")

Eagle Supplies Inc. EXP builds heavy development merchandise and light-weight constructing supplies which are vital for each street development in addition to business and residential development.

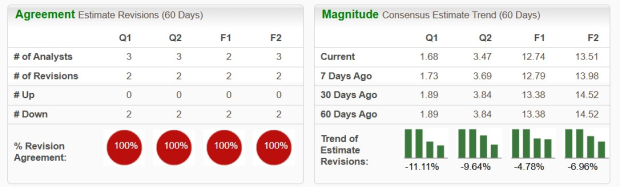

Eagle Supplies’ earnings outlook light once more after it reported its Q3 fiscal 2026 outcomes on January 29, touchdown EXP a Zacks Rank #5 (Robust Promote). The corporate’s current downward revisions are a part of a long-term damaging earnings revision development over the previous year-plus.

Ought to Buyers Keep Away from EXP Proper Now?

Eagle Supplies is a number one U.S. producer of heavy development merchandise and light-weight constructing supplies. The Dallas, Texas-headquartered firm primarily makes Portland Cement, which is vital for constructing roads and highways. It additionally makes Gypsum Wallboard that is a significant cog in residential, business, and industrial development.

Eagle Supplies has posted spectacular progress during the last roughly 15 years, and its long-term upside stays sturdy. It’s going through some near-term headwinds which are negatively impacting its earnings. On high of that, its gross sales progress is slowing a bit after an enormous run, weighed down by a ‘difficult’ residential development market.

Picture Supply: Zacks Funding Analysis

EXP’s This autumn FY26 earnings estimate has dropped 11% since its late January earnings launch. Its FY26 estimate is down 5% as properly, with its 2027 outlook 7% decrease. These current downward revisions land the inventory its Zacks Rank #5 (Robust Promote) proper now.

The development merchandise big’s current damaging revisions lengthen its long-term downward development. This backdrop may imply that traders wish to keep away from Eagle Supplies within the brief time period till it supplies upbeat bottom-line steering.

Picture Supply: Zacks Funding Analysis

Lengthy-term, nevertheless, Eagle Supplies stays a inventory to observe given its publicity to upside throughout the U.S. infrastructure growth and extra. And the U.S. housing market is prone to bounce again sooner or later.

Its CEO touched on that in his Q3 earnings feedback, noting that “federal, state, and native spending on public infrastructure tasks and personal non-residential development remained elevated, supporting sturdy demand for our Heavy development merchandise.”

Zacks Names #1 Semiconductor Inventory

This under-the-radar firm makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is uniquely positioned to reap the benefits of the subsequent progress stage of this market. And it is simply starting to enter the highlight, which is precisely the place you wish to be.

With sturdy earnings progress and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. World semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $971 billion by 2028.

See This Inventory Now for Free >>

Eagle Supplies Inc (EXP) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.