Investor confidence in Lululemon LULU has slipped because the athletic attire chief contends with slower development and tightening margins.

Slowing Lululemon’s growth has been mounting value pressures, most notably increased import tariffs. That stated, buyers are actually questioning if Lululemon can change this ailing outlook narrative when it stories its This autumn outcomes after-market hours on Tuesday, March 17.

Efficiency Overview & CEO Search

Main as much as its This autumn report, LULU shares have dropped 50% within the final yr and are buying and selling close to a 52-week low of $156.

Regardless of constantly exceeding EPS expectations, as illustrated by the inexperienced arrows within the Worth, Consensus, and Shock chart, the steep decline in Lululemon’s inventory continued after offering weaker-than-expected This autumn steerage in September resulting from softer demand in its core U.S. market.

Weaker U.S. gross sales and shareholder strain led to the resignation of former CEO Calvin McDonald, who stepped down on the finish of January. McDonald will stay an advisor by way of the top of the month, as Lululemon’s board searches for his successor, with two senior executives being in cost as interim co-CEOs in the meanwhile.

Picture Supply: Zacks Funding Analysis

Lululemon’s This autumn Expectations

Lululemon’s This autumn gross sales are anticipated to be nearly flat from a yr in the past at $3.6 billion. On the underside line, This autumn EPS is anticipated at $4.77, a 22% drop from $6.14 per share within the prior yr quarter.

Nevertheless, Lululemon has exceeded the Zacks EPS Consensus for a exceptional 22 consecutive quarters, posting a median earnings shock of seven.79% in its final 4 quarterly stories.

Rounding out its fiscal 2026, Lululemon’s full-year EPS is anticipated to be down 11% to $13.04, even with annual gross sales thought to have elevated over 4% to $11.08 billion.

Picture Supply: Zacks Funding Analysis

Steering Expectations

After all, the flexibility to offer favorable steerage can be most important to LULU’s rebound prospects. Lululemon usually offers quarterly and full-year steerage for each income and EPS.

Maintaining this in thoughts, Wall Avenue expects Lululemon’s Q1 gross sales to be up 5% yr over yr to $2.49 billion, with whole gross sales for FY27 anticipated to be up 5% as nicely to $11.62 billion. EPS for Q1 is anticipated at $2.31, with full-year FY27 EPS projected at $12.77, declines of roughly 11% and a pair of%, respectively.

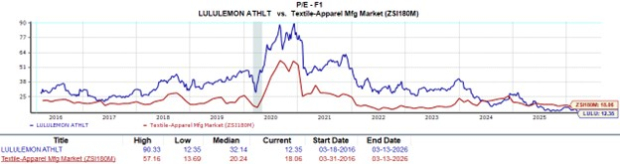

LULU’s Complexing Valuation & Capital Effectivity

Buying and selling at its least expensive P/E valuation in a decade at 12X ahead earnings, LULU trades intriguingly under its Zacks Textile-Attire Business common of 18X and provides an excellent sharper low cost to the benchmark S&P 500.

Picture Supply: Zacks Funding Analysis

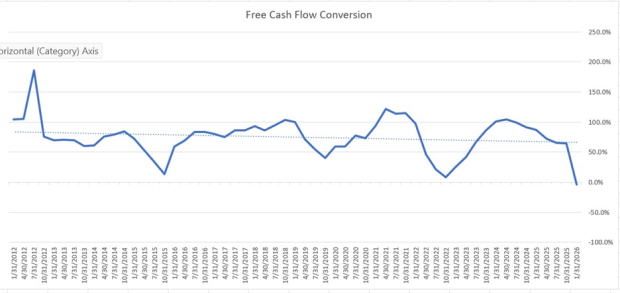

LULU can be on the usually most popular stage of lower than 2X ahead gross sales, and stands out by way of liquidity metrics like money move per share (CFPS).

Though Lululemon has an outstanding CFPS of 18X in comparison with the business common of round 2X, it is noteworthy that the corporate’s free money move (FCF) conversion charge has turned adverse (-3.8%). Whereas this may very well be momentary, the customarily most popular FCF conversion charge is round 75-80% or increased, with Lululemon’s usually at 65-70%.

In different phrases, the excessive CFPS exhibits that Lululemon’s enterprise generates important money, but the deteriorating FCF conversion is an indication that the corporate has develop into much less environment friendly at turning this into true free money flows resulting from increased working capital wants and elevated CapEx.

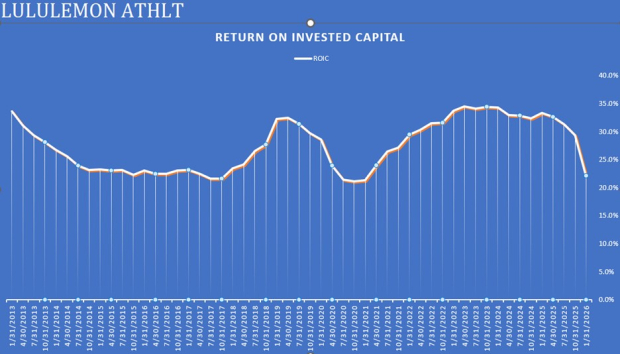

Picture Supply: Zacks Funding AnalysisThen again, Lululemon’s return on invested capital (ROIC) has remained above the admirable stage of 20% or increased and exhibits effectivity in utilizing its capital investments to generate income. This is among the clearest indicators of long-term shareholder worth, nevertheless it’s value noting that Lululemon’s ROIC has fallen sharply as nicely.

Picture Supply: Zacks Funding Analysis

Abstract & Ultimate Ideas

Lululemon inventory is actually drawing consideration as a possible rebound prospect, contemplating LULU is at traditionally low-cost ranges by way of P/E and nonetheless has a favorably excessive ROIC. For now, LULU lands a Zacks Rank #3 (Maintain) as delivering sturdy This autumn outcomes and favorable steerage can be essential to extra upside.

Whereas there nonetheless seems to be long-term worth, extra strategic clarification can be wanted surrounding Lululemon’s management transition and progress on tariffs, together with the restructuring of its provide chain and slicing inner prices.

Zacks’ Analysis Chief Picks Inventory Most More likely to “At Least Double”

Our consultants have revealed their Prime 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. After all, all our picks aren’t winners however this one may far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our Prime Inventory to Double (Plus 4 Runners Up) >>

lululemon athletica inc. (LULU) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.