")

AECOM ACM not too long ago raised full yr earnings steerage because it enjoys a document backlog. This Zacks #1 Rank (Robust Purchase) is predicted to develop earnings by the double digits in fiscal 2026 and 2027.

AECOM is a world infrastructure chief. It solves shoppers’ advanced challenges in water, setting, power, transportation, and buildings. AECOM companions with public- and private-sector shoppers to create revolutionary and resilient options all through the mission lifecycle, from advisory, planning, design and engineering to program and building administration.

AECOM Missed within the Fiscal First Quarter 2026

On Feb 9, 2026, AECOM reported its fiscal first quarter 2026 outcomes and missed on the Zacks Consensus for the primary time in seven quarters. The corporate reported $1.29 versus the Zacks Consensus of $1.41.

That was a miss of $0.12.

Nevertheless, the backlog rose by 9%, to a document highlighted by among the largest and most iconic tasks on this planet.

A few of these tasks embody AECOM’s choice as a most well-liked bidder on Scottish Water’s new multi-billion-dollar funding program to its choice as Supply Accomplice to the Video games Impartial Infrastructure and Coordination Authority for the Brisbane 2032 Olympic and Paralympic Video games.

It has a 1.5x book-to-burn ratio.

AECOM Raised Steering for Fiscal 2026

The corporate had outperformance within the design enterprise within the first quarter, a decrease than beforehand anticipated tax charge, and a document backlog and pipeline throughout the enterprise. It feels assured in its long-term outlook.

It raised its full yr earnings outlook to a variety of $5.85 and $6.05, in comparison with its prior steerage of $5.65 to $5.85.

This steerage was above the Zacks Consensus. Because of this, the analysts have raised their earnings estimates.

Three estimates have been raised within the final week, which has bumped the Zacks Consensus as much as $5.98 from $5.65. That’s earnings development of 13.7% as the corporate made simply $5.26 final yr.

Two estimates have been additionally revised larger for fiscal 2027 within the final week as effectively. The 2027 Zacks Consensus has jumped to $6.59 from $6.18. That’s one other 10.2% earnings development.

Right here’s what it appears like on the worth and consensus chart.

Picture Supply: Zacks Funding Analysis

AECOM is Holding onto Development Administration

AECOM additionally accomplished the evaluation of strategic options for its Development Administration enterprise and has concluded that it’ll proceed to personal and function the enterprise.

It has a powerful backlog and pipeline and has labored on necessary tasks in its markets.

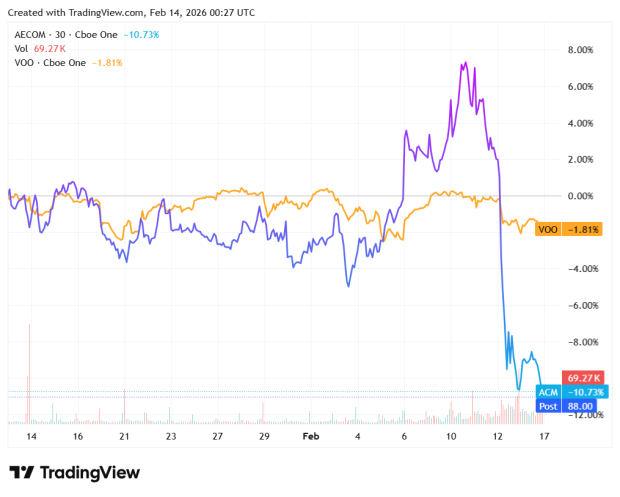

Shares of ACM Fall from Their Highs

AECOM shares have fallen within the final six months.

Picture Supply: Zacks Funding Analysis

The inventory is reasonable. It trades with a ahead price-to-earnings (P/E) ratio of 14.8. A P/E of 15 or below often signifies a inventory is a worth.

AECOM additionally has a price-to-sales (P/S) ratio of 0.7. A P/S ratio below 1.0 often signifies an organization is undervalued.

The corporate is shareholder pleasant. Within the fiscal first quarter, it returned greater than $340 million to shareholders via repurchases and dividends within the quarter. The dividend is yielding 1.4%.

After the primary quarter ended, the Board of Administrators permitted a rise within the share repurchase authorization to $1 billion.

For these buyers searching for an infrastructure firm with rising earnings that can be a worth, they may need to maintain AECOM on their brief record.

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t prone to maintain delivering the most important earnings. Little-known AI companies tackling the world’s greatest issues could also be extra profitable within the coming months and years.

AECOM (ACM) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.