV (earlier than any changes) at 30 September 2025 of €178.70, traders initially have seen a compound internet asset worth return of 18.3% pa, and with a detailed in {discount} from 59% to 53%, whole share return of 20.8% pa.

In fact, ought to traders want to seize all of this, they will’t, and have to just accept a ridiculous {discount} to NAV of ~53% – accepting that the majority would have purchased at a large {discount} to NAV in any case.

Even dead-in-the-water European holding firms who contract out selections on their capital to others don’t commerce at that degree of {discount}. It is a firm the place even handed capital administration has been a key contributor to NAV progress, together with two years of ~€1billion share buybacks in 2023 and the present yr.

Exor has decreased treasury adjusted share capital from 240.9million shares in March 2009 to the present 201.5million, regardless of ESOP points. This has been achieved by shopping for again 54.1million shares over 16 years at a median value of €54.10 (a 70% {discount} to present NAV) however reselling 12million in 2015 at €42.60 (whose acquisition value on the time was €15.32). Previously three and a half years, Exor has stepped up the tempo of buybacks because the {discount} to NAV has widened, having spent €2.5billion to repurchase 30.7million shares or ~13% of the corporate at ~€81.45 or about half NAV.

Having modified to a Dutch holding firm and Amsterdam itemizing in 2022, Exor transitioned to “funding entity” reporting in 2024 to take away the analytical complexities of deconsolidating publicly-listed “industrial” companies to derive a internet asset[14] worth. Exor’s NAV is now absolutely audited on this new clear foundation.

Considerably unusually, the higher the transparency, the higher the {discount} to NAV. The creator’s expertise over time is that reductions to intrinsic worth of investment-type firms typically widen out as slender bull-markets with sturdy thematic influences – resembling exists at current – method their zenith. In order that facet of Exor isn’t any shock. The hefty place to begin, and the persistent “concern” which pervades investor views on Exor (too concentrated, Ferrari is simply too costly, the unlisted bits are opaque, and so forth) is clearly at odds with how comparable traders view securities within the expertise a part of the fairness house.

We consider that it has been forgotten that on a see-through foundation Exor has publicly quoted investments, at costs prevailing on 30 September 2025, equal to €159.52/share, unlisted companies of €22.47 and pro-forma internet debt of €553million after the Iveco deal or €2.75/share. Permitting a 25% {discount} to marketplace for the listed element and 40% for the personal/unlisted piece, suggests a fairer buying and selling value for Exor ought to be round €130/share moderately than the prevailing €83.

However, is that this bearish sufficient? While on this piece, it’s not our intention to deeply analyse and assess the main holdings of Exor – Ferrari, Stellantis, CNH and Philips – valued at over €27billion, of which the primary three have shaped a part of Exor (in some type) because the trendy entity was incepted. In our view, it’s extra fascinating to take a look at among the peripheral investments to judge whether or not they can develop strongly to grow to be “core” or if they’re “lifeless” cash and worthy of the 50%+ NAV {discount} presently ascribed to Exor fairness. Ought to they be freed up and the proceeds use to purchase again but extra fairness?

However we are able to’t gloss over Stellantis and CHNI; a ten% transfer of their share costs modifications the quoted worth of Exor’s holding of every of those companies by €350million – €400million (€1.75 – €1.99/share) and that each are topic to main structural challenges at current. Stellantis has the EV transition challenge accompanied by trying to optimise manufacturing location for tariffs, in addition to enter prices, at a value of €1.5billion within the present CY2025. Current administration modifications try to painting a basing out of the enterprise, primarily in Europe, with improved market share, and an “early stage” restoration in North America. Stellantis has €9billion of internet money in its industrial division (debt is actually within the automobile financing element) towards a present market capitalisation of €23billion.

CNH is very depending on Agriculture (80% of gross sales versus 20% development) and on North America – ~43% of whole gross sales and ~37% of agriculture gross sales. Crop volumes within the present yr throughout most US agricultural commodities are affordable, and while some costs are down, the declines should not catastrophic. The difficulties are twofold: retaliatory motion by shoppers in sure markets, most clearly China which has stopped shopping for US soybeans, and the worth of imported fertiliser – enter prices have risen sharply crimping farmer money circulate. Consequently, H1CY25 gross sales of agriculture gear in North America fell 32% on the corresponding interval. While the US administration is providing new help and funds from the applied tariffs, there are an extra three years of potential ache to navigate.

To reach at extra conservative see-through numbers, we recategorise investments equal to €19/Exor share which have every day market-to-market traits, as follows:

- Place the just lately listed By way of Transportation within the giant scale listed class;

- Mark Stellantis and CNHI to even decrease costs of €2.40 (money/share) and 0 respectively;

- Seperate Exor’s see-through share of Institut Mérieux holdings of bioMérieux (BIM.PA);

- take away Forvia (previously Faurecia) to this class;

- allocate the Exor holding of Lingotto public fairness funds to this space;

- recategorise Iveco to money primarily based on a possible two stage take-out of €5.75/share particular dividend from the sale of defence and the following takeover by Tata Motor at €14.10 per share, yielding €1.45billion to Exor;

- place different identified divestments in money; and

- capitalise Exor company prices, which presently run at an annualised €22million – lower than 6bp of gross belongings.

Assessing Exor’s key unlisted belongings

We consider seven parts of Exor’s unlisted publicity are value of remark:

- Lingotto, the funds administration enterprise which has had a stellar first few years with value-adding contributions from investments we wouldn’t typically affiliate with Exor;

- Institute Mérieux the place the worth of the publicly listed bioMérieux is being supplemented by fascinating strikes within the meals testing subsidiary;

- Ora World, the place the funds are being wound down;

- Christian Louboutin – which stays opaque;

- The Economist the place the biggest holder of 1 class of voting share is now a vendor, which is able to guarantee Exor has a severe determination to make on the funding;

- Welltec, an distinctive enterprise however the place earnings have peaked in the intervening time; and

- TAG Holding, a green-energy publicity with credentialled companions.

In whole, these seven exposures are carried at €6.38billion or €31.73/share within the Exor books at 30 June 2025. All characterize, in numerous methods, the hallmark of Exor: collaboration with credentialled consultants and completed people within the related space.

Lingotto – aggressive public equities administration

Lingotto[15] is a public markets and personal fairness supervisor with a historical past courting again to 2021, however formally based in 2023. This enterprise has belongings beneath administration of US$8.2billion of which Exor is the useful proprietor of some US$3.7billion (€3,193million at 30 June 2025) suggesting exterior capital of US$4.5billon.

