")

BellRing Manufacturers supplies vitamin merchandise in america. The corporate gives ready-to-drink protein shakes and drinks, protein powders, vitamin bars, and different merchandise primarily beneath the Premier Protein and Dymatize manufacturers.

Key challenges stay for BellRing in 2026 together with adjustments in buyer buying conduct and a scarcity of pricing energy. Weak consumption development stays the most important unanswered query within the broader shopper staples sector. A troublesome macroeconomic setting and lingering inflationary situations don’t bode properly for the corporate’s outlook.

As we’ll see, earnings are anticipated to say no within the present fiscal 12 months. BellRing faces intense competitors as shoppers stay centered on well being and navigate towards dietary dietary supplements.

The Zacks Rundown

A Zacks Rank #5 (Sturdy Promote) inventory, BellRing Manufacturers BRBR is a element of the Zacks Meals – Miscellaneous business group, which at the moment ranks within the backside 14% out of roughly 250 Zacks Ranked Industries. As such, we anticipate this business group as an entire to underperform the market over the subsequent 3 to six months, simply because it has all through the previous 12 months:

Picture Supply: Zacks Funding Analysis

Shares within the backside tiers of industries can typically be intriguing quick candidates. Whereas particular person shares have the power to outperform even once they’re a part of a lagging business, the inclusion in a weaker group serves as a headwind for any potential rallies and the journey ahead is that rather more troublesome.

Shares on this business are anticipated to expertise beneath common earnings development, so it’s no shock that BRBR shares have been underperforming the market over the previous 12 months. The inventory hit a 52-week low earlier in January at the same time as the main U.S. indexes hover close to all-time highs.

Current Earnings Miss & Deteriorating Outlook

Again in November, BellRing broke an extended streak of earnings beats after the corporate posted third-quarter earnings of 51 cents per share, lacking the Zacks Consensus Estimate by almost 6%. Falling in need of earnings estimates is a recipe for underperformance, and BRBR is not any exception.

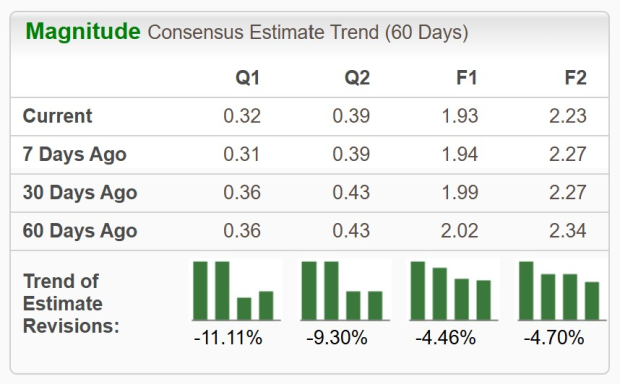

The dietary product supplier has been on the receiving finish of destructive earnings estimate revisions as of late. Trying on the newest quarter, analysts slashed estimates by -11.11% up to now 60 days. The This autumn Zacks Consensus EPS Estimate is now 32 cents per share, reflecting destructive development of -44.8% relative to the identical interval within the prior 12 months.

Picture Supply: Zacks Funding Analysis

Falling earnings estimates are an enormous purple flag and have to be revered. Unfavourable development year-over-year is the kind of pattern that bears prefer to see.

Technical Outlook

As illustrated beneath, BRBR inventory is in a sustained downtrend. Discover how the inventory has been extensively underperforming the main indices. Additionally notice that shares are buying and selling beneath downward-sloping 50-day (blue line) and 200-day (purple line) transferring averages – one other good signal for the bears.

Picture Supply: StockCharts

BRBR inventory has skilled what is called a “loss of life cross,” whereby the inventory’s 50-day transferring common crosses beneath its 200-day transferring common. Shares must make an outsized transfer to the upside and present growing earnings estimate revisions to warrant taking any lengthy positions. The inventory has fallen greater than 60% up to now 9 months alone.

Last Ideas

A deteriorating basic and technical backdrop present that this inventory isn’t set to make its technique to new highs anytime quickly. The truth that BRBR inventory is included in one of many worst-performing business teams provides yet one more headwind to an extended record of issues.

A current earnings miss and falling future earnings estimates will seemingly function a ceiling to any potential rallies, nurturing the inventory’s downtrend.

Potential buyers could need to give this inventory the chilly shoulder, or maybe embody it as a part of a brief or hedge technique. Bulls will need to avoid BRBR till the scenario reveals main indicators of enchancment.

Zacks’ Analysis Chief Picks Inventory Most Prone to “At Least Double”

Our specialists have revealed their Prime 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. In fact, all our picks aren’t winners however this one might far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our Prime Inventory to Double (Plus 4 Runners Up) >>

BellRing Manufacturers Inc. (BRBR) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.