Information is rising at an accelerated tempo, fueled by cloud adoption, AI, IoT and Huge Information. Conventional HDDs and SSDs proceed to serve enterprises and customers, whereas superior DRAM, NAND and HBM options energy cutting-edge purposes like AI coaching and hyperscale knowledge facilities. Two main U.S. gamers dominating discussions on this area are Western Digital Company (WDC) and Micron Expertise (MU). Each function within the storage and reminiscence segments, with their distinctive methods, market exposures and buyback packages.

Western Digital is a various storage firm providing a broad portfolio of merchandise, from conventional HDDs to NAND-based SSDs, catering to each shopper and enterprise markets. Idaho-based Micron is a number one world supplier of semiconductor reminiscence options, manufacturing high-performance DRAM, NAND, NOR, 3D XPoint and different reminiscence applied sciences underneath manufacturers like Micron, Essential and Ballistix, to be used in computing, shopper, networking and cellular merchandise.

Per a report by Priority Analysis, the worldwide semiconductor reminiscence market is projected to achieve round $215.36 billion by 2034, at a CAGR of 6.92% from 2025 to 2034. Additional, the worldwide knowledge storage market is projected to develop from $250.8 billion in 2025 to $483.9 billion by 2030 at a CAGR of 14% as acknowledged by Mordor Intelligence. Each WDC and MU are well-positioned to learn from these rising tendencies, attracting renewed investor curiosity. Nevertheless, if traders should select between the 2, which inventory ought to they contemplate based mostly on fundamentals, valuations, development potential and dangers?

Let’s discover this intimately.

The Case for WDC

Western Digital is a key participant within the world knowledge infrastructure area, capturing a serious chunk of the HDD market. It’s dedicated to innovation, advancing HDD know-how to supply drives with better capability, enhanced efficiency, improved vitality effectivity and the bottom complete value of possession. One of many firm’s key strategic strikes in 2025 was spinning off its flash reminiscence enterprise, SanDisk, to streamline operations and probably unlock shareholder worth.

Going forward, WDC anticipates that the rise of generative AI will drive gadget refresh cycles and increase content material development throughout smartphones, gaming, PCs and shopper units. As AI adoption jumped from 33% in 2023 to 65% in 2024, storage demand is rising for each HDDs and Flash on the edge and core. HBM is more and more essential for AI servers, whereas NAND flash powers quick and environment friendly SSDs for textual content, photographs and video.

Agentic AI purposes are additional accelerating unstructured knowledge era, creating new storage wants. Whereas eSSDs are favored for velocity and reliability, HDDs stay the cost-effective spine for large-scale knowledge storage, supporting world infrastructure. The corporate is already utilizing AI to spice up product improvement, whereas industry-wide adoption is producing knowledge at unprecedented ranges.

The corporate has considerably improved its profitability by specializing in higher-capacity drives and disciplined value administration. These efforts are boosting effectivity, margins and capability for reinvestment. Administration stays targeted on enhancing shareholder worth by way of dividends and buybacks. Backed by sturdy money move and a strong steadiness sheet, the board approved as much as $2 billion in share repurchases and initiated a quarterly dividend. Within the fiscal fourth quarter, the corporate repurchased about 2.8 million shares for $149 million.

Picture Supply: Zacks Funding Analysis

Nevertheless, one of many greatest challenges for WDC has been its excessive debt load. The excessive debt stage jeopardizes its means to pursue accretive acquisitions and different development endeavors. It’s required to generate sufficient money flows to satisfy debt necessities always. As of June 27, 2025, money and money equivalents totaled $2.1 billion, whereas long-term debt (together with the present portion) amounted to $4.7 billion.

Nonetheless, it diminished debt by $2.6 billion within the June quarter by way of money utilization and a debt-for-equity alternate, strengthening its steadiness sheet and reaching its internet leverage goal of 1–1.5x. Throughout the quarter, WDC exchanged about 21 million SanDisk shares to cut back Time period Mortgage A by $800 million whereas retaining 7.5 million shares. The corporate additionally redeemed $1.8 billion of senior unsecured notes, lowering gross debt to $4.7 billion at fiscal 2025 year-end.

The Case for MU

Micron is capitalizing on the quickly rising AI-driven reminiscence and storage markets, with improved stock throughout a number of finish markets supporting top-line development. Robust demand for its HBM merchandise has been encouraging. For MU, AI will not be solely driving demand but in addition boosting productiveness throughout the corporate, from product design and know-how improvement to manufacturing.

Its adoption has led to a 30–40% productiveness uplift in areas like code era. In design, AI accelerates the silicon-to-systems cycle, whereas in manufacturing, it has elevated wafer picture evaluation fivefold and doubled helpful knowledge assortment, enhancing yield efficiency. These capabilities assist Micron obtain larger product high quality, quicker time-to-market and stronger total monetary and aggressive efficiency.

Information middle server demand in 2025 is now anticipated to rise about 10%, larger than MU’s earlier forecasts of mid-single-digit development. Conventional server demand, which was beforehand flat, is projected to develop within the mid-single-digit vary, supported by rising enterprise workloads and the rising use of AI brokers. Alongside sturdy momentum in AI servers, this mixed development in conventional and AI servers is fueling sturdy demand for DRAM merchandise.

