CoreWeave (CRWV) and Amazon (AMZN) are main gamers in AI-focused cloud infrastructure, with the previous specializing in GPU-optimized compute for AI workloads and the latter’s AWS providing large-scale AI and high-performance cloud companies.

CoreWeave grew from a distinct segment GPU supplier into a number one AI cloud by shopping for massive GPU inventories and carving out relationships with AI labs and firms that want a lot of H100/Blackwell-class GPUs. Amazon additionally enjoys a dominant place within the cloud-computing market, notably within the IaaS area, due to AWS, which is one in all its high-margin producing companies.

Per a report from Fortune Enterprise Insights, the worldwide cloud AI market is valued at $102.09 billion in 2025 and is estimated to succeed in $589.22 billion by 2032, at a CAGR of 28.5%. Cloud AI combines AI with cloud computing to enhance how organizations work. Through the use of AI instruments like machine studying, pure language processing and laptop imaginative and prescient via the cloud, firms can increase effectivity, streamline each day duties and keep aggressive.

So if you’re keen to take a position, which inventory must you decide by way of development potential, fundamentals, valuation and threat tolerance? Let’s get to the core.

The Case for CRWV

From hyperscalers to frontier AI labs, organizations racing to construct the way forward for AI are turning to CoreWeave not just for uncooked GPU infrastructure, however for end-to-end high-performance cloud computing, networking and software program companies optimized particularly for AI. Within the final reported quarter, the corporate crushed all estimations, posting document income (up 134%) and a virtually doubled income backlog that now exceeds $55 billion. This backlog contains remaining efficiency obligations and extra quantities that CRWV expects to transform into income in future durations, topic to service supply necessities. This scale of contractual pipeline alerts long-term stability and strong demand for CoreWeave’s GPU-first cloud infrastructure within the period of AI.

CoreWeave is quickly changing into the cloud infrastructure spine for the world’s most superior AI organizations, and the third quarter showcased main new partnerships and capability expansions. It elevated its lively energy footprint by 120 MW sequentially to about 590 MW and expanded contracted energy capability previous 600 MW to 2.9 GW. This offers the corporate a powerful pipeline for future development, with greater than 1 GW of contracted capability nonetheless obtainable to promote and anticipated to come back on-line inside the subsequent yr. It additionally signed main compute contracts with key prospects, increasing present partnerships whereas lowering reliance on any single consumer.

It signed a multi-year deal price as much as $14.2 billion with Meta, expanded its partnership with OpenAI via a further deal of as much as $6.5 billion (bringing whole commitments to about $22.4 billion) and deepened its relationship with a number one hyperscaler, marking their sixth contract collectively. Along with hyperscalers and AI labs, CoreWeave added notable enterprise and authorities purchasers, together with Inference.web, Mizuho Financial institution, NASA JPL and Poolside. These partnerships affirm CoreWeave’s shift from area of interest GPU cloud supplier to a worldwide AI infrastructure powerhouse reliant on purpose-built HPC networking and large parallel compute environments.

Picture Supply: Zacks Funding Analysis

A significant pressure behind CoreWeave’s momentum is its multi-billion-dollar agreements with NVIDIA Company (NVDA). Third-quarter highlights embody being the primary to deploy NVIDIA GB300 NVL72 programs for large-scale frontier AI workloads and the primary to supply NVIDIA RTX PRO 6000 Blackwell Server Version cases, giving CRWV an early lead in real-time AI and simulation workloads. Additional, the corporate is on an acquisition spree to complement inorganic development. In October, it agreed to amass Marimo Inc., maker of an AI-native Python pocket book, strengthening its AI growth infrastructure. This follows earlier acquisitions like OpenPipe and Weights & Biases.

Nonetheless, its proposed $9 billion buy of Core Scientific was canceled after stakeholders rejected the deal. Regardless of working in a positive demand atmosphere, CRWV continues to face rising provide chain pressures, the place demand for its AI cloud platform vastly exceeds obtainable capability, limiting its skill to serve prospects absolutely. Delays in powered-shell supply from an information middle supplier are more likely to negatively influence its efficiency within the fourth quarter. Though non permanent and with the shopper agreeing to regulate the schedule to retain full contract worth, these setbacks have prompted administration to decrease its 2025 outlook. The corporate now expects income of $5.05–$5.15 billion, down from $5.15–$5.35 billion, and adjusted working revenue of $690–$720 million, beneath the earlier $800–$830 million vary.

The Case for AMZN

From AWS to e-commerce and Prime Video to Alexa, AI is driving effectivity, velocity and buyer engagement, serving to energy a powerful quarter for Amazon even amid restructuring prices and a significant authorized settlement. AWS is gaining sturdy momentum as prospects more and more select it for core and AI workloads on account of its superior performance, safety and efficiency. Its broad and deep infrastructure capabilities spanning startups, enterprises and authorities wants make AWS the popular platform for operating manufacturing workloads. With extra companies, richer options and fast innovation, AWS continues to steer the trade.

AWS revenues (18.3% of third quarter gross sales) rose 20.2% yr over yr to $33 billion, which beat the consensus mark by 2.01%. Owing to its sturdy capabilities, safety, efficiency and buyer focus, AWS continues to win most main enterprise and authorities cloud migrations. This makes AWS the first house for firm information and workloads, and a key purpose many shoppers need to run their AI there. To assist this demand, AWS has been quickly increasing capability, including over 3.8 GW of energy previously yr, greater than every other cloud supplier.

