")

Centene Company, a Zacks Rank #1 (Sturdy Purchase), has staged one of many extra spectacular turnarounds within the healthcare area over the previous 12 months.

After a troublesome 2025 that noticed the inventory fall out of favor amid elevated medical prices, the managed care big has come roaring again, supported by recovering margins, surging money move, and a strong wave of upward earnings estimate revisions. The corporate is a number one supplier of government-sponsored healthcare, with a dominant place in Medicaid and a quickly increasing Medicare footprint.

The inventory has rebounded sharply off its 2025 lows and now trades close to its 52-week excessive on rising quantity. Shares proceed to show relative power as shopping for stress accumulates on this resurgent market chief.

Centene is a part of the Zacks Medical – HMOs trade group, which presently ranks within the prime 10% out of roughly 250 Zacks Ranked Industries. As a result of it’s ranked within the prime half of all Zacks Ranked Industries, we count on this group to outperform over the subsequent 3 to six months, simply because it has begun to in latest months:

Picture Supply: Zacks Funding Analysis

Be aware of the favorable traits for this group beneath. The trade’s bettering positioning has been pushed by a optimistic earnings outlook for its constituent firms in combination, together with relative undervaluation — a robust mixture that ought to result in increased costs sooner or later.

Picture Supply: Zacks Funding Analysis

Historic analysis research recommend that roughly half of a inventory’s worth appreciation is because of its trade grouping. In actual fact, the highest 50% of Zacks Ranked Industries outperforms the underside 50% by an element of greater than 2 to 1.

It’s no secret that investing in shares which are a part of main trade teams may give us a leg up relative to the market. By specializing in main shares throughout the prime 50% of Zacks Ranked Industries, we are able to dramatically enhance our stock-picking success.

Firm Description

Centene operates as a diversified, multi-national healthcare enterprise that primarily serves under-insured and uninsured people by way of government-sponsored applications. The corporate operates by way of 4 segments — Medicaid, Medicare, Industrial, and Different — and ranks among the many largest healthcare firms within the nation, with roughly $191 billion in whole projected revenues and a spot at No. 19 on the Fortune 500. It’s also engaged in offering training and outreach applications that assist members entry high quality, acceptable care.

After navigating a difficult 2025 marked by rising medical prices and a withdrawal of steerage that battered the inventory, Centene has executed a methodical restoration. Administration’s relentless give attention to Medicaid margin restoration, disciplined price administration, and fee adequacy is clearly bearing fruit, whereas the Medicare Benefit and prescription drug plan companies have outperformed inside expectations.

The Texas Medicaid growth has added a significant new development vector, and the corporate has used its sturdy money technology — $4.4 billion of working money move in the newest quarter — to fortify the steadiness sheet, decreasing whole debt by $1 billion within the first quarter alone. The consolidated well being advantages ratio has been steadily bettering, a key sign that the worst of the medical-cost stress could also be within the rearview mirror.

Earnings Developments and Future Estimates

What stands out is Centene’s renewed capability to ship eye-catching earnings surprises. The corporate most just lately reported first-quarter 2026 outcomes that blew previous expectations, posting adjusted EPS of $3.37 — a determine that surpassed the Zacks Consensus Estimate by a outstanding 80.2% and climbed 16.2% from the year-ago interval.

Revenues of $49.9 billion rose 7.1% 12 months over 12 months and topped the consensus mark by 5.2%. The corporate has now topped consensus income estimates in every of the previous 4 quarters and exceeded EPS expectations in three of the final 4. This monitor report aligns completely with the facility of the Zacks Rank system, which prioritizes shares exhibiting upward earnings revisions.

On the heels of that beat, administration raised its full-year 2026 adjusted EPS steerage to larger than $3.40, up from a previous flooring of larger than $3.00, and lifted its whole income outlook to a band of $187.5–$191.5 billion.