Lingotto’s three public firm funds have a greater than helpful monitor document in whole. Exor’s publicity to them is tabulated under – figures in €m:

|

Begin date |

Interval |

Begin funds |

Invested |

Return |

Finish funds |

Est. return |

|

31 Dec 21 |

2022 |

337 |

615 |

116 |

1068 |

18.0% |

|

31 Dec 22 |

2023 |

1068 |

325 |

342 |

1736 |

27.8% |

|

31Dec23 |

2024 H1 |

1736 |

– |

222 |

1,958 |

12.8% |

|

30 Jun 24 |

2024 H2 |

1,958 |

– |

275 |

2,233 |

14.1% |

|

31Dec24 |

2025 H1 |

2,233 |

– |

336 |

2,569 |

15.0% |

|

Cumulative |

337 |

940 |

1,291 |

2,569 |

123.2% |

The newest six-month interval was pushed by exposures to treasured metals and huge scale positions in Carvana, Paramount World and Teva Pharmaceutical, the generic drug producer; assuming that the personal funds are completely Exor, we estimate the general public fairness funds maintain round US$7.5billion of investments at 30 June 2025; our estimate of the ten largest US-listed weightings as at 30 June 2025 and six-month value return to 30 June 2025 are as follows:

|

est weight |

return |

est weight |

return |

||

|

Carvana (CVNA) |

17.0% |

+65.7% |

Concord Gold (HMY) |

3.4% |

+70.2% |

|

Paramount World |

8.8% |

+23.3% |

Sibanye Stillwater (OTC:SBGLF) |

2.7% |

+118.8% |

|

Teva Pharma (TEVA) |

6.3% |

-24.0% |

Van Eck Junior Gold miners (GDXJ) |

2.3% |

+58.1% |

|

Vary Sources (RRC) |

3.9% |

+13.0% |

Valaris (VAL) |

2.1% |

-4.8% |

|

Veon Restricted (VEON) |

3.7% |

+14.9% |

Novagold Res. (NG) |

1.9% |

22.8% |

Supply: East 72 Administration P/L estimates from 13-F filings

A lot of these securities are wildly totally different to these sometimes owned by Exor and so characterize an intriguing, if within the creator’s view, barely wild diversification choice.

Institute Mérieux: credibly valued

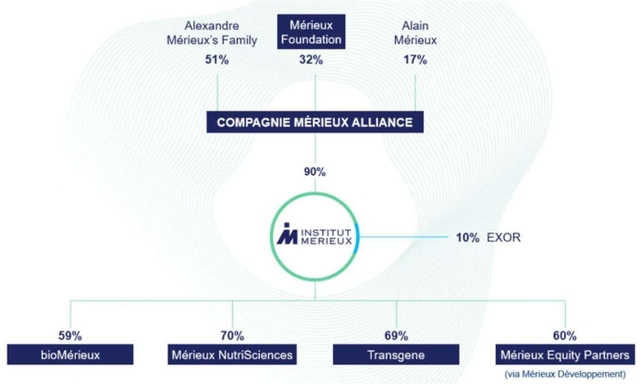

Exor is the only real non-Mérieux household shareholder within the enterprise, which has 4 strands:

The worth of Institut Mérieux is dominated by its 59% controlling shareholding of bioMérieux (BIM.PA), a French-listed diagnostic enterprise capitalised at €13.5billion, during which Exor additionally has a small direct minority holding. Exor’s 10% stake in Institut Mérieux values 100% of the fairness at €9740million with the shareholding in BIM having a present market worth of €7,955million – Exor acknowledge the stake is over 80% of the worth of Institut Mérieux. BIM is immensely worthwhile with gross margins round 56% on revenues of ~€4.1billion. BIM generates annualised free money circulate of ~€440million and carries negligible debt leaving the securities priced at a free money circulate yield of ~3.25% and P/E of 24x – becoming for a top quality testing and options enterprise.

Institut Mérieux doesn’t publish monetary reviews, so the extent of monetary debt is unknown, however is unlikely to be consequential. Transgene (TNG.PA) is a €150million market capitalised listed vaccine designer with numerous merchandise on the scientific trial stage.

By deduction, the remaining belongings inside Institut Mérieux may be ascribed a carrying worth of €1.68billion. The funds administration enterprise – Mérieux Fairness Companions – manages €1.5billion throughout numerous enterprise funds; it’s unclear the extent of the funds’ principal element.

Probably the most fascinating “hidden” a part of Institut Mérieux which might add important worth over the subsequent 2-3 years is the 70% owned Mérieux NutriSciences, with the remaining holding break up 15.4% with Sofina (SOF.PA) the French listed personal fairness investor and 14.6% by Groupe Industriel Marcel Dassualt, the household holding firm of the €22billion Dassault Aviation army jet, Falcon jets and different associated aviation providers. In September, Mérieux NutriSciences closed the acquisition of the worldwide meals testing enterprise of Bureau Veritas for an enterprise worth of €360million (revenues of €133million) and now claims to have a meals testing enterprise with international revenues of €1billion throughout 140 laboratories. Testing companies – throughout the spectrum resembling these within the public area are typically extremely priced, with EV/revenues of ~ 3x (viz BIM itself, this acquisition, Australia’s ALQ, and Switzerland’s SGS[16]) suggesting that the implied carrying worth of 100% of Mérieux NutriSciences is a most€2.4billion, which contextually seems very affordable, with prospects for valuation accretion.

Ora World

Ora World is an unbiased supervisor established by Noam Ohana, who ran Exor Ventures. Ohana is operating the Exor portfolio independently however Exor have famous” that the fund is transitioning in direction of worth realisation”[17]

Christian Louboutin

There are not any publicly out there financials on the corporate though a Moody’s report from 2023 instructed annual income of €1.7billion and EBITDA ~€300million. Assuming no debt, at Exor’s implied worth of €2.4billion for 100% of the fairness, this could recommend an EV/EBITDA a number of of 8x. In our opinion, that is unrealistically low suggesting the rumoured figures are incorrect or there may be some degree of debt within the firm. In any occasion, Louboutin operates 150 costly boutiques around the globe suggesting deduction from EBITDA within the type of lease bills can be important. Therefore, we can’t make an actual judgment on carrying worth however notice general weak point within the publicly listed luxurious sector with chosen exceptions resembling Hermes.

