Macro elements at present driving the financial system, corresponding to inflation, rates of interest, labor markets, provide chain points and so forth have a diversified affect on gamers within the extraordinarily numerous Web – Providers business, though a stronger financial system is usually optimistic. Subsequently, the continued battle; declining client confidence primarily associated to tariffs, inflation and jobs; and inflation-driven rising producer worth index (PPI) could also be thought of unfavourable for the Web Providers business.

Our picks are Zillow Z and Sprout Social SPT due to their development prospects, AI adoption and price reducing measures.

Most business gamers are closely investing in synthetic intelligence and machine studying as this enables them to offer extra options and differentiate their choices. Being a capital-intensive business with excessive fastened price of operation and the pretty fixed have to construct infrastructure, a excessive rate of interest isn’t very optimistic for it. Subsequently, any charge cuts in 2026 would make us incrementally optimistic concerning the Web Providers business.

Valuation stays wealthy, however rising estimates point out the existence of alternatives.

In regards to the Business

Web – Providers corporations are primarily people who depend on big software program and {hardware} infrastructure, known as their properties, to ship numerous companies to customers. Folks can avail the companies by accessing these properties with their private related units from virtually wherever on the earth.

Firms typically function two fashions: an ad-based mannequin and an ad-free mannequin the place the service is charged. Alphabet, Baidu and Akamai are a number of the bigger gamers whereas Crexendo, Upwork, Dropbox, Etsy, Shopify, Uber, Lyft and Trivago are a number of the rising gamers. Very giant gamers (primarily Alphabet) are inclined to skew averages.

Due to the variety of companies provided, it’s tough to establish industrywide elements that would have an effect on all gamers. The impact of macro elements corresponding to inflation, charge hikes, provide chain points and so forth differ.

Components Figuring out Business Efficiency

- Information is central to success on this business, because it permits the gamers to construct synthetic intelligence (AI) fashions to enhance the standard of companies, create new applied sciences and companies, and in addition to decrease the price of operation. AI is altering the way in which these corporations function: search is turning into conversational, content material creation is turning into automated, AI brokers are performing numerous duties and customized suggestions at the moment are out there at scale. Web service suppliers are additionally in a position to differentiate their merchandise based mostly on the dimensions, flexibility and selection in AI-powered instruments that they provide. The market is extraordinarily aggressive and smaller instruments are getting commoditized. Consumer interfaces throughout the online are being redesigned to undertake these adjustments. Bigger corporations usually have the sting in AI as a result of they’ve entry to bigger knowledge units that may be processed to additional develop their AI.

- Monetization is more and more shifting past conventional promoting as corporations search extra steady and diversified income streams. Whereas digital adverts as soon as dominated enterprise fashions, development in promoting has matured and develop into extra cyclical, prompting platforms to develop into subscriptions, transaction charges, marketplaces and monetary companies. Firms now purpose to seize worth instantly from person exercise moderately than solely promoting viewers consideration to advertisers. For instance, platforms combine funds, premium memberships, commerce instruments, and enterprise software program choices to generate recurring or usage-based revenue. This transition improves income predictability, strengthens buyer relationships, and reduces dependence on fluctuating advert markets.

- The web companies business has undergone a significant shift from prioritizing speedy person and income development to emphasizing profitability and sustainable money circulate. Through the low-interest-rate period, traders rewarded corporations for increasing aggressively, even at the price of giant losses. Nonetheless, larger rates of interest and tighter capital markets have modified expectations, pushing corporations to give attention to working effectivity, margin growth and disciplined spending. Companies at the moment are optimizing headcount, decreasing buyer acquisition prices and enhancing monetization of present customers moderately than pursuing development at any price. This transition displays a broader market choice for resilient enterprise fashions able to producing constant earnings throughout financial cycles.

- Being a capital-intensive business, there may be the necessity to increase funds to construct out pricey infrastructure. Funds are additionally wanted to keep up this infrastructure. Given the secular development prospects, corporations have continued infrastructure investments by 2023, 2024 and 2025 regardless of excessive rates of interest. Most analysts anticipate rates of interest to come back down additional in 2026, which might encourage additional improve in capex. Ex-Alphabet PP&E shows some seasonality though the pattern continues to swing upward, which means that corporations are investing closely of their infrastructure.

