It was no shock that shares moved increased on Friday, as September’s cooler inflation readings sparked the rally. Nevertheless, Intel INTC stood out specifically after delivering nice Q3 outcomes on Thursday night that confirmed the chipmaker’s turnaround is possible.

Hitting a recent one-year excessive of $41 a share in Friday’s buying and selling session, Intel inventory has continued an attention-getting rebound from a 52-week and multi-year low of $17.

The higher-than-expected CPI knowledge can also preserve the Federal Reserve on observe for an additional rate of interest lower, which will be very helpful to Intel and different chipmakers. That mentioned, let’s see if it’s time to purchase Intel inventory or fade the rebound in INTC.

Picture Supply: Zacks Funding Analysis

Q3 Marked Intel’s Return to Profitability.. For Now

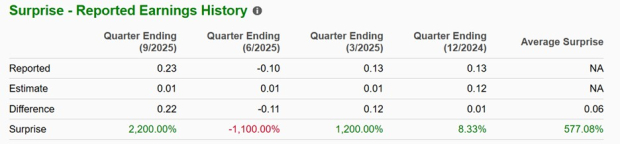

Marking a return to development and profitability, Intel reported Q3 internet revenue of $4.06 billion or $0.23 per share, in comparison with a regarding lack of $16.64 billion within the comparative quarter or -$0.43 a share. Fueling the early morning rally in INTC was that Intel crushed EPS expectations of $0.01.

Nevertheless, it’s noteworthy that Intel’s revenue was largely pushed by one-time non-recurring operational positive factors. This included the divestiture of a majority stake in its programmable chip-unit enterprise, Altera, together with favorable tax therapies and accounting reclassifications associated to its restructuring and asset gross sales.

Notably, whereas Intel was capable of publish optimistic adjusted earnings per share in This fall final yr ($0.13) and Q1 2025 ($0.13) as proven beneath, the corporate’s internet revenue for these quarters was -$129 million and -$887 million, respectively.

Picture Supply: Zacks Funding Analysis

Intel’s Key Progress Drivers

Intel did cite improved execution, with CEO Lip-Bu Tan emphasizing higher operational self-discipline and strategic focus, particularly in manufacturing and analysis and growth (R&D). It’s additionally noteworthy that decrease charges usually gasoline tech corporations by decreasing capital spending prices on R&D, hiring, and enlargement into new or rising markets.

Concerning AI, Intel noticed robust momentum in AI-related merchandise, equivalent to its purpose-built application-specific built-in circuit (ASIC) chips, accelerators, and AI PCs. AI chips and compute infrastructure lifted Intel’s Information Middle and AI (DCAI) division income by 5% yr over yr to $4.1 billion. General, Q3 gross sales rose 3% to $13.65 billion and topped estimates of $13.11 billion.

Strategic AI collaborations are additionally boosting Intel’s operations in regard to the $5 billion fairness funding it obtained from Nvidia NVDA and $2 billion from SoftBank SFTBY. Whereas Intel now seems to have sufficient money to fund capital bills, a charge lower would additionally assist if extra exterior funding is required within the type of borrowing and never fairness. In fact, what has reshaped investor sentiment probably the most is that the U.S. Authorities turned Intel’s largest shareholder after changing the $11.1 billion the corporate obtained from the CHIPS Act grants into fairness.

Intel’s Steerage & Outlook

Intel expects This fall income at $12.8 to $13.8 billion, which fell in vary of Zacks’ projections of $13.37 billion. Intel forecasts This fall EPS at $0.08, consistent with the Zacks Consensus. Moreover, Intel initiatives This fall gross margins of roughly 36.5% and full-year approximate gross capital investments of $18 billion.

Attributed to the deconsolidation of Altera, Intel revised projections for its full-year adjusted working bills right down to $16.8 billion from $17 billion.

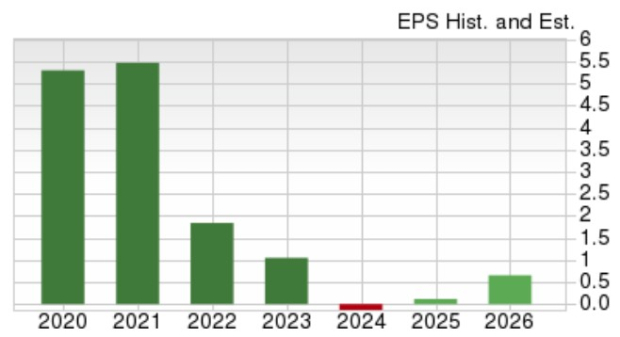

Primarily based on Zacks’ estimates, Intel’s complete gross sales at the moment are anticipated to dip 2% in fiscal 2025 however are projected to rebound and rise 3% in FY26 to $53.76 billion. Intel’s annual EPS is at the moment slated to swing to $0.12 in FY25 in comparison with an adjusted lack of 0.13 a share final yr. Optimistically, FY26 EPS is projected to rebound to $0.64, though that is properly away from Intel’s previous earnings potential.

Picture Supply: Zacks Funding Analysis

Abstract & Closing Ideas

On the floor, Intel’s “robust” Q3 outcomes might look interesting for hopes of a possible turnaround, however there’s nonetheless a lot to see. To that time, the chip big’s return to profitability was largely attributed to divesting Altera and never its core enterprise operations. Nonetheless, the modest AI enhance and echoes of disciplined price administration are reassuring amid the potential for one other rate of interest lower and fairness investments from the federal authorities, Nvidia, and SoftBank.

Given these prospects, it might be too quickly to fade the rebound in INTC, though a big uptick in EPS revisions could also be wanted for FY26 to make sure a purchase score. For now, Intel inventory lands a Zacks Rank #3 (Maintain).

Zacks Names #1 Semiconductor Inventory

This under-the-radar firm makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is uniquely positioned to benefit from the following development stage of this market. And it is simply starting to enter the highlight, which is precisely the place you need to be.

With robust earnings development and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. International semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $971 billion by 2028.

See This Inventory Now for Free >>

Intel Company (INTC) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

SoftBank Group Corp. Unsponsored ADR (SFTBY) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.