The Zacks REIT and Fairness Belief business is bearing the brunt of mortgage price volatility, fueled by persistent inflation and broader financial uncertainty. With mortgage charges averaging within the mid-6% in latest weeks, business gamers are more likely to face continued earnings stress within the close to time period.

Ongoing affordability challenges within the housing market are weighing on buy originations and refinancing exercise. Nonetheless, firms like Ellington Monetary LLC EFC, Redwood Belief Inc. RWT and TPG Mortgage Funding Belief Inc. MITT are well-poised to navigate business challenges.

In regards to the Trade

The Zacks REIT and Fairness Belief business includes mortgage REITs, often known as mREITs. Trade members spend money on and originate mortgages and mortgage-backed securities (“MBS”), and supply mortgage credit score for householders and companies. Sometimes, these firms give attention to both the residential or business mortgage markets. Some spend money on each markets by way of asset-backed securities. Company securities are backed by the federal authorities, making them safer bets and limiting credit score dangers. Such REITs increase funds within the debt and fairness markets by way of widespread and most well-liked fairness, repurchase agreements, structured financing, convertible and long-term debt, and different credit score amenities. The web curiosity margin, the unfold between curiosity revenue on mortgage property and securities held, in addition to funding prices, is a key income metric for mREITs.

What’s Shaping the Way forward for the mREIT Trade?

Volatility in Mortgage Charges Retains Consumers on Sidelines: The 30-year mounted mortgage price has climbed in latest weeks to the mid-6% from low-6% vary within the begin of the 2026.

In the meantime, the Federal Reserve has stored rates of interest unchanged thus far in 2026 as policymakers proceed to steadiness rising inflation with a resilient labor market. In opposition to this backdrop, mortgage charges are more likely to stay elevated within the close to time period.

Greater borrowing prices, mixed with affordability pressures and financial uncertainty, have discouraged many potential homebuyers from getting into the market.

Because of this, mortgage origination and refinancing exercise are beneath stress. This development is anticipated to intensify operational and monetary challenges for mREIT business gamers, whereas weighing on gain-on-sale margins and limiting funding exercise.

Trade Resorts to Dividend Cuts as E-book Values Erode: Elevated rates of interest, persistent mortgage market volatility, and the widening unfold between 30-year Company mortgage-backed securities (MBS) and 10-year U.S. Treasury yields have decreased the worth of Company MBS portfolios.

As such, company mREITs are witnessing a decline in tangible e book worth as spreads on benchmark indices have widened. It will improve earnings stress for extremely leveraged mREITs.

To protect capital and align payouts with sustainable earnings, many ndustry gamers are lowering dividends. Dividend cuts might set off investor outflows from income-focused funds, additional weighing on share costs and e book values, creating near-term headwinds for the mREITs.

Conservative Method to Help Lengthy-Time period Returns: Within the present risky mortgage market setting, mREITs are adopting a extra conservative method, which might strengthen their long-term positioning.

By changing into extra selective of their investments, these firms are specializing in higher-quality property, thereby enhancing the general resilience and stability of their portfolios.

This disciplined technique helps cut back publicity to dangerous credit score situations and limits potential losses during times of uncertainty.

Moreover, using larger hedge ratios to handle rate of interest dangers displays prudent monetary administration. Whereas this method might limit near-term upside, it improves earnings visibility and protects capital from sudden market fluctuations.

By prioritizing liquidity, asset high quality and threat administration, mREITs are better-equipped to navigate market volatility and capitalize on enticing alternatives as soon as situations stabilize.

General, this cautious stance helps sustainable efficiency and creates a stronger basis for constant long-term returns.

Zacks Trade Rank Signifies Bleak Prospects

The Zacks REIT and Fairness Belief business is housed throughout the broader Zacks Finance sector. The business carries a Zacks Trade Rank #211, which locations it within the backside 15% of greater than 244 Zacks industries.

The group’s Zacks Trade Rank, which is the typical of the Zacks Rank of all of the member shares, signifies underperformance within the close to time period. Our analysis exhibits that the highest 50% of the Zacks-ranked industries outperform the underside 50% by an element of greater than 2 to 1.

The business’s positioning within the backside 50% of the Zacks-ranked industries is an consequence of the discouraging earnings outlook for the constituent firms.

Wanting on the mixture earnings estimate revisions, it seems that analysts are regularly dropping confidence on this group’s earnings development potential. The business’s current-year earnings estimate moved 9.3% down during the last yr.

Earlier than we current a couple of shares that you could be need to purchase regardless of near-term challenges, allow us to check out the business’s latest stock-market efficiency and valuation image.

