A giant chunk of the S&P 500 has already reported 2025 This autumn outcomes, although the reporting docket stays stacked for weeks to come back. We’ve already heard from six of the Magnificent Seven members, with NVIDIA NVDA the one one but to report from the beloved group.

A peer to NVIDIA, particularly Superior Micro Units AMD, has already delivered its outcomes, with the inventory going through stress post-earnings. AMD shares have lagged relative to NVDA over the previous three months by a reasonably vast margin, as proven within the chart under.

Picture Supply: Zacks Funding Analysis

Have been AMD’s outcomes unhealthy, or was it extra a mirrored image of profit-taking after an enormous run over the previous 12 months? And what can traders count on from NVIDIA earnings? Let’s take a more in-depth have a look at the outcomes from AMD and expectations for NVDA.

AMD Earnings

AMD’s outcomes had been optimistic throughout the board, breaking information throughout many key metrics. This autumn income grew by 34% year-over-year to a file $10.3 billion, and importantly, Information Heart income of $5.4 billion additionally reached a brand new all-time excessive. Each metrics clearly paint a powerful demand image for the corporate, underpinned by the broader AI frenzy that gained’t be slowing anytime quickly.

Beneath is a chart illustrating AMD’s Information Heart gross sales on a quarterly foundation.

Picture Supply: Zacks Funding Analysis

The general income acceleration over latest intervals will be seen under. Please word that the chart under doesn’t present precise gross sales figures however slightly the YoY progress charges.

Picture Supply: Zacks Funding Analysis

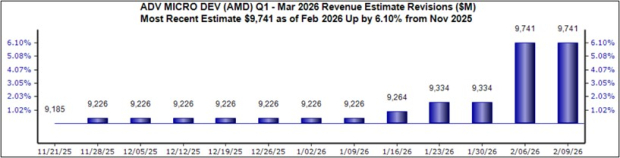

Gross sales acceleration is a key think about share outperformance, notably so for shares concerned within the AI commerce. The gross sales acceleration paired with favorable gross sales revisions for its upcoming interval (2026 Q1) displays a notably bullish pairing, with the $9.7 billion anticipated within the subsequent launch suggesting a 32% YoY progress fee.

As proven under, the gross sales estimate has been revised 6% increased since roughly mid-November of 2025, with the most important revisions occurring extra lately.

Picture Supply: Zacks Funding Analysis

The corporate’s EPS outlook for the upcoming launch (2026 Q1) can be bullish, with the present $1.27 Zacks Consensus EPS estimate up 7% since mid-November and suggesting 33% YoY progress. The outlook for shares continues to stay shiny, with the latest weak spot in shares post-earnings additionally giving shares a pleasant, wholesome breather after an enormous run.

The valuation image right here isn’t overly wealthy, both, relative to its historical past, with the present 31.0X ahead 12-month earnings a number of nicely off the 38.0X five-year median. The present a number of displays a 34% premium to the S&P 500, reflecting traders’ above-average progress expectations however stays nicely under the 77% five-year median premium.

NVIDIA Earnings Expectations

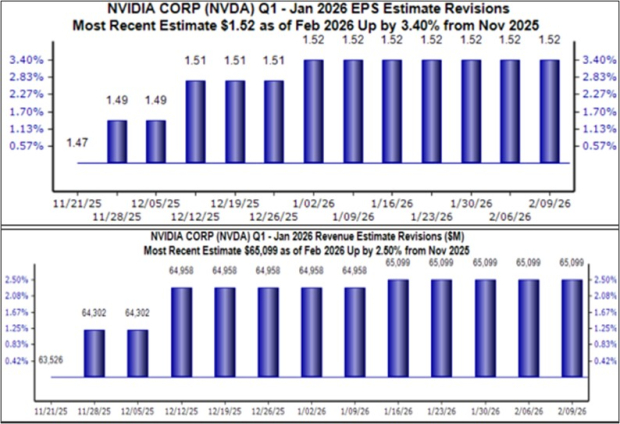

NVIDIA is all the time a ‘late reporter’ within the earnings cycle, with its outcomes coming nicely after lots of the notable tech gamers. EPS and gross sales revisions for the upcoming launch, anticipated on Feb. 25th after the shut, have remained each secure and bullish since mid-November, up by 3.4% and a couple of.5%, respectively.

Whereas no upward revisions have occurred for the reason that starting of the brand new 12 months, the soundness here’s a massive optimistic. Beneath is a chart illustrating how the EPS and gross sales revisions tendencies have developed over latest months.

Picture Supply: Zacks Funding Analysis

Regarding the Information Heart, undoubtedly crucial metric for NVIDIA these days, the Zacks Consensus estimate stands at $58.7 billion, suggesting a 65% YoY progress fee. Take into account that NVDA has repeatedly exceeded our consensus estimate over latest intervals, penciling in 5 beats during the last six quarters.

Beneath is a chart illustrating NVDA’s information heart gross sales on a quarterly foundation, with our consensus $58.7 billion estimate additionally blended in.

Picture Supply: Zacks Funding Analysis

Shares aren’t wealthy by any stretch regardless of the large run, with the present 25.8X ahead 12-month earnings a number of practically half of the 41.3X five-year median whereas reflecting only a 12% premium relative to the S&P 500. Take into account that shares traded nicely above present valuation ranges in 2021 and 2022, when the AI theme had not but been absolutely acknowledged by the market.

Picture Supply: Zacks Funding Analysis

Placing All the pieces Collectively

Each shares replicate nice choices for these in search of AI publicity, although it’s simple that NVIDIA NVDA stays the chief of the pair, underpinned by CUDA, its software program platform that has let builders use GPUs for normal computing, not simply graphics. It was launched method again in 2006, offering an enormous head begin.

Superior Micro Units AMD stays a powerhouse in its personal proper, however it continues to path NVIDIA, notably in market penetration. NVIDIA at the moment ranks as a Zacks Rank #2 (Purchase), whereas Superior Micro Units is at the moment a Zacks Rank #3 (Maintain).

Simply Launched: Zacks High 10 Shares for 2026

Hurry – you’ll be able to nonetheless get in early on our 10 high tickers for 2026. Handpicked by Zacks Director of Analysis Sheraz Mian, this portfolio has been stunningly and constantly profitable.

From inception in 2012 via November, 2025, the Zacks High 10 Shares gained +2,530.8%, greater than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed via 4,400 corporations lined by the Zacks Rank and handpicked one of the best 10 to purchase and maintain in 2026. You may nonetheless be among the many first to see these just-released shares with huge potential.

Superior Micro Units, Inc. (AMD) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.