Archer Daniels Midland Firm ADM posted third-quarter 2025 outcomes, whereby the highest line fell wanting the Zacks Consensus Estimate however elevated yr over yr. In the meantime, earnings surpassed the Zacks Consensus Estimate however declined from the identical interval final yr.

Archer Daniels Midland Firm Value, Consensus and EPS Shock

Archer Daniels Midland Firm price-consensus-eps-surprise-chart | Archer Daniels Midland Firm Quote

Perception Into ADM’s Q3 Efficiency

Adjusted earnings of 92 cents per share surpassed the Zacks Consensus Estimate of 89 cents. Nevertheless, the determine decreased from adjusted earnings of $1.09 per share within the year-ago quarter. On a reported foundation, Archer Daniels’ third-quarter earnings had been 22 cents per share, up from 4 cents within the year-ago quarter.

Revenues gained 2.2% yr over yr to $20.4 billion, however missed the consensus estimate of $20.7 billion.

Section-wise, revenues for Ag Providers & Oilseeds elevated 3.5% yr over yr to $15.6 billion, whereas Carbohydrate Options’ revenues decreased 5.9% yr over yr to $2.7 billion. Vitamin’s revenues rose 4.6% yr over yr to $1.92 billion. The Zacks Consensus Estimate for the segments’ revenues was pegged at $15.7 billion, $2.9 billion and $1.9 billion, respectively. Revenues from Different Enterprise are flat at $109 million in contrast with the determine within the prior-year interval.

The gross revenue decreased 7% yr over yr to $1.3 billion, whereas the gross margin stood at 6.2%. Promoting, common and administrative bills declined to $873 million from $905 million within the year-ago quarter.

Archer Daniels reported adjusted segmental working revenue of $845 million, down 19% from the year-ago quarter.

The corporate has a trailing four-quarter return on invested capital of 6.7% on an adjusted foundation.

ADM’s Segmental Working Revenue

Adjusted working revenue for Ag Providers & Oilseeds dropped 21% yr over yr to $379 million. The Ag Providers subsegment’s working revenue rose 78%, pushed by larger export exercise in North America and improved ends in South America. This quarter included $4 million in web optimistic mark-to-market (MTM) impacts, versus $50 million in web detrimental impacts a yr earlier.

The Crushing subsegment’s working revenue plunged 93% yr over yr on decrease margins ensuing from muted demand tied to the deferral of U.S. biofuel coverage and worldwide commerce challenges. There have been about $41 million of web optimistic mark-to-market timing impacts within the quarter towards zero of web detrimental impacts within the year-ago quarter.

Refined Merchandise and Different working revenue was down 3% from the prior yr, as biodiesel and refining margins had been affected by the delayed biofuel coverage, weighing on North American demand. The quarter included $8 million in web detrimental MTM impacts, versus $20 million within the prior-year interval. Fairness earnings from the corporate’s funding in Wilmar decreased by roughly 10% from the prior-year quarter.

The Carbohydrate Options phase posted an working revenue of $336 million within the third quarter of 2025, reflecting a 26% decline from the year-ago interval. Working revenue within the Starches & Sweeteners subsegment additionally fell 36% attributable to decrease world S&S demand, which pressured each volumes and margins. The subsegment additionally continued to face larger corn prices in EMEA stemming from corn high quality points, additional weighing on profitability.

International wheat milling efficiency remained comparatively secure versus the prior-year quarter, although final yr’s outcomes had benefited from $47 million in insurance coverage proceeds, amplifying the year-over-year comparability. Vantage Corn Processors posted a $46 million improve in working revenue, supported by sturdy export flows and elevated pricing amid decrease business stock ranges attributable to plant downtime from upkeep packages.

The Vitamin phase reported an working revenue of $130 million within the third quarter of 2025, marking a 24% improve from the identical interval final yr. Working revenue within the Human Vitamin subsegment gained 12% yr over yr. Inside this phase, Flavors noticed revenue progress, pushed by larger margins, significantly in North America. The Well being & Wellness class additionally contributed to the rise, benefiting from stronger biotics demand.

