")

Eagle Supplies is a provider of building supplies in the US. The corporate produces and provides cement, concrete and aggregates, gypsum wallboard, and recycled paperboard. Working through a vertically built-in enterprise mannequin, its merchandise are utilized in business and residential building throughout the nation together with builders, contractors, and infrastructure initiatives.

Key challenges stay for Eagle in 2026. Its wallboard enterprise has been struggling currently resulting from gradual housing exercise. Wallboard volumes fell about 14% year-over-year in fiscal Q3, with costs dropping 5% amid value pressures. That is the corporate’s key publicity to housing begins, which stay challenged by excessive charges and affordability points. The broader housing restoration relies on decrease mortgage charges, which can stay elevated given lingering inflation.

Eagle operates in a extremely cyclical enterprise that’s tied to residential housing and broader building spending. As we’ll see, analysts have been reducing earnings estimates currently, placing downward stress on the inventory. Financial slowdowns or delays in infrastructure initiatives may exacerbate this stress.

As well as, margins are experiencing compression as enter prices stay unstable. The shortage of development potential within the yr forward merely doesn’t warrant a bullish stance.

The Zacks Rundown

A Zacks Rank #5 (Robust Promote) inventory, Eagle Supplies EXP is a element of the Constructing Merchandise – Concrete and Aggregates trade group, which at the moment ranks within the backside 15% out of roughly 250 Zacks Ranked Industries. As such, we count on this trade group as a complete to underperform the market over the subsequent 3 to six months, simply because it has over the previous month:

Picture Supply: Zacks Funding Analysis

Shares within the backside tiers of industries can typically be intriguing quick candidates. Whereas particular person shares have the flexibility to outperform even after they’re a part of a lagging trade, the inclusion in a weaker group serves as a headwind for any potential rallies and the journey ahead is that rather more tough.

EXP shares have broadly underperformed the market over the previous yr. The shortage of participation within the newest bull market alerts warning forward.

Historical past of Earnings Misses & Deteriorating Outlook

Eagle Supplies missed the earnings mark in three of the previous 4 quarters. In its newest quarterly report, the corporate missed EPS estimates by 3% with flat general income. This triggered cuts to ahead steerage, contributing to fading earnings momentum and a decrease Zacks Rank.

Throughout the fiscal third quarter, earnings fell 10.3% from the year-ago interval, whereas the highest line additionally declined year-over-year. Persistently falling wanting projections is a recipe for underperformance, and EXP isn’t any exception.

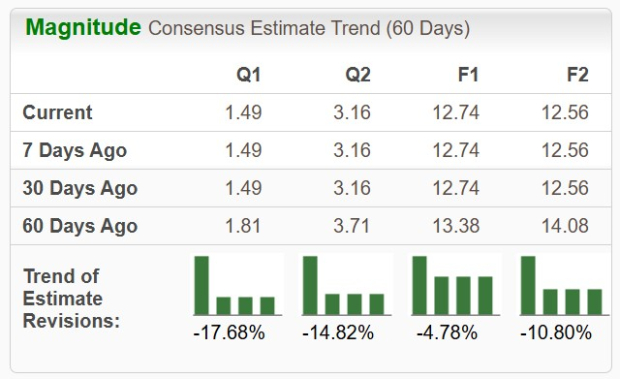

The development supplies provider has been on the receiving finish of unfavourable earnings estimate revisions as of late. Wanting into the fiscal fourth quarter, analysts reduce estimates by 17.68% prior to now 60 days. The Zacks Consensus EPS Estimate is now $1.49 per share, translating to a 28.4% decline relative to the identical interval within the prior yr. Revenues are anticipated to drop practically 2% in the course of the quarter to $461.6 million.

Picture Supply: Zacks Funding Analysis

Falling earnings estimates are an enormous purple flag and must be revered. Unfavorable development year-over-year is the kind of pattern that bears wish to see.

Technical Outlook

As illustrated under, EXP inventory is in a sustained downtrend. Discover how the inventory has been broadly underperforming the key indices. Additionally be aware that shares are buying and selling under downward-sloping 50-day (blue line) and 200-day (purple line) shifting averages – one other good signal for the bears.

Picture Supply: StockCharts

The shortage of shopping for stress is an indication that this inventory ought to be averted. Shares must make an outsized transfer to the upside and present growing earnings estimate revisions to warrant taking any lengthy positions. The inventory has fallen practically 16% prior to now six months alone.

Last Ideas

A deteriorating basic and technical backdrop present that this inventory is just not set to make its option to new highs anytime quickly. The truth that EXP inventory is included in one of many worst-performing trade teams provides one more headwind to a protracted checklist of issues.

A shaky earnings historical past and falling future earnings estimates will possible function a ceiling to any potential rallies, nurturing the inventory’s downtrend.

Potential buyers might need to give this inventory the chilly shoulder, or maybe embody it as a part of a brief or hedge technique. Bulls will need to avoid EXP till the scenario reveals main indicators of enchancment.

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t more likely to hold delivering the largest earnings. Little-known AI corporations tackling the world’s greatest issues could also be extra profitable within the coming months and years.

Eagle Supplies Inc (EXP) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.