The Economist: severe selections to make which have wider ramifications of notion

Exor boosted its stake within the Economist in August 2015 from just under 5% to 43.4% by way of the acquisition of most of Pearson PLC’s stake – a month after the seller had offered the Monetary Occasions to Nikkei. Exor paid £287million for 2 courses of safety, which is very related within the context of up to date occasions.

The Economist was based in 1848 by James Wilson and shares within the enterprise have been held in belief after his demise with a sequence of protections to make sure the independence of the journal. “Possession” modified in 1928 to Monetary Newspaper Proprietors (homeowners of the Monetary Occasions) however established a construction of solely partial voting management with veto rights. After an extra change in possession of the FT’s holding firm in 1945, it was acquired by Pearson Group in 1957, who retained possession for 58years. With the sale of the paper to Nikkei, the stake in The Economist was separated out and dispersed to a small variety of consumers, primarily Exor in addition to the acquisition of treasury shares by the corporate itself, funded by the sale of the long-lasting Economist Constructing in Mayfair, London to Tishman Speyer

The Economist has a peculiar share construction with:

- 1.26million “A” shares who elect 7 of the Board’s administrators;

- 1.26million “B” shares completely held by Exor who elect 6 of the Board’s administrators;

- 17.64million unusual shares (after excluding 5.04mn treasury shares) – no voting on Administrators;

- 100 belief shares that are the last word arbiter on share transactions

Exor owns the “B” shares for which it paid £59.5million in 2015 (£47.22/share) and seven.49million ordinaries, of which 6.3million have been acquired in 2015 for £227.5million (£36.11 per share). The Economist publishes an indicative value per unusual share annually which as at 31 March 2025 was £31.50.

The “A” shares are owned by an elite group of people, together with a variety of previous editors and CEO’s of Economist together with Rupert Pennant-Rea, Andrew Knight, numerous members of the Leyton household, David Sewell Gordon and others together with members of the Cadbury household. Many of those holders are octogenarians, which raises a real challenge. Nonetheless, the biggest holder of “A” shares with 19% (240,440 shares) is Lynn Forester de Rothschild (aka Woman Rothschild) the widow of Sir Evelyn de Rothschild (died November 2022), the previous patriarch of N.M. Rothschild and Sons, the “English” a part of the Rothschild funding banking empire previous to its efficient merger with the French financial institution in 2003. Sir Evelyn was Chair of the Economist from 1972 to 1989.

In September 2025, Woman Rothschild seems to have engaged Lazard to discover choices to promote her stake[18] which the identical article attributes a value of £200million+. While the stake is the biggest “A” share stake – allowing for no shareholder can train over 20% of the vote – it doesn’t carry 20% of financial curiosity for dividend or winding up functions. Therefore, the attributed sale value, at face worth, seems fanciful, when set towards Exor’s agreed transaction for the “B” shares in 2015.

Abridged monetary metrics for The Economist are given under since Exor’s main acquisition in late 2015:

The figures are offered on a seamless foundation and present a moderately mundane sample with 3% CAGR for income over the 9 years, and static working revenue. Income is roughly two-thirds subscribers with round 1.25million presently, of whom two-thirds are digital solely, implying a median value of £196 every year (~US$270 a yr) per subscriber[19]. Subscriber progress is under 3% every year. The enterprise is very money generative, with working money circulate earlier than tax of ~£45million every year (after rental) which assists in servicing the beneficiant dividends. The Economist carries no debt, holds £38million in money, however has £135million of deferred revenue in subscriptions “but to be delivered”.

Exor’s carrying worth of €403 (£352) for 43.4% of The Economist crudely values the fairness at £812million, equal to a P/E of 23x, and a post-tax free money circulate yield (FCF £35million) equating to 4.3%. Bluntly, it’s hardly thrilling and in our opinion, doesn’t have the data-driven pursuits of its erstwhile mum or dad or Information Corp’s Dow Jones. In our view, that limits the extent to which the group has pricing energy sooner or later, regardless of the standard content material.

So for Exor, the choice by Woman Rothschild presents a possible dilemma. Do they appear to barter a pathway to full management, given the age of the “A” shareholder block, primarily based on their pristine popularity as guardians of what’s actually an heirloom? Do they simply purchase out Woman Rothschild and be constrained? Do they appear to divest to a different purchaser in search of full management? Maybe the most important dilemma is for the custodians of the Economist – can they discover a 100% “hands-off” proprietor as Pearson largely have been with Monetary Occasions.

From an Exor standpoint, we’d NOT wish to see additional funding in a scenario the place they’re an efficient guardian of an funding which has grown in worth at under 3% a yr with a ~4% yield. Not what is predicted from a non-public fairness stake, and never a commensurate return for danger. The prevailing valuation, in our view is more likely to be challenged by means of the Woman Rothschild/Lazard course of. Do Exor push for change and attempt to transfer to 100%? Do they promote too? Or sit pat and do nothing. In our view, how that is dealt with – and at what value – has wider ramifications for a way the group’s unlisted investments are considered.

Welltec:

Exor owns 47.6% of Welltec, a Danish-based firm based in 1994 which has dominant international positions (in 2021, 55% and 40% international market shares respectively)[20] in two area of interest areas:

- Robotic options for the cleansing, restore and upkeep of oil wells; and

- Metallic expandable isolation plugs and packers.

Welltec are additionally creating options for inexperienced vitality geothermal and carbon seize house.

Exor’s main co-shareholder is 7-industries, a household workplace of Ruthi Wertheimer, who was a beneficiary of the 2 stage divestment of precision slicing device firm IMC (Iscar) to Berkshire Hathaway in 2006 (80% for $4billion) and 2013 (20% for $2.05billion) based by Stef Wertheimer in 1952. After buying the holding of Welltec founder Jørgen Hallundbæk in June 2021, the 2 primary holders personal 95% of Welltec fairness.

Paradoxically, Welltec’s profitability has grown sharply since Exor/7-industries moved to 95% possession. The enterprise clearly has extremely cyclical elements, depending on oil firm working and improvement expenditures, which have oil value stimulants but additionally value saving and hydrocarbon extraction elements. Welltec has additionally benefitted from the reimbursement of debt since 2020. The principle debt is publicly issued US$ 8.25% senior secured notes (which is why Welltec has public annual reviews); US$325million of principal was issued in October 2021 – successfully representing internet debt on the time. By means of important revenue progress and sensible capital administration, Welltec has redeemed and acquired again practically half of those notes, and when offsetting US$103million of money, carries internet debt of solely US$59million at finish 2024.