In the meantime, the Animal Vitamin subsegment posted an working revenue of $34 million, marking a 79% year-over-year upsurge, fueled by margin enlargement from a strategic deal with higher-value product strains and continued portfolio streamlining and price optimization initiatives.

Archer Daniels’ Different Financials

The corporate ended the quarter with money and money equivalents of $1.24 billion, long-term debt, together with present maturities, of $7.6 billion, and shareholders’ fairness of $22.5 billion. As of Sept. 30, 2025, ADM generated $5.77 billion in money from working actions. It paid out dividends of $743 million through the 9 months of 2025.

For 2025, based mostly on efficiency over the primary 9 months of the yr and present expectations relating to the timing of anticipated advantages from favorable biofuel coverage developments and the evolution of world commerce dynamics, the corporate has revised its full-year adjusted EPS steerage. Adjusted earnings are actually anticipated to be within the vary of $3.25 to $3.50 per share, in comparison with the earlier steerage of roughly $4.00.

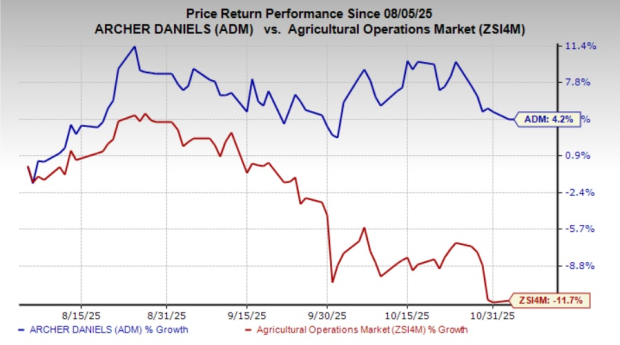

We observe that shares of this Zacks Rank #3 (Maintain) firm have gained 4.2% previously three months towards the business’s 11.7% decline.

ADM Inventory’s Value Efficiency

Picture Supply: Zacks Funding Analysis

Higher-Ranked Shares

Now we have highlighted three better-ranked shares from the Shopper Staples sector, specifically United Pure Meals, Inc. UNFI, PepsiCo, Inc. PEP and Ollie’s Discount Outlet Holdings OLLI.

United Pure is the main distributor of pure, natural and specialty meals and non-food merchandise. It presently sports activities a Zacks Rank #1 (Sturdy Purchase). You’ll be able to see the entire record of in the present day’s Zacks #1 Rank shares right here.

UNFI delivered an earnings shock of 416.2% within the trailing 4 quarters, on common. The Zacks Consensus Estimate for United Pure’s present fiscal-year gross sales and earnings signifies progress of two.5% and 167.6%, respectively, from the year-ago reported figures.

PepsiCo is without doubt one of the main world meals and beverage corporations. It presently carries a Zacks Rank #2 (Purchase).

The Zacks Consensus Estimate for PepsiCo’s present financial-year gross sales signifies year-over-year progress of 1.8%, whereas that for EPS suggests a decline of 0.6%. PEP has a trailing four-quarter detrimental earnings shock of 1.1%, on common.

Ollie’s Discount is a worth retailer of brand-name merchandise at drastically diminished costs and presently carries a Zacks Rank #2. OLLI delivered a trailing four-quarter earnings shock of 4.2%, on common.

The Zacks Consensus Estimate for Ollie’s Discount’s present fiscal-year gross sales and earnings signifies 16.4% and 16.5% rallies, respectively, from the year-earlier reported ranges.

Archer Daniels Midland Firm (ADM) : Free Inventory Evaluation Report

PepsiCo, Inc. (PEP) : Free Inventory Evaluation Report

United Pure Meals, Inc. (UNFI) : Free Inventory Evaluation Report

Ollie’s Discount Outlet Holdings, Inc. (OLLI) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.