")

M-tron Industries MPTI) has been one of many market’s standout small-cap tales, with the economic merchandise firm benefiting from robust demand throughout aerospace, protection, avionics, and area markets.

That stated, traders could need to train warning as expectations seem to have run effectively forward of fundamentals.

MPTI has delivered distinctive features over the previous yr, however valuation considerations, execution dangers, and elevated expectations may make the inventory susceptible to a pointy pullback.

Picture Supply: Zacks Funding Analysis

M-tron’s Dependence on Protection Spending

M-tron’s progress story is closely tied to U.S. protection spending and precision-guided munitions packages. Administration has emphasised its relationships with main protection contractors and its publicity to missile techniques and radar functions.

Though protection budgets stay favorable, authorities spending priorities can shift. Program delays, procurement adjustments, finances negotiations, or geopolitical developments may affect order timing and future income progress.

For a corporation with a comparatively concentrated end-market profile, any slowdown in protection orders may have an outsized affect on outcomes, and investor sentiment may start to fade, particularly with the U.S. and Iran reaching a ceasefire deal.

Backlog Progress Would not Assure Close to-Time period Income

Traders typically view backlog progress as a direct indicator of future earnings, however the timing of changing orders into income may be unpredictable. Whereas M-tron most not too long ago reported its backlog expanded 38% yr over yr to $76.8 million, administration famous that a number of the bigger protection alternatives could not contribute to manufacturing volumes till late 2027 and even 2028.

Which means the market could also be assigning worth to earnings that stay years away from materializing.

Plus, backlog figures can fluctuate considerably based mostly on the timing of enormous contract awards and buyer buying patterns. After all, any slowdown in new bookings may additionally alter investor sentiment.

Margin Dangers Stay

Though M-tron’s profitability has improved considerably, margin stress stays a priority. The corporate has already cited tariff prices and product-mix adjustments as elements affecting gross margins.

Moreover, as M-tron invests in capability enlargement, analysis and growth, and potential acquisitions, working prices may rise. Speedy progress typically brings execution challenges, and sustaining present margin ranges could grow to be more and more troublesome.

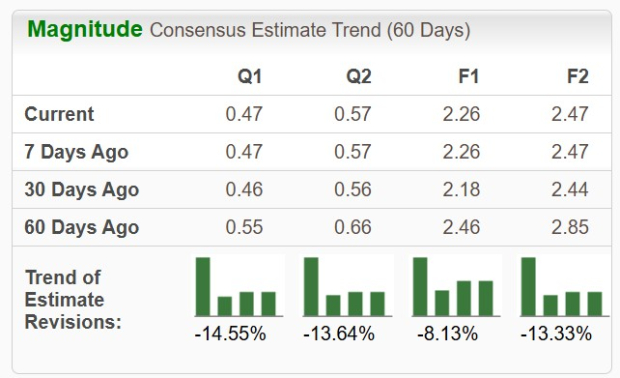

It’s additionally noteworthy that during the last 60 days, M-tron’s FY26 and FY27 EPS estimates are nonetheless down 8% and 13%, respectively, regardless of a modest uptick within the final month.

Picture Supply: Zacks Funding Analysis

Volatility & Valuation Issues

One other danger traders ought to think about is MPTI’s small dimension. Small-cap protection names typically commerce on momentum, making them prone to sharp corrections when investor sentiment adjustments.

With its market capitalization of $426 million being effectively beneath the economic merchandise market common and lots of of its protection friends amid a restricted public float, MPTI can expertise vital volatility.

This dynamic can work in each instructions, however after a considerable run larger, volatility turns into a larger danger for MPTI shareholders.

Picture Supply: Zacks Funding Analysis

Including to the volatility considerations and margin dangers is that MPTI is buying and selling at 43X ahead earnings, a notable premium to the economic merchandise market and the benchmark S&P 500’s common of round 23X, respectively.

Picture Supply: Zacks Funding Analysis

Backside Line

For traders who have already got positions in M-tron Industries inventory, now could also be a great time to take earnings, whereas those that are contemplating MPTI could need to keep away from it for now.

To that time, MPTI’s spectacular efficiency has raised expectations to lofty ranges, as traders at the moment are paying for years of anticipated progress, and the corporate faces dangers tied to protection spending cycles, backlog conversion timing, margin stress, and small-cap volatility.

With a lot of the excellent news seemingly priced in and little room for disappointment, MPTI seems susceptible to a interval of consolidation or a number of compression.

Zacks’ Analysis Chief Names “Inventory Most Prone to Double”

Our staff of specialists has simply launched the 5 shares with the best likelihood of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This prime decide is a little-known satellite-based communications agency. Area is projected to grow to be a trillion greenback business, and this firm’s buyer base is rising quick. Analysts have forecasted a significant income breakout in 2025. After all, all our elite picks aren’t winners however this one may far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our High Inventory And 4 Runners Up

Medical Properties Belief, Inc. (MPT) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.