Welltec’s abridged historic earnings are proven under:

Supply: Welltec firm reviews, Denmark CVR

Based mostly on outcomes for publicly listed cohort firms, it’s clear that exercise has doubtless reached a zenith in the intervening time given a range-bound oil value. Exor famous Welltec revenues at $212million in H1CY25 – roughly flat – however decreased the valuation of their fairness stake to €375million (US$440million).

Broad {industry} leaders Schlumberger (SLB; market cap US$53billion) and Halliburton (HAL, $21.4billion) commerce at a blended EV/EBIT of 8.2x CY2024 historic earnings, a peak for the present cycle. SLB trades at 9.6x however HAL – extra cyclical with a 30% EBIT decline forecast in CY2025 – a decrease 6.7x.

Exor’s carrying worth ascribes an fairness worth of $926million to Welltec and EV of ~$986million, pricing EV/EBIT at a 5.9x a number of, under both of the publicly traded cohort firms. In our view that’s contextually affordable. In time, in our opinion because the cycle strikes to a extra beneficial surroundings, Exor might look to exit the funding.

TAG Holding: one other affiliation with sturdy {industry} gamers

The company construction of TAG Holding (TAGH), of which Exor personal 44.9% at a three-stage value of €212million (€100million in 2023, €89million in 2024 and €23million in 2025) is sadly not absolutely clear. We consider[21] the one different shareholder of TAGH is Impala SAS, an entity managed by Jacques Veyrat, who in mid 2024, offered his 42% stake in Neoen to Brookfield for €2.5billion, when Neoen was acquired for €6billion fairness worth. Veyrat famously acquired the belongings as a part of an exit settlement with Louis Dreyfus Commodities in 2011[22].

In flip, we consider TAGH owns 44% of Tag Vitality (TAGE), with the residual 56% break up equally between two personal fairness fashion traders: the Nataxis affiliate Mirova by way of its Vitality Transition Fund and Omnes, a French PE agency considerably invested in vitality transition by means of its Capenergie #4 fund.

TAGE owns the biggest Southern Hemisphere windfarm close to Geelong (Vic, Australia) with capability of 1.33GW when absolutely full in 2027 at a value of $4billion however has offered a 15% stake of the stage 2 a part of the undertaking. TAGE additionally has a serious battery storage undertaking in France, a 100MW battery facility in Northern England , JV on a 50MW battery in Scotland and tasks in Spain and Portugal.

No public financials can be found on TAGH or TAGE.

What may shut the Exor {discount}?

In our view, Exor suffers from triple-discount elements:

- European funding holding firm syndrome, the place reductions within the sector are routinely 40%+ aside from Investor AB, the Wallenburg managed entity;

- The sturdy affect of Ferrari (RACE), which nonetheless represents ~38% of gross belongings, trades at a ahead P/E of 42.5x reflecting the massive moat of the enterprise and corresponding close to 30% returns on employed capital however the place traders are but to expertise a downcycle in that enterprise since separation in late 2015; and

- 21% of gross belongings uncovered to unlisted entities the place disclosure ranges from absolutely clear to opaque and enterprise from extremely mature (The Economist) to capital intense improvement (TAG Holding)

The primary two elements are unlikely to resolve – we don’t see Exor transitioning to a different kind of entity and the promote down of 4% of Ferrari inventory in February 2025 gained’t be repeated for not less than a yr, and there are actual questions – given historical past – whether or not Exor can be ready to fall under 30% voting rights (20% financial curiosity) presently held.

Therefore, in our view, the closure of the {discount} to NAV has to come back from liberation of capital elsewhere, resembling:

- Discount/sale of Stellantis and CNHI within the subsequent up-cycle – however that’s most likely 3-4 years away;

- Gaining profit from efficiently promoting personal fairness positions at or above guide worth over the subsequent 1-2 years.

Public indications of doubtless divestments of Iveco (€1.4billion), Ora (€648million) and reinsurance autos (€198million) would see Exor be debt free on a pro-forma foundation and the corporate has present undrawn dedicated credit score traces of €675million, suggesting scope to create one other “7.5% – 10%” (€3 – €4billion) main place alongside Philips and Lingotto.

Based mostly on our re-cut see by means of desk of conservative NAV of €148.12 with decrease costs for CNHI and Stellantis, after which attributions of appropriate reductions to non-public and public belongings of 25% and 40%, we view a extra acceptable inventory value for Exor as round €108/share – a reduction of 27% to this lowered NAV, however a close to 30% return on prevailing costs.

Therefore, after being comparatively inactive within the shares for over 12 months, now we have just lately elevated our weighting.

Swatch Group: diving into the inexperienced abyss fifty fathoms under[23, 24]

In a world of quickly altering client tastes, typically in areas the place predictability has beforehand been a key for traders – maybe greatest exhibited in an sudden sharp broad-based decline in alcohol consumption over the previous few years[25]– and consequent disastrous efficiency of the model homeowners, predicting future style developments isn’t any simple activity.

The problem of development prediction is aggravated by the outsized contribution of the Chinese language client to many of those markets. Such shoppers are topic not solely to financial forces – which have largely been destructive over the previous three years – but additionally altering demography which is arguably eradicating the structural progress story which existed twenty years in the past.

2024 represented the third consecutive yr of Chinese language inhabitants decline, the quantity mired at round 1.4billion. India, which supplanted China in 2021, now has a inhabitants of 1450million, nonetheless rising at just under 1% every year, is a really totally different client/style market.

