- The Case for Financial institution of America

- The Case for Citigroup

- How Do Earnings Estimates Examine for BAC & C?

- BAC & C: Value Efficiency, Valuation & Different Comparisons

- BAC or C: Which Financial institution Inventory is a Smarter Maintain By 2026?

- Zacks’ Analysis Chief Names “Inventory Most More likely to Double”

Financial institution of America BAC and Citigroup C are among the many largest U.S. banks, closely uncovered to rate of interest cycles, mortgage development and international monetary markets. They supply diversified monetary companies, together with industrial banking, funding banking, wealth administration and retail banking, and are outstanding, systemically vital establishments with a world footprint.

BAC is extra leveraged to U.S. rates of interest and client well being, whereas C is majorly influenced by international commerce, worldwide development and foreign money/geopolitical traits. Their efficiency heading into 2026 will replicate macroeconomic traits, Fed coverage shifts and evolving capital return methods. On this context, let’s take a better look to find out which inventory has extra room to run.

The Case for Financial institution of America

Regardless of being one of the vital asset-sensitive banks in America, Financial institution of America is much less more likely to witness strain on its internet curiosity earnings (NII) in 2026 amid declining rates of interest. That is anticipated to be pushed by fixed-rate asset repricing, enhancing lending situation, resilient customers and a gradual fall in funding prices. Additional, it’s anticipated to witness first rate deposit development. As such, the corporate tasks a 5-7% year-over-year enhance in NII for 2026, after related development this 12 months.

Moreover, Financial institution of America’s aggressive monetary heart enlargement technique throughout the US will solidify buyer relationships and faucet into new markets, driving NII development over time. The corporate has entered 18 new markets since 2014 and plans to open monetary facilities in six further markets via 2028. This enlargement has already added 170 new monetary facilities and $18 billion in incremental deposits in these markets. The corporate additionally plans to proceed strengthening its know-how initiatives and spend closely on these. These efforts assist it entice and retain prospects and enhance cross-selling alternatives.

Additional, the shift towards simpler financial coverage is anticipated to help shopper exercise, deal circulation and asset values. The corporate plans to make use of knowledge and AI throughout lending, threat and advisory to enhance effectivity, with development led by higher-return companies like center market, international banking and wealth administration, alongside worldwide enlargement and broader capital options. So, Financial institution of America’s non-interest earnings streams will doubtless see significant upside in 2026.

Decrease charges are anticipated to help BAC’s asset high quality, as declining charges will ease debt-service burdens and enhance borrower solvency. Because the financial institution embarks on an bold enlargement plan to open monetary facilities in new and current markets and improve know-how utilization, working bills are more likely to stay elevated within the close to time period.

The Case for Citigroup

As rates of interest fall, Citigroup’s NII development is anticipated to be below strain in 2026. Nonetheless, for this 12 months, the corporate expects NII (excluding Markets) to develop round 5.5%, indicating improved mortgage demand and better deposit balances.

Additional, CEO Jane Fraser continues to advance Citigroup’s multi-year technique to streamline operations and deal with its core companies. Since asserting plans in April 2021 to exit client banking in 14 markets throughout Asia and EMEA, the corporate has accomplished its exit in 9 international locations. These initiatives will unencumber capital and assist the corporate pursue investments in wealth administration operations in Singapore, Hong Kong, the UAE and London to stoke price earnings development. Supported by these initiatives, Citigroup tasks whole revenues to exceed $84 billion in 2025, with revenues projected to see a 4-5% CAGR via 2026.

Additionally, Citigroup is simplifying its organizational construction, slicing 20,000 jobs by 2026, with divestitures and workforce reductions anticipated to save lots of $2-$2.5 billion in annualized run price financial savings by 2026. The corporate additionally continues to deal with streamlining processes and platforms and driving automation to scale back guide touchpoints. Citigroup is more and more deploying synthetic intelligence (AI) instruments to help these efforts.

As the corporate is specializing in a leaner group construction and decreasing international footprint, working bills are more likely to come down. Citigroup anticipates bills to be under $53 billion in 2026, excluding FDIC charges, implying a decline from the $56.4 billion in 2023.

