Inventory Hits 52-Week Highs: Purchase Sign?")

Amgen (AMGN) is having a second. The biotech bellwether is buying and selling close to contemporary 52-week highs, up roughly 8% within the newest session, and the tape is sending a transparent message: establishments are leaning in. When a mega-cap healthcare identify breaks out whereas the broader market debates development versus defensives, buyers ought to listen. The numbers inform a compelling story.

At yesterday afternoon’s earnings report, Amgen reported strong development within the fourth quarter and full yr 2025, with whole revenues rising roughly 9% in This autumn to about $9.9 billion and 10% for the complete yr to roughly $36.8 billion, pushed by quantity beneficial properties throughout its diversified product portfolio.

Zooming out, AMGN has quietly put collectively a robust run: up about 13.7% over the past three months and roughly 11% year-to-date. That is regular accumulation in a $193 billion chief with a deep industrial portfolio and a pipeline that’s beginning to get extra credit score. The important thing query is whether or not this transfer is only a “protected haven” bid, or the beginning of a better valuation regime pushed by earnings energy and catalysts.

Picture Supply: Zacks Funding Analysis

Amgen Inventory Breakout: Why It Issues

A 52-week excessive is greater than a headline, it’s a sign. New highs have a tendency to draw momentum capital, pressure underweight managers to chase, and create a self-reinforcing setup as technical patrons step in. For AMGN inventory, the breakout can be occurring with basic backing: income development is operating at 10%, which is a notable tempo for a mature biopharma franchise.

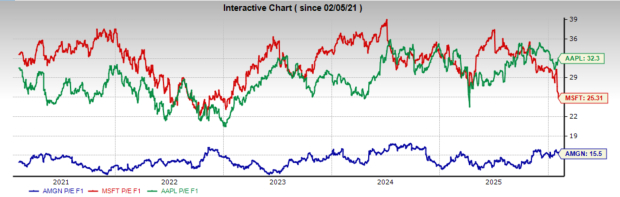

Picture Supply: TradingView

AMGN’s sturdiness comes from a broad portfolio of cash-generating therapies throughout irritation, oncology, bone well being, and uncommon illness. Merchandise like Enbrel, Otezla, Prolia/XGEVA, Repatha, and KYPROLIS anchor the bottom, whereas newer and partnered property add incremental development vectors. That breadth issues in 2026’s market, the place single-product tales routinely get rerated on one trial readout.

Simply as vital, the breakout is occurring with out “story inventory” valuation extra. AMGN trades round 25.2x trailing earnings, however the ahead P/E of 15.6x is the quantity that jumps off the display screen. That a number of is just not pricing in blue-sky outcomes. And when a inventory pushes to highs on an inexpensive ahead a number of, it usually signifies the market is beginning to consider the ahead earnings path is sturdier than beforehand assumed.

AMGN Share Valuation: Earnings Energy Appears Underpriced

Trying on the fundamentals, AMGN’s earnings profile stays the spine of the bull case. Present-year EPS is about $22.33, with next-year EPS anticipated close to $22.92. That’s not a “hypergrowth” curve, however in large-cap pharma, consistency is the characteristic. A inventory doesn’t want explosive EPS development to outperform if the market is underestimating sturdiness, margin resilience, or the contribution from new launches.

Consensus expects continued execution from Amgen’s diversified lineup, and the valuation suggests skepticism stays. Put in another way: the market is paying a mid-teens ahead a number of for an organization delivering double-digit income development. That mismatch is precisely what tends to point out up in breakout charts.

Wall Road’s worth goal tape additionally displays enhancing sentiment. Latest goal strikes embrace RBC lifting its goal to $360 (Outperform) and Goldman Sachs reiterating a Purchase whereas elevating its goal to $415. Cantor Fitzgerald moved its goal to $350 whereas staying Impartial—an vital element as a result of even the extra cautious companies have been compelled to elevate numbers because the inventory grinds increased. Whisper numbers recommend the subsequent leg increased comes from proof that newer property and the pipeline are translating into sturdy, multi-year income streams.

Amgen Catalysts and What’s Subsequent for the Inventory

For buyers chasing a 52-week excessive, the proper transfer is to not stare on the chart, however to outline the catalysts that hold the bid underneath the inventory.

Key catalysts forward embrace continued portfolio growth and pipeline progress. Amgen has been lively in constructing a broader development engine past legacy blockbusters, and the market tends to reward giant biopharma when it proves it may refresh the franchise with out sacrificing profitability. The pipeline is the optionality, however industrial execution is the money register.

The phase/metric that’s the quantity to look at is ahead EPS development versus the present valuation. If AMGN can hold next-year EPS expectations agency (or nudging increased) whereas sustaining its double-digit income development trajectory, the market has room to re-rate the a number of. That’s how a “defensive” turns into a “defensive development” compounder—and people are scarce.

One other underappreciated catalyst: relative attractiveness versus mega-cap tech shares. Apple (AAPL) trades round 32.1x earnings, and Microsoft (MSFT) trades close to 24.3x. Each are elite companies, however their valuations already replicate premium expectations. Against this, AMGN inventory at a 15.6x ahead P/E gives a special danger/reward profile, much less depending on a number of growth and extra tied to execution and money technology. In a market the place charges and danger urge for food can change rapidly, that valuation hole issues.

Picture Supply: Zacks Funding Analysis

What AMGN Inventory’s New Excessive Says

AMGN inventory hitting 52-week highs is a bullish inform, and it’s supported by fundamentals, not hype. A near-$360 worth with sturdy current momentum, ~10% income development, and a ahead P/E round 15.6x creates a setup the place buyers get high quality, scale, and catalysts with out paying a tech-style premium. The numbers inform a compelling story.

The clear takeaway for buyers: deal with the breakout as affirmation that Amgen could also be again in management mode. With cheap valuation, enhancing sentiment, and a number of basic levers, AMGN seems positioned to stay a core large-cap healthcare winner, whilst Apple and Microsoft and different huge tech/AI names proceed to dominate the dialog.

Free Report: Benefiting from the 2nd Wave of AI Explosion

The subsequent section of the AI explosion is poised to create vital wealth for buyers, particularly those that get in early. It should add actually trillion of {dollars} to the financial system and revolutionize almost each a part of our lives.

Traders who purchased shares like Nvidia on the proper time have had a shot at big beneficial properties.

However the rocket journey within the “first wave” of AI shares might quickly come to an finish. The sharp upward trajectory of those shares will start to degree off, leaving exponential development to a brand new wave of cutting-edge firms.

Zacks’ AI Increase 2.0: The Second Wave report reveals 4 under-the-radar firms which will quickly be shining stars of AI’s subsequent leap ahead.

Entry AI Increase 2.0 now, completely free >>

Apple Inc. (AAPL) : Free Inventory Evaluation Report

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Amgen Inc. (AMGN) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.