UnitedHealth Group Included UNH has staged a pointy comeback, with shares climbing 12% over the previous month, trimming its year-to-date loss to 29.1%. The transfer marks an outperformance versus each the broader business’s 9.3% achieve and the S&P 500 Index’s 4% rise throughout the identical interval. Amongst key friends, Humana Inc. HUM fell 4.9%, whereas Elevance Well being, Inc. ELV superior 13.6%, underscoring a large divergence in managed care efficiency.

One-Month Worth Efficiency – UNH, HUM, ELV, Trade & S&P 500

Picture Supply: Zacks Funding Analysis

Traditionally seen as a defensive mainstay in healthcare, UnitedHealth earned its popularity by means of constant earnings, a reliable dividend stream, and a low beta of 0.47, qualities that appealed to risk-averse buyers in search of stability. However from 2024 onward, what as soon as seemed like wholesome pullbacks started to really feel extra like warning indicators as a number of headwinds piled up. The current rally, nonetheless, suggests sentiment could lastly be shifting.

One main catalyst got here from Warren Buffett’s Berkshire Hathaway Inc. (BRK.B), which disclosed a $1.57 billion buy of greater than 5 million UNH shares. The information fueled a surge of institutional and retail shopping for, sparking a rebound from its prolonged downtrend. Including to the optimism, UnitedHealth reaffirmed its up to date 2025 adjusted EPS steering regardless of the anticipated short-term dilution from its August acquisition of Amedisys on account of financing and integration prices.

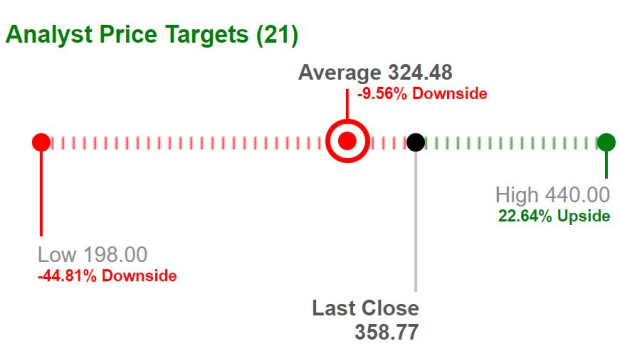

Nonetheless, the inventory at present trades above the Wall Road common value goal of $324.48, suggesting a 9.6% draw back from present ranges.

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

Is UNH Low-cost Sufficient to Chase?

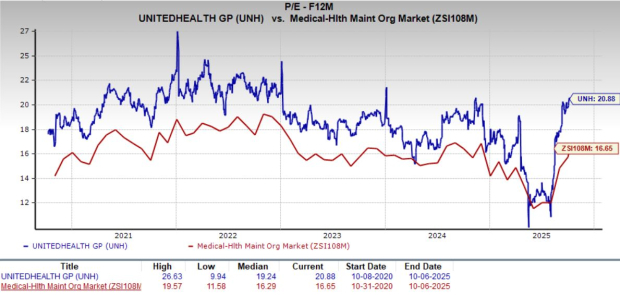

Valuation stays a sticking level. UNH’s ahead P/E stands at 20.88X, increased than its five-year median of 19.24X and above the business common of 16.65X. By comparability, Humana trades at 20.90X, whereas Elevance sits far decrease at 11.27X. The premium displays confidence in UnitedHealth’s long-term stability, but it surely additionally suggests restricted near-term upside potential.

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

UNH’s Headwinds

UnitedHealth continues to wrestle with elevated medical prices and utilization tendencies which have pressured profitability throughout the managed care area. The corporate’s medical loss ratio — a key measure of claims prices relative to premiums — has steadily worsened, rising from 83.2% in 2023 to 85.5% in 2024, and additional to 89.4% within the second quarter of 2025. The upper ratio alerts shrinking margins and restricted room for error.