Many of those modifications appear to have all of a sudden rushed to the forefront of traders’ considering in 2025, regardless of being obvious for a while prior. Share costs of broad-based luxurious items firms have been weak over the course of the previous 21 months, with solely these centered on ultra-luxury manufacturers and product with ultra-disciplined administration (eg CFR, Hermes) or company points of interest staying out of the mire:

|

31/12/23 |

YTD |

peak |

31/12/23 |

YTD |

peak |

||

|

Swatch (OTCPK:SWGAF)(OTCPK:SWGAY) |

-32.3% |

-7.3% |

-74.2% |

Tapestry (TPR) |

+203.4% |

+71.8% |

-3.2% |

|

LVMH (OTCPK:LVMHF) |

-25.7% |

-17.2% |

-40.4% |

Zegna |

-14.9% |

+16.4% |

-40.5% |

|

Kering (OTCPK:PPRUF) |

-26.2% |

+20.8% |

-61.2% |

Prada (OTCPK:PRDSF) |

+10.2% |

-24.4% |

-31.6% |

|

CFR |

+35.1% |

+11.4% |

-17.2% |

B. Cucinelli (OTCPK:BCUCF) |

+10.0% |

-11.1% |

-26.3% |

|

Moncler (OTCPK:MONRF) |

-6.4% |

-1.1% |

-26.9% |

Ferragamo (OTCPK:SFRGF) |

-54.8% |

-20.3% |

-82.0% |

|

Hermes |

-10.8% |

-9.1% |

-25.1% |

Hugo Boss (OTC:HUGPF) |

-37.3% |

-7.8% |

-64.0% |

|

Burberry (OTCPK:BBRYF) |

-15.0% |

+20.3% |

-55.3% |

AVERAGE† |

-14.0% |

-2.5% |

-45.4% |

† excluding Tapestry

On this risky surroundings, why would we ponder investing in a wristwatch firm? Isn’t the {industry} lifeless, supplanted by smartwatches, smartphones and AI expertise? In our view, moderately like particular person segments of the alcohol market (eg champagne however undoubtedly not cognac) watches are a ubiquitous element of the jewelry market. They characterize every part from a standing image, are sometimes fungible, normally collectable, and a desired self-appreciative mark of feat, supported by among the smartest (and largest) advertising and marketing, sponsorship and promoting budgets on the planet. Smartwatches could also be extremely helpful however they aren’t essentially the requisite piece of jewelry with which to decorate up.

Swatch Group is the world’s second largest watch producer by income, solely behind the privately owned Rolex. It owns sixteen separate watch manufacturers starting from the best finish Breguet, Blancpain, Harry Winston and Glashütte Authentic by means of the biggest three manufacturers Omega, Longines and Tissot right down to entry degree Swatch and flik-flak. Swatch owns 13 separate manufacturing companies, 4 digital techniques companies, and an impressive property portfolio. The corporate is a veritable treasure trove of 145 separate entities.

However within the prevailing softer surroundings, it has remained a mounted overhead primarily based firm, pushed by the need of the controlling Hayek household to take care of manufacturing expertise inside Switzerland, a throwback to their father’s institution of the corporate from the close to ruins of the Swiss watch {industry} within the early to mid 1980’s (see later). Swatch’s mounted overheads run at round CHF5.1-5.3billion every year, together with ~CHF1billion in advertising and marketing prices.

So, in easy phrases, to forecast earnings includes putting in a income assumption set towards an 80-83% gross margin on high. Therefore, the sharp focus, beneath this technique, needs to be on revenues, pushed both by the {industry} surroundings – presently risky – or swings from the corporate’s personal advertising and marketing initiatives.

Swatch has two courses of shares: bearer (UHR.SW CHF149.15) and registered (UHRN.SW CHF30.40). The corporate’s 28.741million bearer shares[27]– successfully being FIVE registered shares however with just one vote – personal 55.5% of the financial capital versus the 115.128million registered shares. Nonetheless, with each courses of share having one vote, the controlling Hayek household (see under) exerts 44.6% voting management by means of possession of 63.45million (55%) of the registered shares and 836k (2.9%) of the bearer shares excluding treasury inventory (64.3m votes of 143.8million).

In a very Swiss quirk, due to the Hayek possession, the upper priced bearer shares are much more liquid than the decrease priced registered securities, buying and selling 3– 4TIMES extra securities per day, regardless of the nominal value being 5 instances increased. Within the curiosity of readability, within the evaluation which follows, now we have notionally transformed the registered shares to bearer shares to offer an efficient financial capital construction of 51.767million securities, or an fairness market capitalisation of CHF7.7billion.

Swatch shares are down some 75% from their document excessive of ~CHF600 in late 2013 and after a robust restoration from excessive COVID lows of CHF 126 in March 2020 to a March 2023 excessive of CHF343, a confluence of destructive elements has seen a 55% decline from that degree.

Previously two and a half years, the enterprise has been impacted by:

- a collapse in Chinese language client demand, together with for watches;

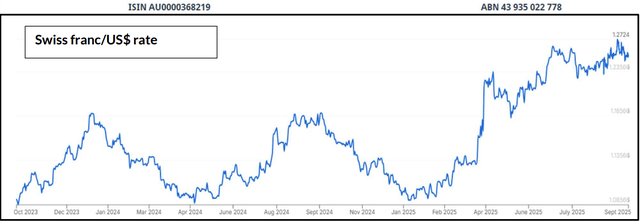

- the power of the CHF towards just about all currencies, together with a 26% achieve since late 2023 towards the US$, rising the efficient value for the articles;

- administration determination to take care of full staffing of Swiss manufacturing services, which misplaced CHF150million within the six months to 30 June 2025 regardless of decreased demand[28]; and

- ensuing collapse in working revenue from CHF1.19billion in CY2023 to CHF68million within the first six months of 2025.

In respect of Swatch shares, the influence of those exterior elements and inside selections – mentioned under in additional element – has arguably been exacerbated by:

- public disagreements between analysts and the controlling Hayek household patriarch;

- a patronising (in our opinion) dismissal of an exterior board candidate;

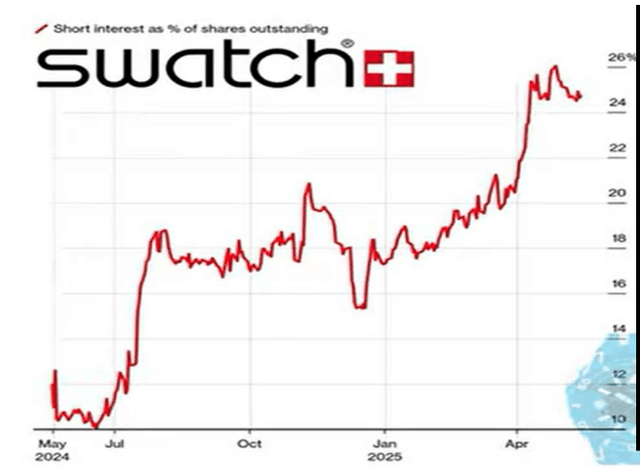

- important quick promoting leading to Swatch changing into the second largest quick sale publicity throughout European equities in August 2025;