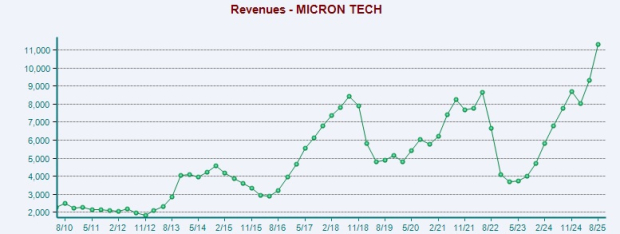

Micron’s knowledge middle enterprise has turn into a serious development driver, contributing 56% of complete income in fiscal 2025 with sturdy 52% margins. The HBM section continues to publish constant development, with fiscal fourth quarter income reaching practically $2 billion, reflecting an annualized run price of about $8 billion fueled by HBM3E adoption. Trying forward, Micron expects its HBM market share to proceed rising, aligning with its broader DRAM share targets.

Picture Supply: Zacks Funding Analysis

AI-driven workloads like cache tiering and database indexing are boosting demand for high-performance NAND SSDs, whereas AI server growth is rising the necessity for large-capacity storage. Micron is strengthening its place with customer-focused execution, superior know-how and the launch of its G9 NAND merchandise, together with the primary PCIe Gen6 SSDs. Within the close to time period, MU expects HDD provide shortages to additional help NAND demand and create a extra balanced market atmosphere.

Micron has a powerful cash-flow producing means, which allows it to enhance its money steadiness and decrease debt. Within the final reported quarter, MU lowered its debt by $900 million, together with a $700 million time period mortgage reimbursement and the repurchase of about $200 million in senior notes. The quarter closed with $14.6 billion in complete debt and $11.9 billion of money and investments, supported by low internet leverage and a weighted-average maturity extending to 2033.

Nevertheless, MU faces powerful competitors within the reminiscence market, with rival capability expansions probably affecting DRAM and NAND pricing. Commerce tensions may additionally push Chinese language corporations towards non-U.S. suppliers like Samsung. Whereas acquisitions increase income alternatives and product combine, additionally they introduce integration dangers and should divert consideration from natural development. Moreover, a better NAND combine, falling reminiscence costs and restricted value declines are more likely to weigh on margins.

Worth Efficiency and Valuation for MU & WDC

Over the previous yr, MU and WDC have registered positive aspects of 51.6% and 56.5%, respectively.

Picture Supply: Zacks Funding Analysis

MU appears to be like extra engaging than WDC from a valuation standpoint. Going by the value/earnings ratio, MU’s shares at the moment commerce at 9.4 ahead earnings, decrease than 15.87 for WDC.

Picture Supply: Zacks Funding Analysis

How Do Zacks Estimates Examine for MU & WDC?

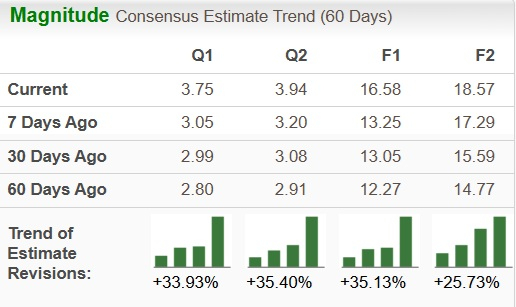

The Zacks Consensus Estimate for MU’s earnings for fiscal 2026 has been revised north 35% to $16.58 over the previous 60 days.

Picture Supply: Zacks Funding Analysis

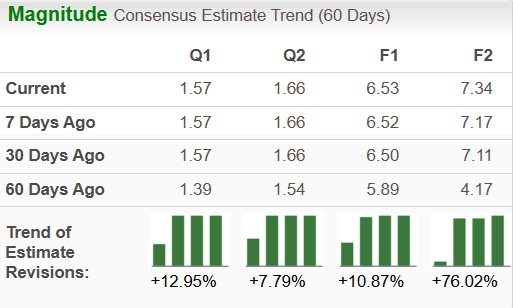

The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been revised up 10.9% to $6.53 over the previous 60 days.

Picture Supply: Zacks Funding Analysis

MU or WDC: Which is a Higher Choose?

Each WDC and MU are poised to capitalize on the rising knowledge storage {industry}, capturing development throughout a number of end-markets, from AI to enterprise to shopper storage.

MU at current sports activities a Zacks Rank #1 (Robust Purchase), whereas WDC has a Zacks Rank #3 (Maintain). Consequently, by way of Zacks Rank and valuation, MU appears to be a greater decide for the time being. You possibly can see the whole record of at this time’s Zacks #1 Rank shares right here.

5 Shares Set to Double

Every was handpicked by a Zacks skilled as the favourite inventory to realize +100% or extra within the months forward. They embrace

Inventory #1: A Disruptive Pressure with Notable Progress and Resilience

Inventory #2: Bullish Indicators Signaling to Purchase the Dip

Inventory #3: One of many Most Compelling Investments within the Market

Inventory #4: Chief In a Crimson-Scorching Trade Poised for Progress

Inventory #5: Fashionable Omni-Channel Platform Coiled to Spring

Many of the shares on this report are flying underneath Wall Avenue radar, which offers an awesome alternative to get in on the bottom flooring. Whereas not all picks will be winners, earlier suggestions have soared +171%, +209% and +232%.

Obtain Atomic Alternative: Nuclear Power’s Comeback free at this time.

Western Digital Company (WDC) : Free Inventory Evaluation Report

Micron Expertise, Inc. (MU) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.