Trade Lags the Sector & the S&P 500

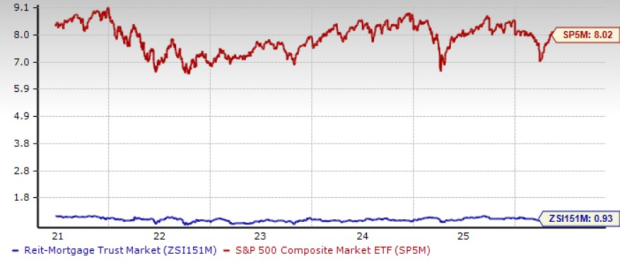

The Zacks REIT and Fairness Belief business has underperformed the broader Zacks Finance sector and the S&P 500 composite up to now yr.

The business has gained 1.4% within the above-mentioned interval in contrast with the broader sector’s rise of 15.6%. Additional, the S&P Index has grown 27.7% over the previous yr.

Worth Efficiency

Trade’s Present Valuation

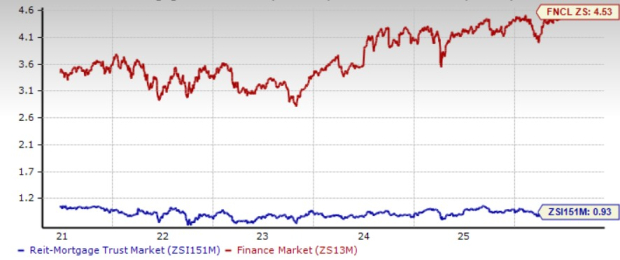

Primarily based on the trailing 12-month price-to-book (P/B), which is a generally used a number of for valuing mREITs, the business is buying and selling at 0.93X in contrast with the S&P 500’s 8.02X. Previously 5 years, the business has traded as excessive as 1.05X, as little as 0.70X and on the median of 0.91X.

Worth-to-E-book TTM

As finance shares usually have a low P/B ratio, evaluating REIT and Fairness Belief with the S&P 500 might not make sense to many buyers. A comparability of the group’s P/B ratio with that of the broader sector ensures that the group is buying and selling at a strong low cost. The Zacks Finance sector’s trailing 12-month P/B got here in at 4.53X. That is above the Zacks REIT and Fairness Belief business’s ratio, because the chart under exhibits.

Worth-to-E-book TTM

3 mREIT Shares to Wager On — EFC, RWT & MITT

Ellington Monetary invests in a various array of economic property. These embrace residential and business mortgage loans and mortgage-backed securities, shopper loans, and asset-backed securities.

The property are supported by shopper loans, collateralized mortgage obligations, non-mortgage and mortgage-related derivatives, fairness investments in mortgage origination firms, and different strategic investments.

EFC is well-positioned to climate volatility within the mortgage market, supported by its diversified publicity throughout residential and business mortgage mortgage portfolios, and powerful momentum in its securitization platform.

The corporate’s mortgage originations, particularly in business mortgage bridge loans, proprietary reverse mortgages and closed-end second lien loans, proceed to contribute to secure development and revenue.

Its first-quarter 2026 development was pushed by sturdy efficiency throughout its diversified mortgage and credit score platforms. Its subsidiary, Longbridge Monetary, remained a serious earnings contributor within the first quarter of 2026, benefiting from larger mortgage originations, securitizations, and servicing revenue.

To navigate market uncertainty, Ellington Monetary is actively leveraging dynamic hedging methods, sustaining a broad and balanced portfolio, securing a number of sources of financing and working with low leverage.

These measures mirror a disciplined method to threat administration and a dedication to preserving e book worth whereas adapting to shifting market situations.

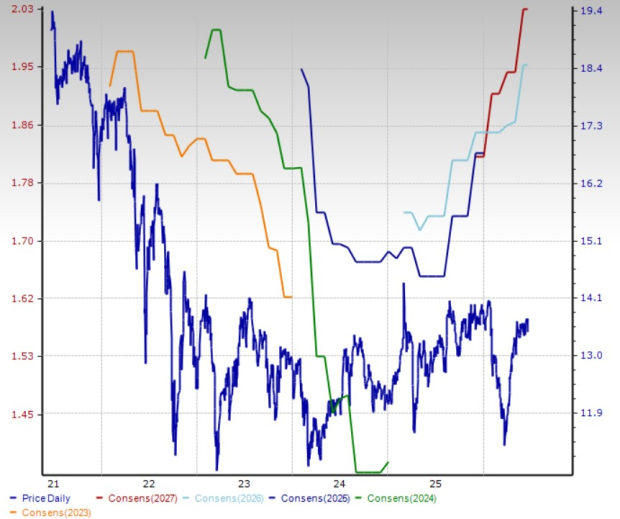

The corporate’s 2026 earnings estimates have been unchanged at $1.95 per share over the previous month, indicating year-over-year development of seven.1%.

