")

Figuring out weak shares to keep away from, or potential quick candidates, is commonly extra simple than discovering the subsequent massive winner. The fairness market is extremely aggressive, and plenty of listed firms finally delist over the long-term. Whereas some buyers seek for accounting points or speculative bubbles when attempting to find shorts, the extra dependable strategy is often easier: give attention to companies dealing with slowing demand, deteriorating fundamentals, or structural headwinds.

To floor all these names, I sometimes start with a display within the Zacks Inventory Screener. My baseline filters embrace a Zacks Rank #5 (Sturdy Promote), destructive five-year trailing gross sales development, and share value efficiency lagging the broader market. This simple course of persistently highlights firms exhibiting indicators of sustained operational strain. One inventory that lately surfaced from that display is Avantor (AVTR). With declining gross sales developments, downward earnings revisions, and chronic value weak point, the setup suggests a reputation buyers might wish to strategy with warning or keep away from altogether.

Picture Supply: Zacks Funding Analysis

Avantor Shares Plummet Amid Deteriorating Fundamentals

Avantor’s basic outlook stays below strain. Over the previous 4 years, annual income has fallen roughly 13%, declining in every consecutive 12 months throughout that interval. Profitability has weakened as nicely, with internet margins compressing from about 12% to 9%, reflecting each softer demand and working strain. Consensus forecasts name for gross sales to slide one other 0.7% this 12 months, adopted by solely a modest 2.4% rebound subsequent 12 months, which is hardly the kind of development profile that sometimes helps sustained share-price power.

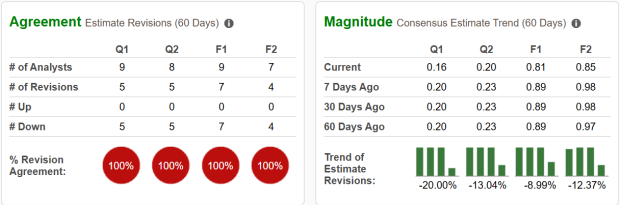

On the identical time, the earnings outlook has steadily deteriorated. Analysts have been revising estimates decrease since 2022, and the cuts have continued lately throughout a number of timeframes. Over simply the previous week, consensus projections for the present quarter have dropped about 20%, whereas full-year estimates have fallen roughly 9%. This sample of persistent downward revisions has pushed Avantor right into a Zacks Rank #5 (Sturdy Promote), reinforcing the destructive basic pattern surrounding the inventory.

Picture Supply: Zacks Funding Analysis

Ought to Traders Keep away from AVTR Inventory?

Given the mixture of declining income, margin compression, and chronic earnings downgrades, Avantor at present lacks the basic momentum that sometimes helps sturdy inventory efficiency. Firms dealing with multi-year gross sales strain and ongoing estimate cuts usually battle to regain investor confidence, as every revision decrease tends to reset expectations and weigh on valuation multiples.

Whereas sharp selloffs can generally create turnaround alternatives, the important thing sign to look at is stabilization in each gross sales developments and analyst revisions. At current, neither has clearly materialized. Till the corporate demonstrates constant demand enchancment, margin restoration, or a sustained halt in estimate reductions, the risk-reward profile seems unfavorable in comparison with different alternatives available in the market.

For buyers targeted on capital preservation, AVTR could also be higher considered as a reputation to keep away from for now fairly than one to aggressively accumulate.

5 Shares Set to Double

Every was handpicked by a Zacks knowledgeable because the #1 favourite inventory to achieve +100% or extra within the coming 12 months. Whereas not all picks could be winners, earlier suggestions have soared +112%, +171%, +209% and +232%.

Many of the shares on this report are flying below Wall Avenue radar, which gives an awesome alternative to get in on the bottom ground.

At the moment, See These 5 Potential Dwelling Runs >>

Avantor, Inc. (AVTR) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.