")

JD.com Firm Overview

Based mostly in Beijing, Zacks Rank #5 (Sturdy Promote) inventory JD.com (JD) one of many largest Chinese language e-commerce and know-how corporations. Also called Jingdong, JD.com separates itself from the competitors by being an basically vertically built-in e-commerce retailer. JD holds its personal stock, is answerable for its personal logistics and deliveries, and supplies its personal customer support. JD is just like Amazon (AMZN) in that it sells all kinds of merchandise on its e-commerce platform, together with clothes, groceries, electronics, and extra. Past e-commerce, JD additionally operates well being, know-how, actual property, and industrial section companies. Moreover, JD owns Ochama, a European-based retail model with operations within the Netherlands France, and Poland.

JD Suffers from Relative Worth Weak point Vs. Friends

Legendary development investor William O’Neil as soon as proclaimed that Wall Avenue’s nice paradox is, “Shares that appear too excessive in worth and dangerous for many traders normally go increased and shares that appear low and low cost typically go decrease.” I’ve largely found that most of the time, O’Neil’s paradox involves fruition. That’s unhealthy information for JD shares, which commerce at $30 and are properly off their all-time excessive of >$100. Moreover, relative worth motion can present traders with invaluable clues. At the moment, JD shares exhibit troubling relative weak spot and are -15.02% over the previous 12 months, far underperforming high rivals like Pinduoduo (PDD) and Alibaba (BABA) that are up 20.76% and 83.76% respectively.

Picture Supply: TradingView

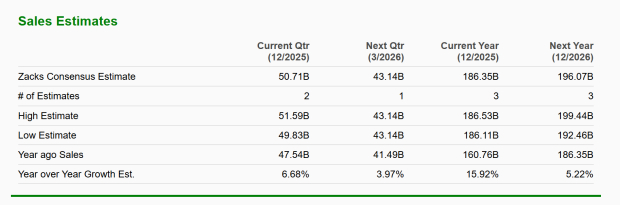

JD: Slowing Gross sales Development

JD gross sales development is declining at an alarming fee. For the present quarter, Zacks Consensus Analyst Estimates recommend that earnings development will likely be simply 6.68%%. In the meantime, Zacks Consensus Estimates recommend sluggish annual income development of 5.22% in 2026.

Picture Supply: Zacks Funding Analysis

JD Meals Supply Enterprise is a Headwind

JD is making an aggressive play for the Chinese language meals supply market. Whereas the variety of customers for the corporate’s Uber (UBER) Eats or DoorDash (DASH) like enterprise has elevated, the section has produced important losses up to now. Worse nonetheless, the corporate should make investments important capital preserve its popularity for quick and dependable supply in a extremely aggressive market.

Backside Line

JD.com at the moment face a troublesome uphill battle. Between alarming slowdowns in development and the monetary pressure of enlargement into the aggressive meals ship market, JD’s “low cost” share worth could also be warranted.

Free Report: Benefiting from the 2nd Wave of AI Explosion

The subsequent part of the AI explosion is poised to create important wealth for traders, particularly those that get in early. It’s going to add actually trillion of {dollars} to the financial system and revolutionize almost each a part of our lives.

Traders who purchased shares like Nvidia on the proper time have had a shot at big good points.

However the rocket experience within the “first wave” of AI shares could quickly come to an finish. The sharp upward trajectory of those shares will start to stage off, leaving exponential development to a brand new wave of cutting-edge corporations.

Zacks’ AI Increase 2.0: The Second Wave report reveals 4 under-the-radar corporations which will quickly be shining stars of AI’s subsequent leap ahead.

Entry AI Increase 2.0 now, completely free >>

Amazon.com, Inc. (AMZN) : Free Inventory Evaluation Report

JD.com, Inc. (JD) : Free Inventory Evaluation Report

Alibaba Group Holding Restricted (BABA) : Free Inventory Evaluation Report

PDD Holdings Inc. Sponsored ADR (PDD) : Free Inventory Evaluation Report

Uber Applied sciences, Inc. (UBER) : Free Inventory Evaluation Report

DoorDash, Inc. (DASH) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.

Soars 6.5% Forward of FY25 Earnings")