Picture Supply: Zacks Funding Analysis

Amazon is quickly increasing AWS’ energy capability, doubling what it had in 2022 and on observe to double once more by 2027. Within the fourth quarter alone, it expects so as to add one other 1 GW. The growth contains energy, information facilities and chips like AWS’ Trainium and NVIDIA GPUs. AWS additionally launched Venture Rainier, a big AI compute cluster with almost 500,000 Trainium2 chips, now utilized by Anthropic to construct and deploy Claude. Trainium2 demand is robust, absolutely subscribed and now a multibillion-dollar enterprise rising 150% quarter over quarter.

Moreover, its aggressive worldwide growth is driving long-term development by tapping into high-potential e-commerce markets throughout Asia, Europe and Latin America. By strengthening its logistics community and enhancing supply speeds, Amazon boosts buyer satisfaction whereas lowering reliance on the mature North American market. As digital adoption and middle-class spending rise globally, Amazon’s confirmed mannequin positions it to seize vital worth throughout growing areas.

Nonetheless, Amazon’s heavy spending on AI and information middle growth is pressuring its funds. AWS’ rising infrastructure wants require large ongoing funding in chips, computing energy and services, which is squeezing margins and lowering free money stream. With unsure returns and powerful competitors from Microsoft and Google, Amazon faces a chronic interval of excessive capital spending which will frustrate buyers searching for higher profitability and money era. Going forward, it expects its money CapEx to succeed in round $125 billion in 2025, with additional will increase deliberate for 2026. Heavy debt load limits its formidable development initiatives, creating monetary inflexibility throughout escalated macroeconomic fluctuations.

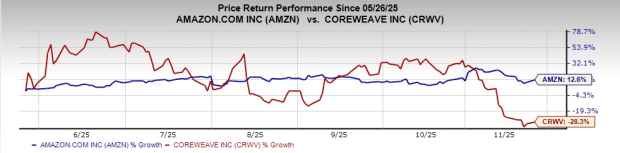

Share Efficiency and Valuation for CRWV & AMZN

Up to now six months, CRWV has declined 28.3% whereas AMZN is up 12.6%.

Picture Supply: Zacks Funding Analysis

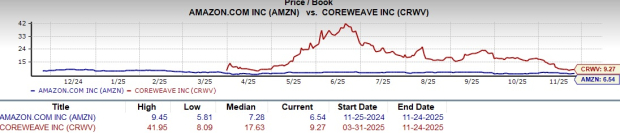

Valuation-wise, CoreWeave is overvalued, as recommended by the Worth Rating of D, whereas Amazon has a rating of B.

Picture Supply: Zacks Funding Analysis

When it comes to Value/Guide, CRWV shares are buying and selling at 9.27X, in contrast with AMZN’s 6.54X.

How Do Zacks Estimates Evaluate for CRWV & AMZN?

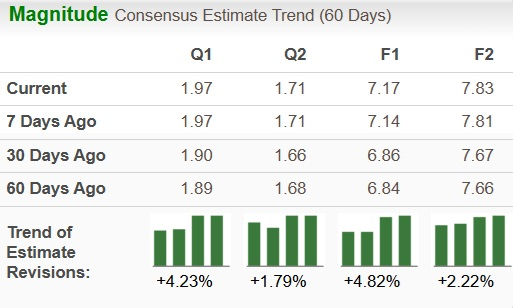

Analysts have saved their earnings estimates upward for AMZN’s backside line for the present yr.

Picture Supply: Zacks Funding Analysis

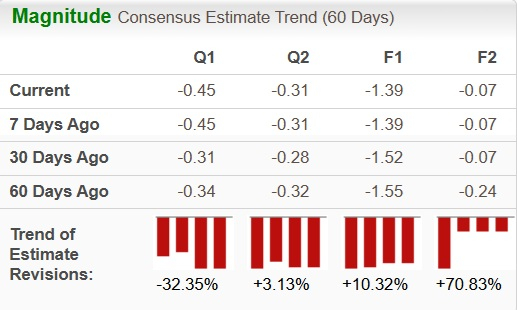

For CRWV, there’s a 10.32% upward revision.

Picture Supply: Zacks Funding Analysis

CRWV or AMZN: Which One to Purchase?

Amazon’s prospects are pushed by fast-growing AWS demand for AI and customized silicon, supported by main infrastructure growth set to double energy capability by 2027. Regardless of particular prices weighing on revenue, the corporate plans to maintain investing in AI, cloud and retail innovation, with promoting power and new merchandise fueling future development. CoreWaeve is a fast-growing, GPU-heavy specialist driving explosive AI demand, with excessive development potential. Nonetheless, excessive capital wants, buyer focus and execution threat pose worries.

AMZN presently carries a Zacks Rank #2 (Purchase) whereas CRWV has a Zacks Rank #3 (Maintain). Consequently, by way of Zacks Rank and valuation, AMZN appears to be a greater decide for the time being. You may see the whole record of in the present day’s Zacks #1 Rank (Robust Purchase) shares right here

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t more likely to maintain delivering the most important earnings. Little-known AI companies tackling the world’s greatest issues could also be extra profitable within the coming months and years.

See “2nd Wave” AI shares now >>

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

CoreWeave Inc. (CRWV) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.