Alibaba BABA is selling fast commerce as a key progress driver, with revenues surging 60% 12 months over 12 months within the second quarter of fiscal 2026, pushed by robust order momentum and enlargement of Taobao On the spot Commerce. This progress is boosting consumer engagement, growing month-to-month energetic customers on the Taobao app and supporting buyer administration revenues by greater visitors and monetization, although its rising prices have gotten a rising problem to margins.

Alibaba has acknowledged that heavy spending on subsidies, logistics and consumer expertise is weighing on profitability, significantly inside the China e-commerce section, which plunged 76% 12 months over 12 months within the second quarter of fiscal 2026. Excluding fast commerce losses, core China e-commerce EBITA would have posted mid-single-digit progress — underscoring that fast commerce is presently the dominant drag on profitability and affecting near-term margins.

Value developments reinforce this stress. Gross sales and advertising and marketing bills jumped sharply to just about 27% of revenues, reflecting intense competitors in China’s prompt supply and native commerce markets. On the similar time, money stream has deteriorated meaningfully. Money technology has softened, largely on account of continued investments in fast commerce and supporting infrastructure.

Administration has been clear that adjusted EBITA might fluctuate within the coming quarters as competitors stays intense and funding ranges keep excessive. With prices prone to improve, EBITA volatility is prone to proceed, suggesting that margin stress shouldn’t be solely mounting however might persist longer than anticipated.

Alibaba Faces Stiff Competitors in E-Commerce House

JD.com JD poses stiff competitors to Alibaba by specializing in a self-operated, price-competitive and supply-chain-driven mannequin. JD.com advantages from robust high quality management, sooner supply and excessive buyer belief, particularly in electronics and residential home equipment. Within the third quarter of 2025, JD.com posted income progress of 14.9% to RMB299.1 billion, supported by retail enlargement and worth competitiveness, whilst greater logistics prices stress margins — highlighting Alibaba’s intensifying aggressive panorama.

PDD Holdings PDD intensifies competitors with Alibaba by its low-cost, social commerce mannequin. PDD Holdings emphasizes worth effectivity, robust consumer engagement and a capital-light construction that helps excessive profitability. Within the third quarter of 2025, PDD Holdings delivered strong income progress and powerful web revenue features, pressuring Alibaba’s core platforms. Its capability to scale shortly, monetize retailers and keep wholesome margins highlights rising aggressive stress.

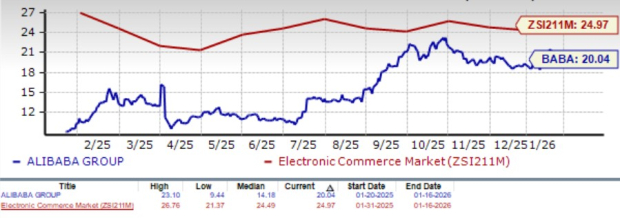

BABA’s Share Worth Efficiency, Valuation & Estimates

BABA shares have gained 37.5% prior to now six-month interval, outperforming the Zacks Web – Commerce business and the Zacks Retail-Wholesale sector’s progress of three.1% and 6.4%, respectively.

BABA’s Six Month Worth Efficiency

Picture Supply: Zacks Funding Analysis

From a valuation standpoint, BABA inventory is presently buying and selling at a ahead 12-month Worth/Earnings ratio of 20.04X in contrast with the business’s 24.97X. BABA has a Worth Rating of F.

BABA’s Valuation

Picture Supply: Zacks Funding Analysis

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $6.10 per share, down by 5% over the previous 30 days and indicating a 32.3% year-over-year decline.

Picture Supply: Zacks Funding Analysis

Alibaba presently carries a Zacks Rank #5 (Robust Promote).

You’ll be able to see the entire checklist of in the present day’s Zacks #1 Rank (Robust Purchase) shares right here.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unbelievable demand for knowledge is fueling the market’s subsequent digital gold rush. As knowledge facilities proceed to be constructed and continuously upgraded, the businesses that present the {hardware} for these behemoths will develop into the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to reap the benefits of the subsequent progress stage of this market. It makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is strictly the place you need to be.

See This Inventory Now for Free >>

JD.com, Inc. (JD) : Free Inventory Evaluation Report

Alibaba Group Holding Restricted (BABA) : Free Inventory Evaluation Report

PDD Holdings Inc. Sponsored ADR (PDD) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.