")

The Zacks Rank signifies that TAT Applied sciences TATT is a inventory that traders could wish to take income in immediately.

Buying and selling close to an all-time excessive of $53 a share, TATT has been lifted by positve sentiment for aerospace and protection shares that was reignited following the U.S navy operations in Venezuela.

Nevertheless, TAT inventory is now buying and selling at pretty stretched ranges as a supplier of engineered options for plane, together with elements and upkeep providers for F-16 fighter jets.

With it definitely showing to be a perfect time to fade the newest rally, TAT inventory lands a Zacks Rank #5 (Sturdy Promote) and is the Bear of the Day.

Picture Supply: Zacks Funding Analysis

A Small Fish in a Large Pond

Whereas the F-16 stays probably the most extensively used and versatile plane in navy service, the hype for TAT’s inventory could also be nicely overdone at this level with it being noteworthy that the extra profitable contracts and manufacturing of F-16s nonetheless go solely via Lockheed Martin LMT.

Moreover, a surprisingly giant ecosystem of firms carry out upkeep restore overhaul (MRO), upgrades, and sustainment for the F-16 worldwide, together with Amentum Holdings AMTM, AAR Corp AIR, and Prime Aces, together with a slew of different personal corporations.

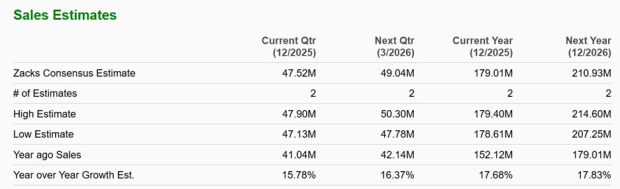

Income Issues & Weak Earnings Momentum

What units the overhyped time to promote alarm off is that TAT is just not an organization that just lately launched an IPO, however as a substitute has been public since 1987, and regardless of increased demand in recent times, is bringing in lower than $300 million in annual gross sales.

TAT most just lately missed Q3 gross sales estimates of $46.26 million in November and got here wanting the Q3 EPS Consensus of $0.40 as nicely.

Picture Supply: Zacks Funding Analysis

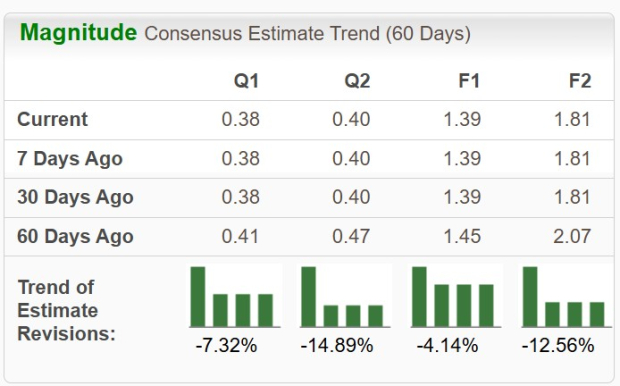

Following the lackluster Q3 outcomes, EPS revisions have remained decrease during the last 60 days, down by 4% and 12% for fiscal 2025 and FY26, respectively.

Picture Supply: Zacks Funding Analysis

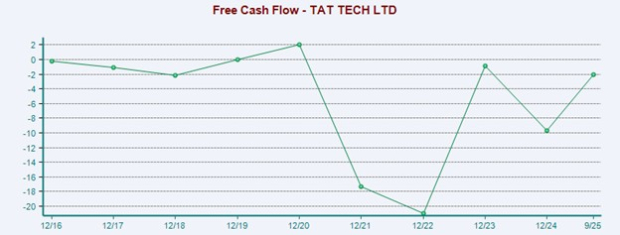

Stretched Valuation & Adverse Free Money Move

The elephant within the room is that many analysts have identified that TAT is nearing the overvalued zone. TAT’s 28X ahead earnings a number of and ahead worth to gross sales ratio of 3X could not look like worrisome, however it is a far stretch from the place it has traded prior to now, and the corporate has didn’t generate constructive free money stream, which weakens intrinsic worth.

Picture Supply: Zacks Funding Analysis

Conclusion & Ultimate Ideas

It wouldn’t be shocking if a sell-off have been in retailer for TAT Applied sciences’ inventory or if an prolonged correction led to the corporate giving again a lot of its current positive factors.

Tright here is little doubt that TAT has benefited from elevated protection spending, however now seems to be a perfect time to take income with its present inventory worth beginning to mirror hypothesis and never enhancing enterprise fundamentals.

5 Shares Set to Double

Every was handpicked by a Zacks professional as the favourite inventory to achieve +100% or extra within the months forward. They embody

Inventory #1: A Disruptive Drive with Notable Development and Resilience

Inventory #2: Bullish Indicators Signaling to Purchase the Dip

Inventory #3: One of many Most Compelling Investments within the Market

Inventory #4: Chief In a Pink-Sizzling Trade Poised for Development

Inventory #5: Trendy Omni-Channel Platform Coiled to Spring

Many of the shares on this report are flying underneath Wall Road radar, which gives an important alternative to get in on the bottom ground. Whereas not all picks will be winners, earlier suggestions have soared +171%, +209% and +232%.

Obtain Atomic Alternative: Nuclear Power’s Comeback free in the present day.

TAT Applied sciences Ltd. (TATT) : Free Inventory Evaluation Report

Lockheed Martin Company (LMT) : Free Inventory Evaluation Report

AAR Corp. (AIR) : Free Inventory Evaluation Report

Amentum Holdings, Inc. (AMTM) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.