As an AI cloud supplier that has been backed by investments from Nvidia NVDA, CoreWeave CRWV inventory continues to be up a formidable +90% since launching its IPO earlier within the 12 months.

That mentioned, CRWV has slid greater than 50% from its excessive of $187 a share as traders have turn out to be involved over CoreWeave’s slowing development, heavy debt, and weaker-than-expected steering.

For sure, this has drawn consideration to the notion that the AI increase could also be peaking, a minimum of for CoreWeave.

Picture Supply: Zacks Funding Analysis

Why CoreWeave’s Steering Has Traders Involved

Regardless of comfortably exceeding its Q3 expectations in November and reporting document income development, CoreWeave gave disappointing full-year steering that has contributed to its latest inventory decline. Whereas CoreWeave’s Q3 gross sales of $1.34 billion greater than doubled 12 months over 12 months, its development price is predicted to decelerate, elevating doubts about sustainability, particularly for the reason that firm isn’t worthwhile but.

Including to profitability considerations, CoreWeave’s working margins have fallien beneath 4%. In regard to its decelerating development price, CoreWeave reduce its fiscal 2025 income forecast to between $5.05-$5.15 billion, down from prior steering of $5.35 billion as a result of delays in main buyer contracts and information heart development setbacks. Nonetheless, CoreWeave has secured new offers with Meta Platforms META and OpenAI, with the corporate insisting that its lowered forecast displays timing points relatively than demand weak point.

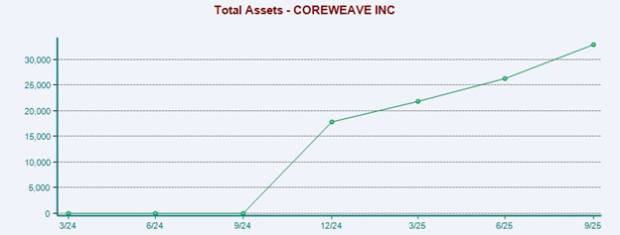

Monitoring CoreWeave’s Stability Sheet

What can be regarding traders is that CoreWeave carries important debt, and rising curiosity bills might make profitability more durable to realize. Nonetheless, CoreWeave is solvent, having $32.91 billion in complete belongings, though this isn’t advantageously above its complete liabilities of $29 billion. It’s noteworthy that CoreWeave has seen a pleasant uptick in money and equivalents since going public, which presently sits at round $2.53 billion.

Picture Supply: Zacks Funding Analysis

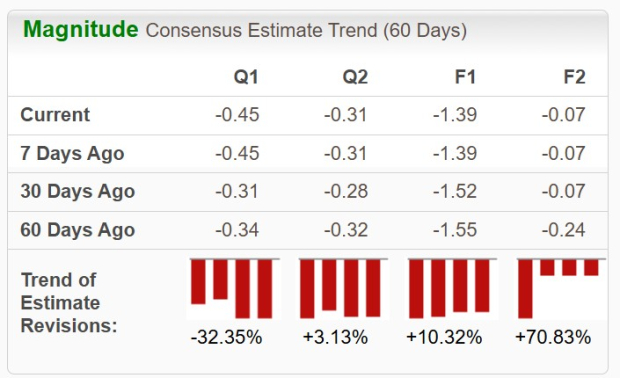

Monitoring Coreweave’s EPS Revisions

Posting a smaller-than-expected adjusted lack of -$0.08 a share throughout Q3, CoreWeave’s full-year EPS is now anticipated at -$1.39 in comparison with estimates of -$1.52 a month in the past. Optimistically, CoreWeave is predicted to maneuver nearer to the profitability line subsequent 12 months. Plus, during the last 60 days, FY26 EPS revisions are as much as -$0.07 from estimates of -$0.24.

Picture Supply: Zacks Funding Analysis

CoreWeave’s Affordable P/S Ratio

Value-to-sales could also be one of the best ways to gauge CoreWeave’s basic worth to traders for the time being, and CRWV does have an inexpensive ahead P/S ratio of 5X. Contemplating the price-to-sales premiums that high-growth tech shares can command, CoreWeave’s P/S ratio is pleasantly beneath the benchmark S&P 500, with Nvidia, for instance, at 22X and Meta Platforms at 8X.

Plus, primarily based on Zacks’ estimates, CoreWeave’s annual gross sales are projected to leap to $11.51 billion in FY26, and the corporate has an enormous income backlog value $56 billion.

Picture Supply: Zacks Funding Analysis

Conclusion & Last Ideas

Though CoreWeave continues to be rising quickly, its transitioning from explosive growth to steadier, backlog-driven development, which is much less thrilling for traders chasing AI hypergrowth tales.

Coreweave’s means to handle debt, execute on its backlog, and stabilize margins will decide whether or not its latest setback is momentary or an indication of deeper structural challenges. It might be too quickly to purchase the dip, however CoreWeave’s place as an AI infrastructure developer may nonetheless be very profitable with CRWV touchdown a Zacks Rank #3 (Maintain).

Analysis Chief Names “Single Finest Decide to Double”

From 1000’s of shares, 5 Zacks specialists every have chosen their favourite to skyrocket +100% or extra in months to come back. From these 5, Director of Analysis Sheraz Mian hand-picks one to have essentially the most explosive upside of all.

This firm targets millennial and Gen Z audiences, producing practically $1 billion in income final quarter alone. A latest pullback makes now a perfect time to leap aboard. After all, all our elite picks aren’t winners however this one may far surpass earlier Zacks’ Shares Set to Double like Nano-X Imaging which shot up +129.6% in little greater than 9 months.

Free: See Our High Inventory And 4 Runners Up

CoreWeave Inc. (CRWV) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.

Maintain Its Triangle Breakout?")