On the similar time, regulatory pressures are easing. In response to a Reuters article, which was revealed on MSN, the Fed closed long-standing supervisory notices associated to Citigroup’s threat administration and knowledge governance shortcomings. With this burden lifted, the financial institution is better-positioned to execute its development and effectivity initiatives.

How Do Earnings Estimates Examine for BAC & C?

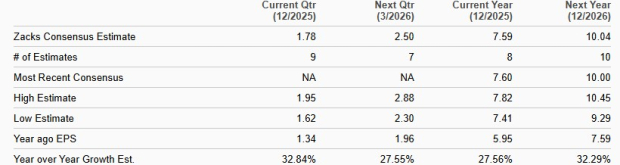

The Zacks Consensus Estimate for BAC’s 2025 and 2026 earnings signifies 15.9% and 14% development, respectively. Financial institution of America’s earnings estimates for 2025 and 2026 have been revised decrease over the previous seven days.

BAC Earnings Estimates

Picture Supply: Zacks Funding Analysis

The Zacks Consensus Estimate for C’s 2025 and 2026 earnings signifies a bounce of 27.6% and 32.3%, respectively. Its earnings estimates for 2025 and 2026 have been revised barely upward over the previous week.

C Earnings Estimates

Picture Supply: Zacks Funding Analysis

BAC & C: Value Efficiency, Valuation & Different Comparisons

Over the previous six months, C and BAC shares have risen 45.6% and 19.8%, respectively. This displays that traders are optimistic in regards to the success of Citigroup’s enterprise transformation plan. Therefore, when it comes to worth efficiency, C has a transparent edge over Financial institution of America.

Six-Month Value Efficiency

Picture Supply: Zacks Funding Analysis

By way of valuation, Citigroup is presently buying and selling at a 12-month ahead price-to-earnings (P/E) of 11.81X. BAC inventory, in distinction, is presently buying and selling at a 12-month ahead P/E of 12.93X.

P/E F12M

Picture Supply: Zacks Funding Analysis

Each are buying and selling at a reduction in contrast with the trade’s 12-month ahead P/E of 15.09X. So, C is buying and selling at a reduction in contrast with Financial institution of America.

Financial institution of America and Citigroup bear annual stress assessments carried out by the Fed earlier than they’ll announce their capital distribution plans. Following the 2025 stress check, they hiked their dividends. Citigroup raised its quarterly dividend by 7% to 60 cents per share. It has a dividend yield of two.03%. Likewise, BAC elevated its quarterly dividend by 8% to twenty-eight cents per share. It has a dividend yield of two.00%. Primarily based on dividend yield, C has a slight edge over BAC.

Dividend Yield

Picture Supply: Zacks Funding Analysis

Financial institution of America’s return on fairness (ROE) of 10.76% is means increased than Citigroup’s 7.91%. This displays BAC’s environment friendly use of shareholder funds in producing income.

ROE

Picture Supply: Zacks Funding Analysis

BAC or C: Which Financial institution Inventory is a Smarter Maintain By 2026?

Whereas Financial institution of America affords secure development potential and a robust U.S. footprint, Citigroup stands out as the higher 2026 funding. Its ongoing transformation, international strategic focus, aggressive cost-cutting and stronger earnings development expectations place it properly for improved profitability.

Buying and selling at a decrease valuation and exhibiting superior latest worth efficiency, Citigroup supplies extra upside potential because it executes on operational effectivity and worldwide wealth development. With regulatory overhangs easing and income momentum constructing, C inventory seems higher poised to reward long-term traders heading into 2026.

At current, each BAC and C carry a Zacks Rank #3 (Maintain). You’ll be able to see the whole record of right this moment’s Zacks #1 Rank (Sturdy Purchase) shares right here.

Zacks’ Analysis Chief Names “Inventory Most More likely to Double”

Our staff of consultants has simply launched the 5 shares with the best chance of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This high choose is a little-known satellite-based communications agency. House is projected to change into a trillion greenback trade, and this firm’s buyer base is rising quick. Analysts have forecasted a serious income breakout in 2025. After all, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our High Inventory And 4 Runners Up

Financial institution of America Company (BAC) : Free Inventory Evaluation Report

Citigroup Inc. (C) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.