I’ve been detailing the rotation unfolding beneath the floor of the market in latest weeks. Whereas mega-cap know-how and far of the AI ecosystem pulled again, worth shares, cyclicals and several other worldwide markets attracted recent inflows. The sort of management transition is frequent throughout ongoing bull markets. Prolonged winners consolidate, capital briefly rotates elsewhere, and as soon as expectations reset, the strongest franchises usually resume management.

That sample seems to be taking part in out once more. The Magnificent 7 has largely traded sideways to modestly decrease since final November as issues surrounding AI overinvestment, valuation multiples and aggressive capital spending prompted some buyers to step apart. But the elemental actuality has not deteriorated. If something, the strategic positioning of those corporations seems to be stronger than ever. These companies stay the premier property in world equities, combining dominant aggressive moats, monumental money movement technology and publicity to almost each main secular progress theme within the trendy financial system.

Importantly, synthetic intelligence is just not their solely progress driver. Even with out AI, these companies would nonetheless sit on the heart of a number of long-term growth developments spanning cloud computing, digital promoting, e-commerce, enterprise software program, shopper gadgets, social media, and digital funds. AI due to this fact capabilities much less as a speculative add-on and extra as an accelerator layered on high of already highly effective enterprise fashions.

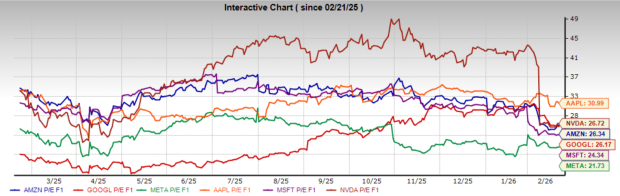

Picture Supply: TradingView

Cloud Is Reaccelerating for MSFT, GOOGL and AMZN

For Amazon (AMZN), Alphabet (GOOGL) and Microsoft (MSFT), essentially the most quick sign of strengthening fundamentals is coming from cloud computing. Demand for compute capability tied to AI workloads stays terribly sturdy, with hyperscalers persevering with to report that out there capability is successfully offered out. In sensible phrases, they can not construct knowledge facilities quick sufficient to fulfill buyer demand.

After moderating by components of 2024, progress in these cloud divisions is now re-accelerating. On the identical time, valuations for a number of of those names have change into notably extra affordable following the latest consolidation.

Amazon and Microsoft specifically are buying and selling close to a few of their extra compelling ahead multiples in a number of years, whereas Alphabet, although barely elevated is just not unreasonably priced. For buyers searching for publicity to AI infrastructure with out paying peak enthusiasm pricing, this reset could show significant.

Compelling Valuations Throughout Magnificent 7 Shares

Meta Platforms (META) stays one of many clearest valuation standouts throughout the cohort. The inventory continuously turns into the topic of maximum sentiment swings, but the underlying enterprise continues to generate large free money movement whereas sustaining dominant world promoting attain. Buying and selling at lower than roughly 22x earnings whereas analysts challenge roughly 20% long-term annual earnings progress, the risk-reward profile seems unusually enticing for an organization of its scale. Early proof additionally means that AI-driven enhancements in content material focusing on, advert effectivity and inside operations are contributing to margin growth.

Nvidia (NVDA) continues to operate because the foundational infrastructure supplier for the worldwide AI buildout. Regardless of remaining one of many market’s strongest performers over the previous two years, the inventory now trades across the mid-20s on ahead earnings whereas consensus expectations nonetheless name for earnings progress approaching the high-40% vary. That mixture produces a PEG ratio close to 0.5, a degree that traditionally has signaled sturdy progress relative to valuation for dominant know-how leaders. So long as hyperscale spending stays elevated, Nvidia’s central function in supplying high-performance AI chips retains its earnings outlook firmly supported.

Apple (AAPL) occupies a considerably totally different however equally essential place contained in the Magnificent 7. In contrast to many friends, Apple has not pursued the identical aggressive AI infrastructure spending technique, which has helped protect the inventory from a number of the capex-related volatility affecting different mega-caps. Operationally, the corporate continues to execute at a formidable degree given its monumental measurement. Current outcomes confirmed renewed energy in each iPhone demand and China income, two areas that beforehand involved buyers, whereas the high-margin companies section continues to broaden quickly. Whole income progress within the mid-teens underscores that Apple’s ecosystem stays terribly resilient. More and more, buyers are recognizing that Apple’s best AI benefit is probably not constructing fashions however proudly owning the dominant world system platform by which billions of customers will entry AI companies.

Picture Supply: Zacks Funding Analysis

Magnificent 7 Shares Consolidating

Considered collectively, the latest buying and selling sample within the Magnificent 7 seems to be way more like a wholesome consolidation than a structural breakdown. Bull markets not often advance in straight traces, notably after highly effective multi-year runs. Intervals of sideways motion enable earnings to meet up with costs, valuations to normalize and investor expectations to reset.

With cloud demand strengthening, AI adoption persevering with to broaden, earnings progress forecasts remaining strong and valuations in a number of circumstances changing into extra enticing, the setup means that mega-cap know-how could also be positioned to reassert management because the yr progresses.

For buyers, the important thing takeaway is easy: the non permanent pause out there’s most dominant corporations has not altered their long-term aggressive positioning. If the broader bull market stays intact, historical past means that the premier franchises with the strongest steadiness sheets, widest moats and deepest publicity to structural progress developments are sometimes those that finally lead the following advance.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unimaginable demand for knowledge is fueling the market’s subsequent digital gold rush. As knowledge facilities proceed to be constructed and consistently upgraded, the businesses that present the {hardware} for these behemoths will change into the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to reap the benefits of the following progress stage of this market. It focuses on semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is precisely the place you wish to be.

See This Inventory Now for Free >>

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

Apple Inc. (AAPL) : Free Inventory Evaluation Report

Microsoft Company (MSFT) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.