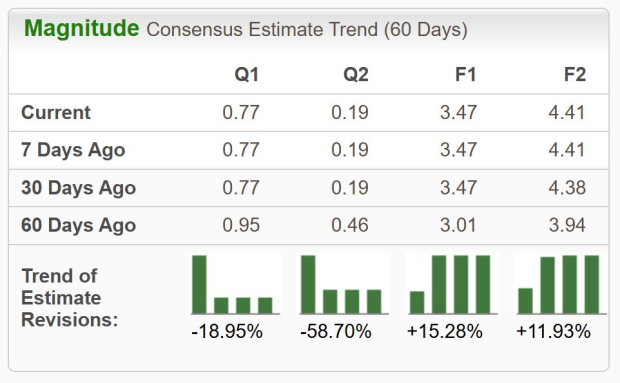

Analysts have responded enthusiastically: the Zacks Consensus Estimate for the present 12 months has surged 15.28% over the previous 60 days. That consensus now stands at $3.47 per share, reflecting an infinite 66.8% improve relative to the prior-year determine. Notably, the inventory screens as deeply undervalued even after its rally, carrying a PEG ratio of simply 0.51 versus the trade’s 1.12 and a prime Zacks Development Type Rating of A.

Picture Supply: Zacks Funding Analysis

Let’s Get Technical

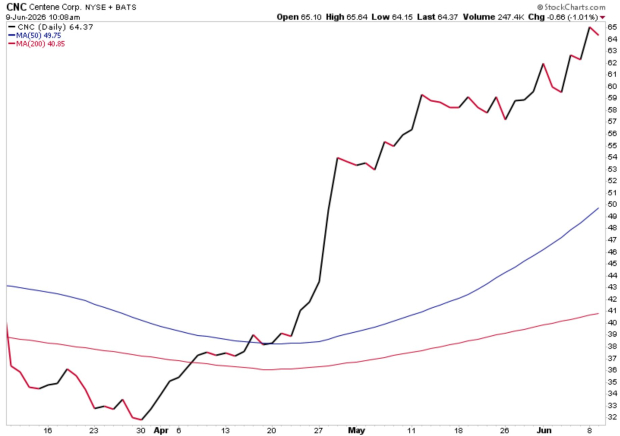

Centene CNC has transitioned from a falling knife in 2025 into one of many higher restoration tales available in the market right now. After bottoming final 12 months close to $25, shares have greater than doubled and now commerce close to their 52-week excessive. That is precisely the form of inventory we need to embody in our portfolio — one that’s trending properly and receiving optimistic earnings estimate revisions.

Picture Supply: StockCharts

Discover how shares now reside above upward-sloping 50-day (blue line) and 200-day (purple line) transferring averages, an indicator of a wholesome uptrend. The momentum has clearly constructed all through 2026. With each bettering fundamentals and a constructive technical image, Centene seems poised to proceed its outperformance.

Empirical analysis exhibits a robust correlation between near-term inventory actions and traits in earnings estimate revisions. As we all know, Centene has just lately witnessed sharp upward revisions. So long as this development stays intact (and CNC continues to ship earnings beats), the inventory will possible proceed its bullish run.

Backside Line

Backed by a number one trade group and a renewed historical past of earnings beats, it’s not troublesome to see why this turnaround story is a compelling funding. Presently, CNC carries a Zacks Rank #1 (Sturdy Purchase), pushed by highly effective estimate momentum.

The mix of Medicaid margin restoration, Medicare outperformance, bettering money move, and a reduced valuation ought to proceed to supply a tailwind for the inventory worth. With the subsequent earnings report anticipated in late July, sturdy fundamentals mixed with a strengthening technical development actually justify including shares to the combo. In case you haven’t already completed so, make sure to put CNC in your watchlist.

Zacks’ Analysis Chief Names “Inventory Most More likely to Double”

Our crew of consultants has simply launched the 5 shares with the best chance of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This prime choose is a little-known satellite-based communications agency. Area is projected to turn into a trillion greenback trade, and this firm’s buyer base is rising quick. Analysts have forecasted a serious income breakout in 2025. In fact, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our Prime Inventory And 4 Runners Up

Centene Company (CNC) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.