- Regulation and antitrust stress have develop into a defining pressure shaping the web companies business as governments worldwide improve scrutiny of enormous digital platforms. Policymakers are specializing in points corresponding to market dominance, knowledge privateness, algorithm transparency, app-store practices and digital promoting energy. New laws purpose to restrict anti-competitive habits, shield client knowledge and guarantee honest entry for smaller rivals, forcing corporations to regulate enterprise fashions, product design and growth methods. Compliance prices and authorized dangers are rising, whereas acquisitions and platform integrations face nearer overview. Because of this, regulation is not a background threat however a core strategic issue influencing innovation, monetization and long-term development selections.

Zacks Business Rank Signifies Close to-Time period Stress

The Zacks Web – Providers business is housed throughout the broader Zacks Pc and Expertise sector. It carries a Zacks Business Rank #176, which locations it among the many backside 28% of 243 Zacks-classified industries.

The group’s Zacks Business Rank, which is mainly the typical rank of all of the member shares, signifies that there are a number of alternatives within the area.

Wanting on the mixture earnings estimate revisions over the previous 12 months, enhancements in each the 2026 and 2027 estimates have been roughly constant, remaining comparatively stronger within the final two months. Because of this, the combination estimates for 2026 and 2027 are up a respective 12.1% and 13% over the previous 12 months.

Traditionally, the highest 50% of Zacks-ranked industries outperforms the underside 50% by an element of greater than 2 to 1. So the business having moved into the underside 50% signifies that investor sentiments stay muted.

Earlier than we current a couple of shares that you could be need to think about in your portfolio, let’s check out the business’s latest stock-market efficiency and valuation image.

Business Valuation: Wealthy

Over the previous 12 months, the business has returned greater than each the broader Expertise sector and the S&P 500. It had been buying and selling beneath each indexes up till July however began pulling forward thereafter. It has widened the hole with each since September final 12 months.

The business’s web acquire of 65.6% over the previous 12 months is greater than the broader sector’s 28.6% and the S&P 500’s 17.6%.

One-12 months Value Efficiency

Picture Supply: Zacks Funding Analysis

Business Seems Considerably Overvalued

On the idea of ahead 12-month price-to-earnings (P/E) ratio, we see that the business is at present buying and selling at a 23.90X a number of, which is kind of its median worth of 23.89X over the previous 12 months. It is a 15.3% premium to the S&P 500’s 20.72X and a 5.3% premium to the sector’s 29.07X.

Over the previous 12 months, the business has traded within the vary of 17.22X to 29.74X, a much wider vary than the S&P’s 20.63X to 23.8X. The sector has traded within the 22.7X to 29.9X vary.

Ahead 12 Month Value-to-Earnings (P/E) Ratio

Picture Supply: Zacks Funding Analysis

2 Strong Bets

The Web Providers business is just not in an excellent place in the intervening time primarily due to an unsure macro and persistently excessive rates of interest. For the reason that business is extremely numerous, it is just to be anticipated that some gamers could be doing exceedingly effectively whereas others not a lot. We at present have a Zacks #2 (Purchase) score on each Zillow and Sprout Social mentioned beneath.

Zillow Group Inc. (Z): Zillow operates a digital real-estate market that connects homebuyers, sellers, renters, real-estate brokers, landlords, and mortgage suppliers throughout the US. Its platforms permit customers to go looking property listings, view worth estimates (Zestimates), schedule excursions and make contact with brokers. Z

illow generates income primarily by promoting and lead-generation companies bought to real-estate professionals, rental market charges and mortgage origination companies. The corporate is evolving into an end-to-end “housing super-app,” integrating search, financing, touring, transaction help and leases right into a unified on-line ecosystem designed to streamline residential real-estate transactions from discovery by closing.

The shift away from a listings web site to a platform market reduces Zillow’s dependence on advert income and opens up the potential of a number of charges per transaction, driving up income per dwelling bought. The corporate is effectively positioned to capitalize on its huge visitors, sturdy model recognition and nationwide community to generate strong development. Moreover, it’s investing in AI-based dwelling suggestions, automated valuations, good agent matching and

conversational search, all of which ought to facilitate the transition. Its income mannequin guarantees extra steady margins and its asset-light mannequin will permit it to capitalize on housing market upcycles with restricted stability sheet affect.

The one main draw back to the entire story is its dependence on the rate of interest, which is predicted to stay excessive relative to historic requirements. This drives up mortgage charges and due to this fact, dwelling costs, and dries up shopping for intent. The prospect of decrease dwelling gross sales naturally drives down earnings expectations and hits the share worth.