Regulatory and authorized scrutiny provides one other layer of uncertainty. The Division of Justice is probing UnitedHealth’s Medicare billing practices, reimbursement insurance policies and Optum Rx’s pharmacy profit administration operations. Moreover, the corporate faces questions surrounding its dealing with of loans to healthcare suppliers following the 2024 Change Healthcare cyberattack.

In the meantime, President Donald Trump’s “most-favored nation” government order might disrupt the pharmacy profit administration mannequin, probably reshaping how Optum Rx negotiates and manages drug pricing.

Unfavorable Earnings Outlook for UNH

Analyst sentiment has turned cautious. The Zacks Consensus Estimate tasks a pointy 41.4% drop in 2025 EPS to $16.21, whilst revenues are anticipated to rise 12.1% 12 months over 12 months. This mismatch underscores issues that top-line development isn’t translating into bottom-line power. The consensus forecast for the third quarter factors to a steep 59.9% year-over-year earnings decline, suggesting profitability stays below intense stress.

Compounding the uncertainty, the corporate missed earnings estimates in two of the final 4 quarters, beating within the different two, with a median earnings shock of damaging 3.3%.

UnitedHealth Group Included Worth, Consensus and EPS Shock

UnitedHealth Group Included price-consensus-eps-surprise-chart | UnitedHealth Group Included Quote

UNH Charting a Restoration Course?

Regardless of its challenges, UnitedHealth stays a powerhouse within the U.S. healthcare sector, benefiting from unmatched scale, diversification and an enormous buyer base. As of June 30, 2025, its UnitedHealthcare division served 50.1 million members, up 2.1% from a 12 months in the past, pushed primarily by self-funded business plans.

Administration has taken proactive steps to stabilize operations. Dealing with tighter regulatory situations, slashed funding and better healthcare bills, UnitedHealth plans to curtail its Medicare Benefit presence for this 12 months, exiting greater than 100 plans throughout 109 counties in 16 states. Nonetheless, the transfer will have an effect on roughly 180,000 members, per a number of reviews.

Whereas eligibility redeterminations and decreased authorities subsidies will probably weigh on membership development, demand for UnitedHealth’s high-margin, fee-based business plans is predicted to offset a part of the impression. The corporate additionally continues to generate strong money stream, producing $24.2 billion in working money in 2024 and $6.3 billion throughout the first half of 2025.

Though decrease income could briefly gradual money era, sturdy operational effectivity and disciplined expense administration ought to assist maintain margins. Backed by its money stream resilience, UnitedHealth continues to reward shareholders, distributing over $5.5 billion by means of dividends and buybacks within the first half of 2025.

Backside Line

UnitedHealth’s current rebound has actually rekindled investor curiosity, helped by Berkshire Hathaway’s backing and administration’s regular steering. But, beneath the floor, the challenges stay important as rising medical prices, tightening regulation and earnings stress proceed to cloud its near-term outlook. Whereas the corporate’s scale, diversification and money stream era lend it resilience, the premium valuation and muted revenue trajectory restrict upside potential within the quick run.

General, UnitedHealth presents a balanced risk-reward profile at present ranges, regular however not with out challenges. At the moment, the inventory carries a Zacks Rank #3 (Maintain), suggesting buyers could also be higher served by endurance till clearer indicators of sustainable margin restoration emerge.

You may see the whole checklist of at this time’s Zacks #1 Rank (Sturdy Purchase) shares right here.

5 Shares Set to Double

Every was handpicked by a Zacks professional because the #1 favourite inventory to realize +100% or extra within the coming 12 months. Whereas not all picks could be winners, earlier suggestions have soared +112%, +171%, +209% and +232%.

Many of the shares on this report are flying below Wall Road radar, which supplies an important alternative to get in on the bottom flooring.

Immediately, See These 5 Potential House Runs >>

UnitedHealth Group Included (UNH) : Free Inventory Evaluation Report

Berkshire Hathaway Inc. (BRK.B) : Free Inventory Evaluation Report

Humana Inc. (HUM) : Free Inventory Evaluation Report

Elevance Well being, Inc. (ELV) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.