- Value Efficiency (Six months)

- Core Tailwinds Strengthening PPL Company’s Outlook

- Headwinds for PPL

- PPL’s Earnings Estimates Going Up

- PPL’s Capital Return Program

- PPL Inventory Returns Decrease Than the Business

- PPL Inventory Trades at a Premium

- Rounding Up

- Zacks’ Analysis Chief Names “Inventory Most More likely to Double”

PPL Company’s PPL shares have gained 2.7% within the final six months in contrast with the Zacks Utility-Electrical Energy business’s rise of 11.9%. The corporate additionally underperformed the Zacks Utilities sector in the identical timeframe.

PPL reported constructive earnings shock within the final reporting quarter, however larger working bills are a priority. Nonetheless, the corporate is benefiting from elevated information middle demand, significantly in Pennsylvania and Kentucky, as these amenities require substantial electrical energy.

One other operator in the identical house, Xcel Vitality XEL, is making a considerable funding to strengthen its infrastructure to offer dependable providers to clients. The corporate missed earnings estimates within the final reporting quarter and its shares have gained 10.2% prior to now six months.

Value Efficiency (Six months)

Picture Supply: Zacks Funding Analysis

Ought to traders contemplate including PPL to their portfolio primarily based on the present softness in worth actions? Allow us to delve deeper and discover out the components that may assist traders resolve whether or not it’s a good entry level so as to add the PPL inventory to their portfolios.

Core Tailwinds Strengthening PPL Company’s Outlook

PPL Company’s capital funding technique is closely centered on strengthening its technology, transmission and distribution infrastructure. These steady upgrades have already improved system reliability, leading to fewer buyer outages. Trying forward, the corporate intends to speculate $20 billion from 2025 to 2028 to additional improve operations and guarantee it continues delivering high-quality service to clients.

PPL Company makes use of a “self-healing grid” as a part of its good grid know-how, enabling the system to mechanically determine outages and reroute energy to scale back buyer disruptions. This superior setup delivers real-time information, supporting proactive upkeep and boosting total grid resilience and effectivity.

PPL can also be experiencing load development in its service areas, pushed by information middle demand. Almost 20.5 gigawatts (“GW”), up from 14.4 GW within the second quarter, of potential information middle demand are within the superior levels, in Pennsylvania area representing a possible transmission capital funding of $1 billion, up from $0.4 million. In Kentucky area, information middle requests have elevated to eight.7GW from 5.7GW within the second quarter. The corporate has infrastructure in place to serve the rising demand in its service area and acquire from the identical.

Greater than 60% of PPL’s capital funding plan is topic to “contemporaneous restoration,” which reduces the impression of regulatory lag on earnings for investments. The restoration of capital expenditures shortly permits the corporate to fund long-term initiatives simply.

Headwinds for PPL

PPL’s Pennsylvania Regulated section faces competitors for transmission initiatives. It has to abide by sure guidelines of the Federal Vitality Regulatory Fee to develop transmission initiatives and construction the price for a similar. The growing competitors within the transmission enterprise, thus forcing the corporate to scale back prices to stay aggressive.

PPL makes vital investments in infrastructure initiatives and people have to adjust to environmental legal guidelines. Any delay or failure of completion of initiatives on time or inside funds and elevated unexpected prices or danger of restoration of venture prices might negatively impression its financials.

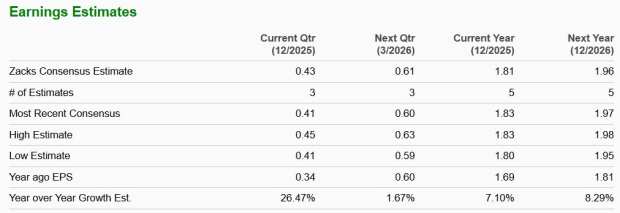

PPL’s Earnings Estimates Going Up

PPL expects its 2025 earnings estimate within the vary of $1.78-$1.84 per share. The Zacks Consensus Estimate for PPL’s 2025 and 2026 earnings per share signifies a yr over yr improve of seven.1% and eight.29%, respectively.

Picture Supply: Zacks Funding Analysis

One other utility, DTE Vitality DTE, working in the identical house, can also be making substantial investments like PPL to improve its infrastructure. The Zacks Consensus Estimate for DTE’s 2025 and 2026 earnings per share signifies a year-over-year improve of 5.9% and seven.1%, respectively.

PPL’s Capital Return Program

The corporate has been distributing dividends to its shareholders for a very long time and plans to extend dividends yearly within the vary of 6-8% at the least by 2028, topic to the board’s approval. The corporate’s present quarterly dividend charge is 27.25 cents, leading to an annual dividend of $1.09 per share. The present dividend yield is 2.99%, which is best than the S&P 500 group’s yield of 1.54%.

PPL has raised dividends for its shareholders 4 occasions prior to now 5 years. Verify PPL’s dividend historical past right here.

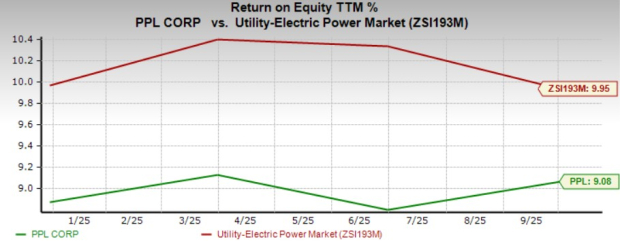

PPL Inventory Returns Decrease Than the Business

Return on Fairness (“ROE”) reveals how successfully an organization’s administration is using traders’ cash to generate returns. ROE of PPL is a tad decrease than its business. The present ROE of the corporate is 9.08% in contrast with its business’s 9.95%.

Picture Supply: Zacks Funding Analysis

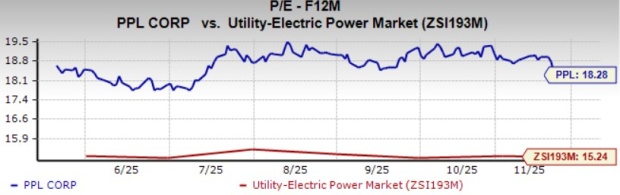

PPL Inventory Trades at a Premium

PPL Company is at present valued at a premium in contrast with its business on a ahead 12-month P/E foundation. The inventory is buying and selling at P/E F12M of 18.28X in contrast with its business’s 15.24X.

Picture Supply: Zacks Funding Analysis

Rounding Up

PPL is well-positioned to profit from the rising demand for clear power throughout its service areas. The corporate is making investments to broaden its operations to fulfill rising demand. PPL’s potential to get better greater than 60% of its capital expenditures in actual time supplies flexibility to effectively fund long-term initiatives.

PPL is growing shareholders’ worth by making common dividend funds and its earnings estimates are additionally transferring up.

But, PPL Company’s shares at present commerce at a premium and its returns stay barely under the business common. So, the brand new traders ought to watch for a greater entry level so as to add this Zacks Rank #3 (Maintain) inventory to their portfolio.

You’ll be able to see the whole record of right this moment’s Zacks #1 Rank (Robust Purchase) shares right here.

Zacks’ Analysis Chief Names “Inventory Most More likely to Double”

Our group of consultants has simply launched the 5 shares with the best chance of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This high choose is a little-known satellite-based communications agency. Area is projected to change into a trillion greenback business, and this firm’s buyer base is rising quick. Analysts have forecasted a significant income breakout in 2025. After all, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our High Inventory And 4 Runners Up

PPL Company (PPL) : Free Inventory Evaluation Report

Xcel Vitality Inc. (XEL) : Free Inventory Evaluation Report

DTE Vitality Firm (DTE) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.