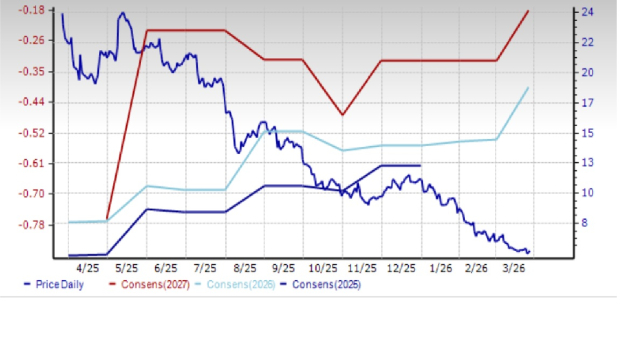

The corporate beat earnings estimates by 3 cents. Each 2026 and 2027 estimaes are unchanged within the final 30 days though each are down in contrast with 60 days in the past. Analysts are at present in search of 2026 income and earnings development of 15.1% and 28.1%, respectively. For 2027, they’re anticipating 13.4% income development and 28.9% earnings development.

The shares of this Zacks Rank #2 (Purchase) inventory are down 38.1% over the previous 12 months.

Value and Consensus: Z

Picture Supply: Zacks Funding Analysis

Sprout Social, Inc. (SPT): Sprout Social, Inc. is a cloud-based software program firm that gives companies with instruments to handle, analyze and optimize their social-media presence throughout platforms corresponding to Instagram, LinkedIn, TikTok, Fb and X. Its subscription platform integrates content material publishing, message administration, customer support, social listening, influencer advertising and marketing and efficiency analytics right into a unified dashboard.

Firms use Sprout to schedule posts, reply to prospects by a centralized inbox, monitor model sentiment and generate data-driven advertising and marketing insights. The corporate more and more embeds AI to automate workflows, interpret social knowledge, and assist organizations flip on-line conversations into measurable enterprise intelligence and buyer engagement methods.

As social media evolves from a mere advertising and marketing channel to a platform supporting a spread of capabilities, together with buyer care, model monitoring, disaster administration, gross sales discovery and fame analytics, the demand for a SaaS platform that may deal with all these points for manufacturers can also be on the rise. Sprout has been progressively growing its giant enterprise focus as a result of the broader volumes and scale are make this an apparent option to drive income and profitability.

Enterprises don’t typically hop from one vendor to a different, which lowers churn, provides predictability to income streams and helps pricing energy. There’s additionally the potential of progressively increasing companies inside accounts. Basically, software program supply prices develop at a slower tempo than subscriptions. So as soon as investments stabilize, there may be important working leverage, which results in strong margin growth.

There may be an ongoing debate about whether or not AI is absolutely useful for the corporate because it lowers obstacles to entry and will increase competitors, together with from giant social media gamers’ inhouse developments, whereas additionally growing price of innovation as options are rapidly commoditized. Nonetheless, Sprout does have a aggressive moat within the huge quantities of unstructured datasets throughout platforms that it already possesses, together with its normalization and analytics operations, which require the sort of infrastructure that can’t be in-built a rush. Historic datasets additionally enhance AI accuracy.

Sprout processes large social datasets and embeds AI into sentiment evaluation, automated engagement and marketing campaign optimization. Buyer evaluations and rankings proceed putting Sprout as a frontrunner in social listening and analytics instruments.

Sprout topped estimates within the final quarter, with earnings beating by 25%. The 2026 estimate has not modified within the final 30 days whereas the 2027 estimate elevated 5 cents (4.4%). At these ranges, they signify a 7.8% improve in income and a 14.6% improve in earnings for 2026 and a 7% income improve and 27.1% earnings improve within the following 12 months.

The shares of this Zacks Rank #2 (Purchase) inventory have misplaced 77.2% of their worth over the previous 12 months.

Value and Consensus: SPT

Picture Supply: Zacks Funding Analysis

Zacks Names #1 Semiconductor Inventory

This under-the-radar firm makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is uniquely positioned to make the most of the following development stage of this market. And it is simply starting to enter the highlight, which is precisely the place you need to be.

With sturdy earnings development and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. International semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $971 billion by 2028.

See This Inventory Now for Free >>

Zillow Group, Inc. (Z) : Free Inventory Evaluation Report

Sprout Social, Inc. (SPT) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.