Reporting favorable Q1 outcomes this week, Dwelling Depot HD) and Lowe’s LOW) simply gave buyers the identical broad message: The house enchancment market isn’t falling aside, however it’s not accelerating both.

Elevated rates of interest, low housing turnover, and cautious “Do It Your self” (DIY) spending proceed to weigh on massive discretionary initiatives.

The distinction is that Dwelling Depot continues to be leaning tougher into skilled providers for contractors (PRO) and the specialty distribution market, whereas Lowe’s is making an attempt to indicate it will possibly take market share with a extra balanced “Whole Dwelling” technique throughout Professional, on-line, home equipment, house providers, and DIY loyalty gross sales.

Buyers could also be questioning which main house enchancment retailer has the higher strategic strategy and might be poised for a sharper rebound, as a slowdown within the broader housing market has weighed on their inventory performances.

Picture Supply: Zacks Funding Analysis

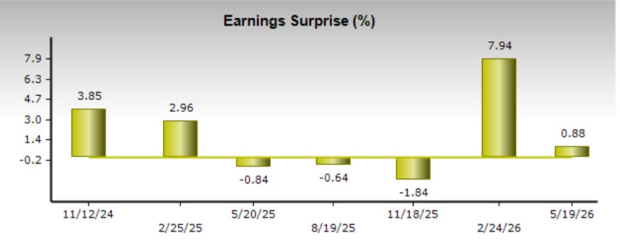

Dwelling Depot’s Q1 Outcomes & Outlook

Dwelling Depot’s Q1 was regular however considerably uninspiring. Q1 gross sales have been up roughly 5% 12 months over 12 months to $41.76 billion, whereas comparable gross sales elevated 0.6%, however adjusted EPS declined to $3.43 from $3.56 a 12 months in the past. The highest and backside line figures exceeded Q1 EPS and gross sales expectations by practically 1%, respectively.

Picture Supply: Zacks Funding Analysis

Notably, Dwelling Depot said demand seemed “comparatively related” to final 12 months regardless of larger client uncertainty and housing affordability stress. Contemplating this, Dwelling Depot reaffirmed its full-year outlook for flat-to-2% comparable gross sales development and flat-to-4% EPS development.

The important thing line from Dwelling Depot’s Q1 name was not the comp quantity; it was the reason. CEO Ted Decker stated Dwelling Depot’s core buyer stays financially resilient, supported by house fairness, employment, wage development, and funding portfolios.

Nevertheless, Decker additionally stated uncertainty is retaining prospects from taking over bigger initiatives, whereas greater charges are holding down housing turnover and new development exercise. In different phrases, Dwelling Depot isn’t seeing a collapse within the house owner, it is seeing delayed ambition.

That creates a nuanced inventory narrative. Dwelling Depot is a high-quality operator with a rich house owner base, sturdy Professional publicity, and a long-term housing-repair thesis. However the near-term catalyst stays muted. Administration explicitly said that it is not relying on a significant enchancment in underlying demand, because the anticipated second-half comp enchancment is essentially tied to a return to regular climate exercise.

Lowe’s Q1 Outcomes & Outlook

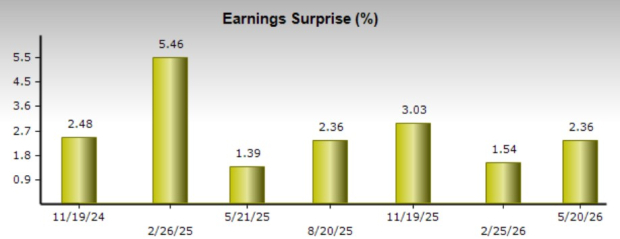

Lowe’s instructed the same housing story, however with a barely completely different emphasis. Q1 gross sales spiked to $23.07 billion, comps elevated 0.6%, and adjusted EPS rose practically 4% to $3.03. The highest and backside line figures exceeded Q1 EPS and gross sales expectations by 2.36% and 0.62%, respectively.

Picture Supply: Zacks Funding Analysis

Lowe’s additionally reaffirmed its full-year steerage for $92 billion-$94 billion in gross sales, which might equate to a minimum of 6% development, with comparable gross sales development anticipated to be flat-to-2%

CEO Marvin Ellison was extra direct in regards to the macro backdrop, calling this probably the most troublesome housing market he has confronted because the monetary disaster. To that time, Lowe’s is extra uncovered to the DIY buyer, which makes the housing freeze extra painful, with administration saying roughly 60% to 65% of income comes from DIY, and about one-third of the enterprise is discretionary.

That issues as a result of the weakest classes stay big-ticket discretionary initiatives, whereas restore, upkeep, alternative, Professional, home equipment, and providers are holding up higher.

Moreover, Lowe’s framed the patron as “Ok-shaped,” as higher-income prospects are nonetheless spending on innovation and modernization, whereas lower-income prospects are extra cautious. That commentary helps clarify why the corporate can publish constructive comps whereas nonetheless sounding cautious, which means the common buyer has not vanished, however spending is being redirected towards smaller, mandatory, or value-driven initiatives.

Dwelling Depot & Lowe’s Strategic Variations

In the mean time, the clearest distinction between Dwelling Depot and Lowe’s inventory is strategic.

Dwelling Depot is constructing a big specialty distribution and Professional ecosystem by way of its subsidiaries SRS, GMS, and Mingledorff’s. This comes as Dwelling Depot has emphasised a $700 billion Professional alternative in a complete addressable market that it says has reached $1.2 trillion.

Lowe’s, in the meantime, is making an attempt to show that its diversification can offset a softer DIY cycle, by way of Professional enlargement, on-line development, house providers, its loyalty program, and final 12 months’s acquisitions of Basis Constructing Supplies (FBM) and Artisan Design Group (ADG). This comes as Lowe’s on-line gross sales grew greater than 15% throughout Q1, and administration says Professional ought to proceed to outperform DIY for the 12 months.

Investor Takeaway

Dwelling Depot nonetheless appears to be like like the higher long-term house enchancment retailer, particularly if its Professional and specialty distribution phase scales as deliberate. Then again, Lowe’s could supply the sharper restoration story if DIY demand normalizes, as a result of its enterprise is extra immediately uncovered to the patron classes which are at present below stress.

Nonetheless, each shares are tied to the identical catalysts which are wanted to create higher development alternatives: decrease charges, higher housing turnover, and renewed confidence in bigger reworking initiatives.

Till then, the Q1 message is evident. Dwelling Depot is saying the cycle is prolonged however manageable, whereas Lowe’s is saying the housing market is traditionally robust, however execution can nonetheless drive development.

Neither firm is looking a flip in housing, and each are asking buyers to consider that when the flip lastly comes, they are going to emerge with extra market share than that they had earlier than. For now, Dwelling Depot and Lowe’s inventory each land a Zacks Rank #3 (Maintain).

Radical New Know-how May Hand Buyers Enormous Good points

Quantum Computing is the subsequent technological revolution, and it might be much more superior than AI.

Whereas some believed the know-how was years away, it’s already current and transferring quick. Massive hyperscalers, similar to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Cook dinner reveals 7 rigorously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s monumental potential again in 2016. Now, he has keyed in on what might be “the subsequent huge factor” in quantum computing supremacy. In the present day, you’ve got a uncommon likelihood to place your portfolio on the forefront of this chance.

See High Quantum Shares Now >>

Lowe’s Firms, Inc. (LOW) : Free Inventory Evaluation Report

The Dwelling Depot, Inc. (HD) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.

!")