- unsure influence (or sustainability) of 39% US tariffs imposed efficient 7 August 2025; and

- present lack of response to the USA by arguably timid Swiss politicians.

|

“We promote watches, not shares. What counts for us is the long-term improvement of the corporate, not the short-term nature of the share value” Why don’t you delist the Swatch Group? “Hallelujah. This will surely be greatest for the long-term improvement of the corporate. However sadly going personal shouldn’t be potential with out us taking over huge debt. And we don’t like debt in any respect.” 29 |

In fact, the big quick place could be seen as an actual attraction, particularly set towards an ungeared steadiness sheet and undoubted crude asset worth traits of the shares at prevailing ranges:

|

CHF million at 30 June 25 |

decrease |

low |

remark |

|

Internet money and monetary belongings |

1,089 |

1,089 |

money 1,031; monetary belongings 245, debt (187) |

|

Internet receivables |

357 |

357 |

|

|

Properties at historic value/worth |

2,986 |

4,000 |

per administration feedback (see later) |

|

Estimated uncooked materials element of stock |

640 |

640 |

|

|

TOTAL |

5,072 |

6,086 |

CHF98/share; CHF117.57 |

If these “scorched earth” figures are appropriate – and Swatch did commerce near the “low” (not decrease) certain on “Liberation Day” in April 2025 – on the Swatch value on 30 September 2025, the sixteen manufacturers + CHF3.9bn completed stock and IP are valued by the inventory market at CHF1.65bn – CHF2.66bn (US$2.1bn – US$3.4bn). Provided that Harry Winston alone value US$1bn in January 2013, and the “value” consists of the world’s third largest particular person watch model – Omega – this seems incongruously low.

The uncooked materials stock determine takes account of lower than 10% of whole stock and excludes semi-finished and accomplished items; on condition that completed items sometimes account for ~50% of guide worth stock – so ~CHF3.7billion at 30 June 2025 – and are offered at a gross margin averaging a comparatively steady 79% over the previous 28 years, producing an implied income of over CHF18billion, albeit that’s some three years gross sales at present charges – the margin of security embedded inside Swatch securities is critical.

Is the watch {industry} lifeless?

Switzerland is 5 instances larger than another watch exporting nation, with just below US$30billion of annual exports, in comparison with Hong Kong’s US$6.3billion and Mainland China’s US$5bilion in CY2024[30]. Therefore, Fédération de l’industrie horlogère Suisse (FIH) month-to-month statistics of Swiss exports by area, value level and in whole are important influences on investor sentiment surrounding the sector. Mechanical watches account for under ~35% of exports by models, however ~86% of export worth.

Swiss watch exports are an distinctive microcosm of THE international development of latest years: the wealthy get richer. Within the 24 full years because the flip of the millennium, Swiss watch exports have:

-

- halved in models shipped from 29.6million to fifteen.3million;

- seen their worth rise from CHF9.3billion to CHF24.8billion;

- the common export value per watch improve from CHF313 to CHF1618 (9.4percentpa); and

- models within the above CHF3,000/piece class improve four-fold or 6.1% every year

Structurally, it’s clear the {industry} shouldn’t be lifeless, however over the previous 3-4 years, progress has slowed to a crawl, even within the increased priced classes. The danger is, in fact, that the imposition of such hefty tariffs on the biggest export market – USA – which represented ~16.5% of exports in 2024, when added to the decline in China, represents a much bigger hurdle over the subsequent few years.

This month-to-month concentrate on the FIH statistics has been led to by the US tariff regime, which commenced in August, however was flagged prior. Consequently, important shipments have been made to the US upfront, inflating the July statistics. The August statistics, have been comparatively weak, as anticipated, compounded by an obvious fallback in China. Swatch CEO Hayek has been extra optimistic concerning the scenario for the corporate in a latest advert hoc briefing.31

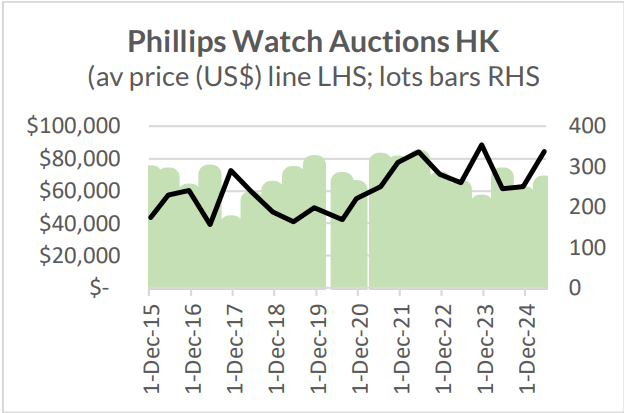

There are indicators, nevertheless, that Asian watch markets might be basing out, and in a style that implies Swatch should place higher emphasis on their highest value fashions within the Blancpain, Brequet and “area of interest” manufacturers. Now we have tracked each Phillips Hong Kong watch public sale since 2015 – dominated by beautiful items and Rolex, Audemars Piguet, Cartier and Patek Philippe. The newest public sale XX (20) in Might 2025 was energetic (254 tons offered) on the second highest ever common value (US$84,479)[32]

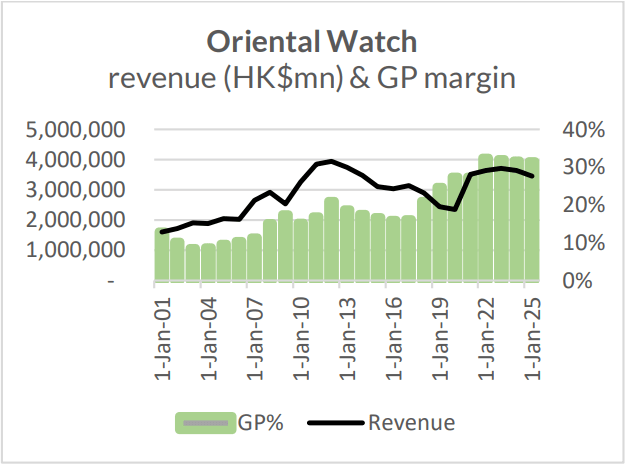

As well as, the 2 listed Hong Kong watch retail firms – Oriental Watch (0398.HK) and Emporer Watch (0887.HK), while not near their 2012-year peaks in income, have each elevated margin considerably. To some extent, this has been to Swatch Group’s detriment as each are closely centered on Rolex throughout the watch class (Emporer has a major jewelry element) and have honed down the extent of their choices. In our view, it once more emphasises the probabilities for Swatch to construct the “status” manufacturers of Blancpain and Breguet inside their choices.

