Pepsi PEP is among the notable enterprise giants that helped kick off the Q3 earnings season on a optimistic word this week.

Exceeding Q3 expectations, the long-lasting Pepsi model has been capable of maintain by means of the corporate’s strategic innovation, cost-cutting initiatives, and pricing energy regardless of many beverage makers going through quantity pressures from a extra inflation-conscious client.

Following its favorable Q3 outcomes yesterday morning, Pepsi inventory has now spiked +8%, rising as a lot as +6% in Friday’s buying and selling session.

Nevertheless, PEP remains to be greater than 14% from its 52-week excessive of $177 a share, making it a worthy subject of whether or not now is a perfect time to purchase Pepsi inventory for an prolonged rebound.

Picture Supply: Zacks Funding Analysis

Pepsi’s Favorable Q3 Outcomes

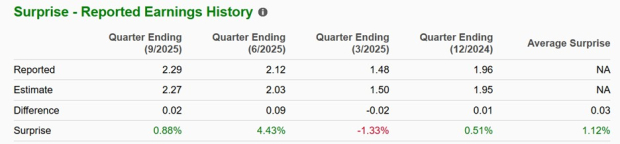

Posting Q3 gross sales of $23.93 billion, Pepsi’s prime line expanded 2% from $23.31 billion within the prior yr quarter and topped estimates of $23.87 billion. On the underside line, Pepsi posted Q3 earnings of $2.29 per share, topping expectations of $2.27 regardless of dipping from EPS of $2.31 a yr in the past.

Offsetting a 1% decline in international meals and beverage volumes, Pepsi’s efficient pricing rose 4%, exhibiting the corporate remains to be capable of increase costs with out dropping clients.

Pepsi has now exceeded prime and backside line expectations in three of its final 4 quarterly experiences, with a median gross sales and earnings shock of 0.57% and 1.12% respectively.

Picture Supply: Zacks Funding Analysis

Pepsi’s Revolutionary Product Line

Separating Pepsi from chief rival, Coca-Cola KO, has been its growth into meals and snack merchandise, and is now innovating them to focus on a extra health-conscious buyer base. Eradicating synthetic elements from Lay’s and Tostitos chips, Pepsi has additionally rolled out new merchandise like protein-fortified Doritos and Quaker Oats objects.

Together with this, Pepsi is increasing its presence in zero-sugar drinks, together with a lineup of low-sugar Gatorade, in addition to pursuing fiber because the “subsequent protein” in a wager on fiber-enhanced snacks and drinks.

Pepsi’s Steerage & Outlook

Attributed to its cost-cutting initiatives and progressive product line, Pepsi expects improved profitability in its core North America phase. Reaffirming its full-year steering, Pepsi nonetheless expects natural income development of roughly 4% however forecasts a 0.5% decline in earnings per share in fiscal 2025 from EPS of $8.16 final yr.

Zacks’ projections at the moment name for Pepsi’s EPS to dip to $8.05 in FY25, though FY26 earnings are projected to rebound and rise 5% to $8.50 per share. Primarily based on Zacks’ estimates, Pepsi’s whole gross sales are slated to rise 1% this yr and are projected to extend one other 3% in FY26 to $96.22 billion.

Picture Supply: Zacks Funding Analysis

PEP Efficiency & Valuation Comparability

Amid the post-earnings rally, Pepsi inventory remains to be down practically 2% yr so far, noticeably trailing the benchmark S&P 500’s +15%, Coca-Cola’s +8% and their Zacks Beverage-Smooth drinks Market’s return of +2%.

From an extended view, PEP is up a really subpar +6% within the final 5 years, however has a complete return of over +20% when together with dividends, though this has largely trailed the broader market, Coca-Cola, and its Zacks sub-industry’s returns of over +40%.

Picture Supply: Zacks Funding Analysis

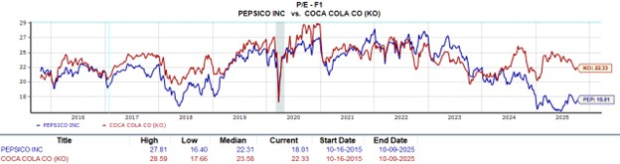

At present ranges, Pepsi inventory is beginning to stand out at 18X ahead earnings, buying and selling roughly on par with its {industry} common and providing a definite low cost to Coca-Cola’s 22X and the benchmark’s 25X.

It’s additionally price noting that PEP is buying and selling at a pleasant low cost to its decade-long ahead P/E a number of excessive and median of 27X and 22X.

Plus, PEP trades close to the popular degree of lower than 2X ahead gross sales, which can be on par with the {industry} common and properly beneath Coca-Cola’s 6X and the S&P 500’s 5X.

Picture Supply: Zacks Funding Analysis

Pepsi’s Attractive Dividend

Relating to worth and definitely revenue investing, Pepsi shares are enticing with a 3.93% annual dividend yield that impressively tops Coca-Cola’s 3.07% and the S&P 500’s common of 1.1%.

Moreover, a lot of its {industry} friends don’t supply a payout, however like Coca-Cola, Pepsi is a Dividend King, growing its dividend for greater than 50 consecutive years. That stated, over the past 5 years, Pepsi has had a extra attractive annualized dividend development fee of seven.65% in comparison with Coca-Cola’s 4.84%.

Dedicated to rewarding shareholders by means of dividends and buybacks, Pepsi expects to return a worth price $8.6 billion in 2025 when together with dividends and share repurchases.

Picture Supply: Zacks Funding Analysis

Backside Line

Pepsi’s favorable Q3 report does recommend an prolonged rebound could possibly be in play and will assist PEP retain its present Zacks Rank #2 (Purchase) ranking, which is based on rising earnings estimate revisions (EPS).

In distinction, Coca-Cola inventory lands a Zacks Rank #4 (Promote) for the time being as EPS revisions have trended decrease with the beverage big’s Q3 report scheduled for Tuesday, October 21st. Whereas Coca-Cola tends to get the nod forward of Pepsi from worth buyers, this state of affairs doesn’t seem like the case for the time being.

Zacks’ Analysis Chief Picks Inventory Most More likely to “At Least Double”

Our specialists have revealed their High 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. After all, all our picks aren’t winners however this one may far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our High Inventory to Double (Plus 4 Runners Up) >>

PepsiCo, Inc. (PEP) : Free Inventory Evaluation Report

CocaCola Firm (The) (KO) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.