EFC flaunts a Zacks Rank #1 (Sturdy Purchase) at current and has a market capitalization of $1.71 billion.

Worth and Consensus: EFC

Redwood Belief is a self-advised and self-managed actual property funding belief.

RWT makes a speciality of buying and managing actual property mortgage property, which can be acquired as complete loans or as mortgage securities representing pursuits in or obligations, backed by swimming pools of mortgage loans.

The corporate has been witnessing distinctive development in its mortgage banking platforms over the latest quarters regardless of a risky interest-rate setting.

Mortgage banking manufacturing reached a document $8.5 billion within the first quarter of 2026, marking the third consecutive quarterly document, supported by sturdy demand for Sequoia and Aspire merchandise, elevated securitization exercise and better whole-loan gross sales.

In latest months, RWT undertook focused actions to simplify its working construction and sharpen its give attention to companies producing sturdy and sustainable returns. This positions the platform to comprehend value financial savings sooner or later.

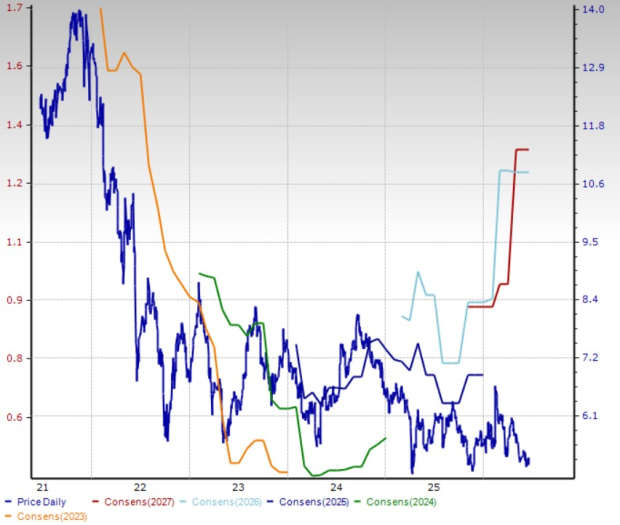

Redwood Belief’s 2026 earnings have been unchanged at $1.28 over the previous month. It signifies a year-over-year soar of 45.5%.

The corporate at the moment carries a Zacks Rank # 2 (Purchase) and a market capitalization of $659.9 million.

Worth and Consensus: RWT

TPG Mortgage is a residential mREIT with a give attention to investing in a diversified risk-adjusted portfolio of residential mortgage-related property principally within the U.S. mortgage market.

Over the previous few quarters, MITT’s development has been pushed by a resilient residential mortgage portfolio and disciplined capital administration regardless of market volatility.

The corporate maintained an $8.1-billion funding portfolio within the first quarter of 2026, supported by $7.7 billion of financing, primarily by way of non-recourse borrowings, whereas preserving financial leverage at a conservative 1.7X. The corporate can also be benefiting from secure web curiosity revenue and continued power in its funding in Arc Dwelling.

In February 2026, TPG Mortgage introduced a long-term strategic funding administration partnership with Jackson Monetary Inc., which is anticipated to unlock further avenues for development over time.

TPG Mortgage’s 2026 earnings have been unchanged at $1.09 per share over the previous month. It signifies a year-over-year rally of 26.7%.

At current, MITT has a Zacks Rank #2 and a market capitalization of $252.5 million.

Worth and Consensus: MITT

Radical New Expertise May Hand Traders Enormous Good points

Quantum Computing is the following technological revolution, and it may very well be much more superior than AI.

Whereas some believed the know-how was years away, it’s already current and shifting quick. Massive hyperscalers, corresponding to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Prepare dinner reveals 7 fastidiously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s huge potential again in 2016. Now, he has keyed in on what may very well be “the following large factor” in quantum computing supremacy. In the present day, you’ve a uncommon probability to place your portfolio on the forefront of this chance.

See Prime Quantum Shares Now >>

Ellington Monetary Inc. (EFC) : Free Inventory Evaluation Report

Redwood Belief, Inc. (RWT) : Free Inventory Evaluation Report

TPG Mortgage Funding Belief Inc. (MITT) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.