These indicators have been not obvious in Swatch six-month interim outcomes to 30 June 2025, partly because of a really poor first quarter (Swatch doesn’t report quarterly figures). To some extent the H2 CY2024 numbers have been padded by the Paris Olympics timing contracts, with estimated income of CHF140million. Gross sales fell sequentially 7% between H1 CY25 and the prior half yr, completely on account of China and Hong Kong gross sales declines. These areas in recent times have made up 33% of gross sales, fell to 27% in CY2024, and are doubtless under 25% within the present interval. Though prices and stock have been decreased, with a corresponding improve in gross margin, EBITDA fell CHF130mn on the prior corresponding interval from CHF406mn to CHF276mn (by way of CHF314million in H2CY24). Working revenue is a paltry CHF68million in H1 CY2025. Having Better China get well, not simply base out is essential to ahead progress.

Few listed funding options

There are a mere handful of publicly listed wristwatch producers – three “pure” producers the place watches are the predominant product – along with two others the place watches are a part of a wider luxurious group. We haven’t centered on listed watch retailers elsewhere (HourGlass; Watches of Switzerland Group) given their Rolex emphasis and relationship.

|

2024 or 3/25 |

Swatch† |

Seiko33 |

Citizen33 |

Richemont34 |

LVMH |

|

ticker |

UHR.SW |

8050.JP |

7762.JP |

CFR.SW |

MC.PA |

|

Issued Cap |

51.767mn |

40.87 mn |

243.9 mn |

587.9 mn |

497.0 mn |

|

Share value |

CHF149.45 |

¥6,540 |

¥1,003 |

CHF151.60 |

€520.50 |

|

Market Cap |

CHF7,737mn |

¥267.3bn |

¥244.6bn |

CHF89.1bn |

€241.7bn |

|

Market Cap CHF |

7,737mn |

1,440mn |

1,318mn |

89,125mn |

241,693mn |

|

Watch enterprise traits – 2024 – all measured in CHF |

|||||

|

Watch Gross sales |

6,735 |

1,023 |

1,030 |

3,124‡ |

10,075‡‡ |

|

Working revenue |

304 |

120 |

104 |

166 |

1,473 |

|

EBITDA € |

720 |

157 |

144 |

447 |

NA |

|

Working mgn |

4.5% |

11.7% |

10.1% |

14.3% |

14.6% |

|

† transformed onto bearer share foundation ‡ specialist watchmakers phase solely. Cartier provides €3,532mn (CHF3,361mn) at unknown margin in order that whole CFR watch gross sales are solely ~CHF250mn lower than Swatch Group ‡‡ consists of watches (Hublot, TAG Heuer, Zenith) and jewelry (Tiffany, Chaumet, Bulgari) and combos |

What stands out is the very low margin earned within the 2024 yr by Swatch because it maintained a hefty overhead base, towards a major 15% decline in gross sales in 2024. Why does it do that? Historical past.

How historical past guides the corporate

Bluntly, with out the historical past of Swatch Group, comprehension of why the Hayek household run the corporate within the prevailing method is not possible to know.

Swatch is born out of two crises: the final financial disaster of the 1930’s and the precise {industry} difficulties from the late 1970’s. Within the 1930’s the collapse of the worldwide financial system led to the Swiss Authorities and bankers guiding collectively a bunch of 20 motion producers in August 1931 to be mixed as ASUAG[35]. A yr earlier than, in February 1930, the 2 watchmakers Omega and Tissot have been merged to type SSIH[36].

The second disaster within the 1970’s was created by the invention of the quartz motion by Seiko in 1969 for its “Astron” watch. Paradoxically, the Swiss had their very own quartz watch made by Ebauches[37] by 1970, however the {industry} didn’t embrace the brand new expertise of the battery pushed vibrating quartz crystal and caught resolutely to the normal mechanical timepieces. These cheaper creations boomed in recognition which together with the oil value pushed financial disaster of the mid 1970’s, mixed to decimate the normal Swiss watch {industry}, ASUAG and SSIH have been each in important monetary problem and their Swiss bankers appointed a administration guide, Nicholas G Hayek38, to create a strategic plan for the businesses.

Hayek’s plans and execution is the stuff of legend[39]. ASUAG and SSIH have been merged in 1983, facilitating the removing of huge duplication of selling and administration throughout all the manufacturers. Nonetheless, the creation of a brand new “decrease market” watch – moderately than the continuous devaluation of key manufacturers like Omega by means of extension throughout all value factors – was not taken on board by the controlling banks.

This gave Hayek the chance to amass 51% of the merged entity, renamed Société de Microélectronique et d’Horlogerie (SMH) for CHF151million. Contemplating that in 1983, SMH misplaced CHF173million on income of CHF1.5billion, the “gamble” was exceptional. Nonetheless, Hayek’s means to now management immediately as an proprietor facilitated extra radical reform, notably at Omega, slashing mannequin numbers and changing administration. In fact, the brand new “decrease finish” watch to compete globally was “Swatch” –an acronym for “second watch” and encompassing enjoyable and progressive design with a far decrease variety of parts at a sale value of CHF40-50.

