")

2025 was one other turbulent yr for Azenta AZTA inventory, which fell greater than 30% because the medical options supplier struggled with ongoing gross sales weak point. Azenta’s struggles have been highlighted by each short-term efficiency points and longer-term structural challenges.

The prolonged underperformance has led to diminished investor confidence and promoting stress, with Azenta showing to lose its mojo concerning its providers for drug improvement, medical analysis, and superior cell therapies.

Even with occasional rebounds, the general momentum stays weak for Azenta inventory, and analysts have expressed warning concerning the firm’s capacity to outperform going ahead.

Picture Supply: Zacks Funding Analysis

Income Weak spot & Market Uncertainty

Azenta’s challenges look like tied to elementary enterprise softness, particularly in key income segments. Though Azenta was in a position to attain EPS expectations of $0.21 for its most up-to-date fiscal fourth quarter and edged gross sales estimates of $156.67 million, the market’s optimistic response was short-lived as its high line contracted from $170 million within the prior yr quarter.

To that time, Azenta has had difficulties in regard to sustaining its annual income above $500 million, as proven beneath. Moreover, Azenta has warned of continued uncertainty within the macro atmosphere, notably round capital spending from its prospects, which generally contains biotech corporations in addition to gene and cell remedy corporations.

Picture Supply: Zacks Funding Analysis

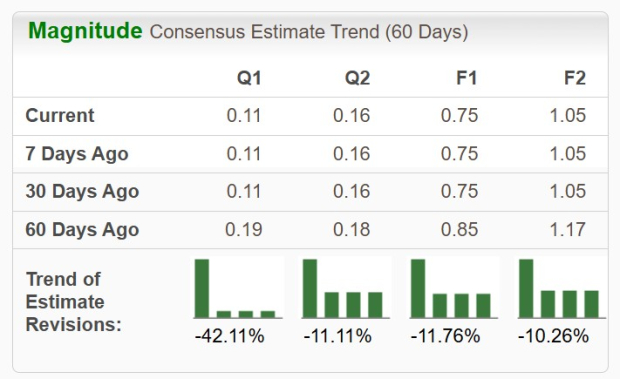

Declining EPS Revisions

Justifying the market’s considerations is that Azenta’s present fiscal 2026 and FY27 EPS estimates have declined over 10% within the final 60 days, respectively.

And at $34 a share, Azenta inventory nonetheless isn’t low-cost when it comes to its ahead P/E a number of of 46X, a pointy premium to the benchmark S&P 500’s 26X regardless of vastly underperforming the broader market lately.

Picture Supply: Zacks Funding Analysis

Backside Line

Till Azenta demonstrates sustained income progress or operational enhancements, its inventory could proceed to face stress. Correlating with such, AZTA at present lands a Zacks Rank #5 (Sturdy Promote) and has been a notable inventory to keep away from going into 2026.

Zacks Naming Prime 10 Shares for 2026

Wish to be tipped off early to our 10 high picks for the whole lot of 2026? Historical past suggests their efficiency might be sensational.

From 2012 (when our Director of Analysis Sheraz Mian assumed duty for the portfolio) by means of November, 2025, the Zacks Prime 10 Shares gained +2,530.8%, greater than QUADRUPLING the S&P 500’s +570.3%.

Now Sheraz is combing by means of 4,400 corporations to handpick the perfect 10 tickers to purchase and maintain in 2026. Don’t miss your probability to get in on these shares after they’re launched on January 5.

Be First to New Prime 10 Shares >>

Azenta, Inc. (AZTA) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.