")

Boise Cascade Firm BCC is an engineered wooden merchandise and plywood large. BCC inventory has tumbled 50% previously 12 months as Wall Road dumps the inventory primarily based on quite a lot of industry-specific headwinds and macroeconomic challenges.

The engineered wooden merchandise maker offered disappointing steerage as soon as once more when it reported its third quarter 2025 outcomes on November 3.

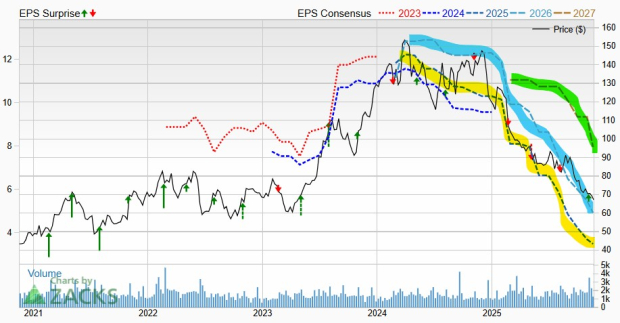

Boise Cascade’s destructive earnings per share (EPS) revisions following its launch earn the inventory a Zacks Rank #5 (Robust Promote) and extend its string of downward EPS revisions.

Ought to Traders Keep Away from BCC Inventory for Now?

Boise Cascade is a number one producer of engineered wooden merchandise and plywood. The corporate can also be an enormous participant within the wholesale distribution of constructing merchandise within the U.S.

BCC posted a powerful stretch of top-line enlargement between 2012 and 2022, highlighted by 18% progress in 2020 and 45% in 2021, pushed by the wild Covid-driven housing and residential enchancment increase.

Boise Cascade adopted that up with one other 6% gross sales progress in 2022 earlier than tumbling in opposition to a troublesome to compete in opposition to stretch and broader headwinds which might be difficult your complete housing-related market.

Picture Supply: Zacks Funding Analysis

Mortgage charges soared off their lows, whereas housing costs and inflation have skyrocketed as properly, drying up the housing market, crushing demand. On high of that, commodity costs are hurting Boise Cascade. The huge Covid-era pull ahead can also be onerous to overstate and overcome within the brief run because it disrupted a lot.

The corporate’s gross sales fell 19% in 2023 and a pair of% in 2024, whereas its earnings tanked roughly 40% and 20%, respectively. Most not too long ago, Boise Cascade adjusted EPS plummeted 75% YoY in Q3 FY25 on 3% decrease gross sales, because it faces “subdued demand and commodity pricing headwinds.”

BCC’s This autumn earnings estimate tanked 51% since its early November launch, with its fiscal 2025 estimate 18% decrease and its FY26 consensus down 18%. This backdrop lands Boise Cascade its Zacks Rank #5 (Robust Promote), extending its practically two-year run of plummeting earnings estimates.

Picture Supply: Zacks Funding Analysis

The corporate did announce on November 18 that it reached an settlement to buy “Humphrey Firm, Inc., a number one two-step distributor of constructing supplies situated in Chicopee, Massachusetts, with roughly $145 million in income over the past 12 months.” The transfer helps BCC increase its attain and develop in the important thing northeast area.

The inventory may additionally probably profit from a possible rotation out of tech. Traders excessive on Boise Cascade long-term may take into account including BCC to their watchlists as an alternative of shopping for it proper now amid all of the headwinds and unknowns surrounding the housing market.

5 Shares Set to Double

Every was handpicked by a Zacks knowledgeable because the #1 favourite inventory to realize +100% or extra within the coming yr. Whereas not all picks may be winners, earlier suggestions have soared +112%, +171%, +209% and +232%.

A lot of the shares on this report are flying beneath Wall Road radar, which supplies an important alternative to get in on the bottom ground.

Immediately, See These 5 Potential House Runs >>

Boise Cascade, L.L.C. (BCC) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.