Hayek retained the important thing “expertise” of SMH – renamed Swatch in 1998 – in respect of actions and numerous componentry and digital techniques manufacturing. A lot of this emanated from the assorted firms which had merged into ASUAG and SSIH through the years with a particular area of interest or experience, which might be deployed in a wider however nonetheless centered method:

Provenace of present Swatch manufacturers:

|

Model |

Founders |

based |

feedback/acquirors |

|

Blancpain |

Blancpain household |

1735 |

acquired SSIH 1961, offered 1982, re-acquired by SSIH 1992 for CHF60mn |

|

Jacquet Droz |

Droz household |

1738 |

acquired Swatch 2000 |

|

Longines |

Agaassiz |

1832 |

branded/renamed 1867, merged to ASAUG 1971, SMH 1983 |

|

Glasshütte Authentic |

Lange, Schneider, Assmann |

1845 |

Grew to become GUB in 1951 inside East Germany, privatised 1990, reconstituted 1994, Swatch 2000 |

|

Omega |

Brandt household |

1848 |

renamed Omega 1894, merged to SSIH 1930, SMH 1983 |

|

Tissot |

Tissot household |

1853 |

merged to SSIH 1930, SMH 1983 |

|

Breguet |

Brown household |

1870 |

Chaumet 1970, Investcorp 1987, Swatch 1999 |

|

Certina |

Kurth household |

1888 |

acquired ASAUG 1971, SMH 1983 |

|

Hamilton |

numerous |

1892 |

Merger of three American watchmakers 1892, SSIH 1974 |

|

Union |

Dürrstein |

1893 |

closed 1933; model reborn beneath Glasshütte Authentic 1996 |

|

Harry Winston |

Winston household |

1908 |

Swatch 2013 |

|

Leon Hatot |

Hatot household |

1911 |

Swatch 1999 |

|

Rado |

Schlup & Co. |

1917 |

renamed Rado 1950, acquired SMH 1983 |

|

Mido |

Schaeren |

1918 |

acquired ASAUG 1972, SMH 1983 |

|

Swatch |

1983 |

created 1983 “Second Watch” by SMH |

|

|

Balmain |

1987 |

Unique international rights from Pierre Balmain |

|

|

FlikFlak |

1987 |

created 1987 for youngsters by Swatch |

Nicholas Hayek stepped down as CEO in 2003, selling Nick Hayek to the position, and died in workplace as Chairman in June 2010.

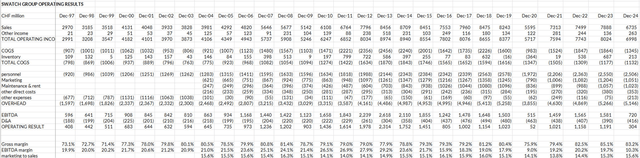

Lengthy-term monetary evaluation

Now we have reproduced chosen historic monetary evaluation for a 27year interval from 1997. That will seem to be overkill, but it surely does illustrate the exceptional stability of quite a few indicators of efficiency throughout the group, led to by the methods of Hayek father and son.

Notably:

- advertising and marketing spends of CHF1.0bn to 1.3bn every year;

- latest overhead bills of ~ CHF5.0bn – CHF5.3bn together with advertising and marketing;

- exceptionally steady gross margin averaging precisely 79% over the interval;

- sturdy management of receivables since 2017, not unrelated to previous selections on provide of actions;

- blow out in stock ranges from the COVID interval onwards, which are actually at a document excessive of practically seven years of which completed good characterize over half; and

- variability of capital expenditure reflecting lumpy acquisitions of properties in numerous years

Swatch Group tends to be about “proudly owning”. Proudly owning works throughout 4 areas:

- completed items stock, particularly the place Swatch Group function their very own shops moderately than a franchise mannequin;

- property – as with different luxurious items firms, Swatch Group needs to bodily personal their shops at chosen strategic areas but additionally owns a major residence portfolio in and round its watchmaking services in Switzerland, in addition to among the buildings themselves;

- vertical integration moderately than insourcing componentry – each Swatch Group watch is comprised close to 100% of in-house manufactured parts, not like many opponents the place motion manufacture is outsourced; and

- different elements of stock with the corporate additionally manufacturing chosen parts elements for third events.

At 30 June 2025, Swatch Group was carrying CHF7.4billion of stock, marginally down on the CHF7.6billion at 31 December 2024. The group doesn’t give a breakdown on the interim outcomes stage however latest historical past suggests a tough 50:50 break up between completed items and different classes (semi-finished, in-progress, uncooked supplies and spare elements) suggesting round CHF3.7billion of precise watches and jewelry.

We estimate Swatch (the model) has round 180 international monobrand shops, that Omega has an extra 300 with Longines and Tissot working round 250 every. Plenty of these shops throughout every model are franchised however there are important numbers of firm operated venues. In H1 CY2025, round 45% of watch and jewelry gross sales got here from the corporate’s OWN retail actions, moderately than by means of wholesalers and different distributors suggesting round CHF1.4billion within the six-month interval. Most notably, the corporate does not franchise the 44 Harry Winston boutiques (not like sure CFR manufacturers) which every carry upwards of CHF20million of stock[40] Therefore, if the supply feedback are correct, some CHF1billion of the CHF3.7billion completed items stock is at simply 44 areas. Some elementary arithmetic by reference to stock suggests many of the monobrand boutiques are firm owned, which might account for the very excessive degree of inventory.

Hidden property belongings

The Group’s property portfolio of land and buildings is carried at ~CHF1.73billion at 31 December 2024, of which funding properties accounted for CHF529million, having been constructed up considerably over the previous ten years. The properties are extraordinarily conservatively accounted for, as may be evidenced from historic and up to date accounts:

- as way back as December 2005, land and buildings have been carried at CHF478million towards historic value of CHF918million as roughly CHF20million every year in depreciation was being utilized towards these belongings (not gear);

- the final time it was disclosed, in 2005, the insured worth of those land and buildings was CHF1,419million – three TIMES their carrying worth and 55% above historic value; and

- depreciation towards land and buildings yearly runs at round CHF70million and reached CHF77million within the 2024 yr

Since 2004, Swatch has selectively acquired or developed important buildings at a value of over CHF800million, for its personal use or for funding functions. Probably the most notable of those constructions are tabulated under:

|

acquired |

constructing |

location |

feedback |

|

2004-2007 |

Nicholas G. Hayek Middle |

Ginza, Tokyo (multi-Swatch model boutiques) |

Previous constructing acquired for CHF150million then redeveloped. Est whole CHF200m |

|

Nov 2014 |

“Peterhof” constructing [INVESTMENT] |

30 Bahnhofstrasse, Zurich[41] |

Constructed 1913, acquired for est CHF400mn from Credit score Suisse. Retail floor flooring (Louis Vuitton, Bongénie Grieder) and workplaces on six flooring |

|

H1 CY2023 |

32-33 Previous Bond Avenue [INVESTMENT] |

West Finish, London |

CHF120mn (1347sqm) rented to Saint Laurent |

|

October 2023 |

171 New Bond Avenue |

West Finish, London |

CHF90million – Harry Winston boutique (562sqm) |

|

October 2023 |

Ave des Champs Elysees |

Paris |

Small, undisclosed, could also be Swatch retailer at 104 solely small a part of constructing. |