")

Taiwan Semiconductor (TSM) is the world’s largest and most superior contract semiconductor producer, or “foundry.” Based in 1987 and headquartered in Hsinchu, Taiwan, TSM produces chips for a variety of industries, together with shopper electronics, automotive, and now the Synthetic Intelligence industries.

The corporate is understood for its cutting-edge expertise and innovation, particularly in superior course of nodes like 5nm and 3nm, making it a vital provider for tech giants reminiscent of Apple, AMD, and Nvidia. TSM’s dominant place within the semiconductor trade makes it a key participant within the international tech provide chain and a premier asset for traders.

Not solely does Taiwan Semiconductor play a important function within the expertise sector, but it surely additionally boasts a high Zacks Rank, robust earnings progress forecasts and an inexpensive valuation. Moreover, its inventory has compounded at a formidable 17.1% annualized during the last 20 years, greater than double the market common, and appears doubtless that it’s going to proceed to outperform based mostly on present estimates.

Picture Supply: Zacks Funding Analysis

AI Enlargement Continues to Increase Gross sales at TSM

Taiwan Semiconductor, who shares month-to-month updates on its revenues, introduced that in July revenues grew an unimaginable 44.7% year-on-year (YoY) to $7.9 billion. This progress outpaces the earlier month (32.9%) and suggests robust ongoing demand for AI chips, notably from main purchasers like Nvidia and Apple.

At its most up-to-date quarterly assembly, TSM’s CEO, C.C. Wei, indicated the corporate might doubtlessly elevate costs as clients shift to its most superior applied sciences. Regardless of investor issues over the AI increase’s sustainability, TSM stays well-positioned for strong efficiency, notably with its involvement in high-performance computing led by AI, which accounted for 52% of its latest income.

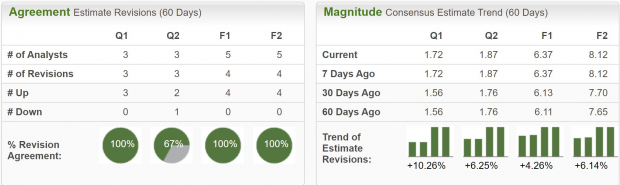

Analysts Elevate Earnings Forecasts at Taiwan Semiconductor

Over the past month, analysts have close to unanimously raised earnings estimates throughout timeframes, giving TSM a Zacks Rank #1 (Robust Purchase) ranking. This high rank considerably will increase the percentages of a near-term rally and confirms the continued power of the underlying enterprise.

Over the following three to 5 years, earnings are forecast to develop 26.5% yearly, which is an unimaginable tempo for such a mammoth firm.

Picture Supply: Zacks Funding Analysis

Taiwan Semiconductor Shares Commerce at a Truthful Valuation

Immediately, Taiwan Semiconductor is buying and selling at a one 12 months ahead earnings a number of of 25.8x. That is above the broad market common and above its five-year median of 21x. Nonetheless, it must be famous that the super tailwind from AI is an inexpensive trigger for this elevated earnings a number of as TSM and the trade as an entire could also be rising quicker than latest historical past.

Moreover, with earnings anticipated to develop 26.5% yearly, TSM really has a PEG ratio beneath 1, which is a reduction based mostly on the metric. On the very least, TSM is buying and selling close to honest worth, with expectations of each gross sales and earnings to develop above 20% yearly.

Picture Supply: Zacks Funding Analysis

Ought to Traders Purchase Taiwan Semiconductor Inventory?

Given the spectacular progress trajectory and robust monetary outlook, Taiwan Semiconductor presents a compelling funding alternative. The corporate’s dominant place within the semiconductor trade, coupled with its important function in AI and high-performance computing, helps a strong long-term progress narrative.

For traders searching for publicity to the quickly increasing AI sector and a key participant within the international tech provide chain, Taiwan Semiconductor is well-positioned to ship robust returns. Regardless of the marginally elevated valuation, the corporate’s progress prospects, and important trade function make it a worthy consideration for any growth-oriented portfolio.

Analysis Chief Names “Single Greatest Choose to Double”

From 1000’s of shares, 5 Zacks specialists every have chosen their favourite to skyrocket +100% or extra in months to return. From these 5, Director of Analysis Sheraz Mian hand-picks one to have probably the most explosive upside of all.

This firm targets millennial and Gen Z audiences, producing almost $1 billion in income final quarter alone. A latest pullback makes now a really perfect time to leap aboard. In fact, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Nano-X Imaging which shot up +129.6% in little greater than 9 months.

Free: See Our Prime Inventory And 4 Runners Up

Taiwan Semiconductor Manufacturing Firm Ltd. (TSM) : Free Inventory Evaluation Report

To learn this text on Zacks.com click on right here.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.