BHP Group Restricted BHP and Vale S.A. VALE are among the many world’s largest iron ore producers and diversified miners, making them opponents within the world metals and mining sector. Each corporations are positioned to learn as infrastructure funding picks up worldwide and long-term demand grows for metal, copper, lithium, nickel and different minerals important for clear vitality applied sciences.

BHP has a market capitalization of $165 billion, whereas VALE has a market capitalization of $66 billion.

For traders on this house, let’s analyze which inventory is best positioned for upside, BHP or Vale. A more in-depth take a look at their fundamentals, progress drivers and key dangers can provide readability.

The Case for BHP

BHP produced a file 263 Mt of iron ore in fiscal 2025, inside its guided 255-265.5 Mt and up 1% yr over yr. Manufacturing at Western Australia Iron Ore (WAIO) was a file of 257 Mt (290 Mt on a 100% foundation). WAIO has been the lowest-cost iron ore producer globally for greater than 4 years.

The upside continued within the first half of fiscal 2026 with iron ore manufacturing rising 2% yr over yr to 134 Mt. WAIO reported a file first half manufacturing of 130 Mt, aided by robust supply-chain efficiency.

For fiscal 2026, BHP continues to count on iron ore manufacturing of 258-269 Mt. WAIO’s output is more likely to be 251-262 Mt (284-296 Mt on a 100% foundation). This components within the deliberate renewal of Automotive Dumper 3 (CD3) and the continuing tie-in actions for Rail Expertise Program 1 (RTP1).

BHP continues to reshape its portfolio towards commodities resembling copper and potash, allocating practically 70% of its medium-term capital expenditure to those areas. This technique positions the corporate to learn from decarbonization, electrification, inhabitants progress and rising residing requirements in rising markets.

Copper manufacturing reached a file 2,017 kt in fiscal 2025, the primary time BHP crossed the two,000-kt milestone. Output has risen 28% over the previous three years, reflecting sustained funding.

Within the first half of fiscal 2026, copper manufacturing remained fixed yr over yr at 984 kt. BHP elevated its fiscal 2026 copper output steerage to between 1,900 and a pair of,000 kt from prior acknowledged 1,800-2,000 kt.

BHP can also be advancing the Jansen Stage 1 potash mission, a large-scale, low-cost, high-grade useful resource with a mine life exceeding 100 years. It has been 75% accomplished and BHP is working towards its first manufacturing by mid-2027. As soon as operational, Jansen Stage 1 is anticipated to supply 4.15 million tons of potash yearly. Stage 2 of the mission has been 14% accomplished and is anticipated to ship its first manufacturing in fiscal 2031.

These investments will remodel Jansen into one of many world’s largest potash mines, doubling manufacturing capability to eight.5 million tons per yr, positioning BHP as a serious world producer of potash by the top of the last decade.

The Case for Vale

Vale lately acknowledged that iron ore manufacturing for 2025 was round 335 Mt, on the greater finish of its focused 325-335 Mt. Copper output was round 370 kt in 2025, additionally assembly the excessive finish of its focused 340-370 kt. Nickel output was reported at 175 kt in contrast with the corporate’s goal of 160-175 kt.

Vale can also be investing closely within the base metals enterprise to learn from the worldwide vitality transition. The corporate’s capex plans for the enterprise are $1.6 billion in 2026 and $2 billion from 2027 onward.

In 2026, Vale’s copper manufacturing is anticipated to be between 350 kt and 380 kt, and attain 420-500 kt as of 2030 and 700 kt by 2035. With these projections, Vale guarantees a 7% CAGR over 2024-2035 versus the 4% common for friends.

The Bacaba mission will lengthen the lifetime of the Sossego Mining Advanced, contributing a median annual copper output of fifty ktpy over an eight-year mine life. Manufacturing is anticipated to begin within the first half of 2028. Different tasks, resembling Salobo Coarse Particle Flotation (CPF), Alemão and Cristalino, will enhance Vale’s copper manufacturing capability.

Vale lately signed an settlement with Glencore Canada (Glencore) to collectively consider a possible brownfield copper improvement mission at their adjoining properties within the Sudbury Basin, with an anticipated start-up in 2030. Vale plans to hit 700 kt ranges by 2035, primarily by the accelerated improvement of property within the North and South hubs within the Carajás area.

For 2026, Vale expects its nickel manufacturing between 175 kt and 200 kt, reflecting replenishment tasks in Canada, publicity to Pomalaa and Morowali, and the start-up of the second furnace at Onça Puma. For 2030, nickel manufacturing is anticipated at 210-250 kt, with enter from tasks resembling Thompson Ultramafics, Sorowako HPAL, partnership tasks and offtake.

How do Estimates Examine for BHP & VALE?

The Zacks Consensus Estimate for BHP’s fiscal 2026 earnings signifies a year-over-year rise of 23.1%. The estimate for earnings for fiscal 2027 displays a 1.9% drop. Each the earnings estimates for fiscal 2026 and financial 2027 for BHP have moved up over the previous 60 days.

Picture Supply: Zacks Funding Analysis

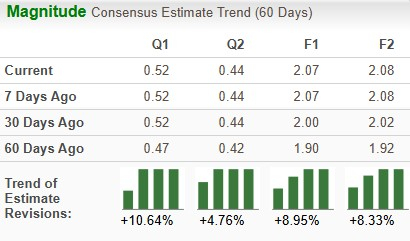

The Zacks Consensus Estimate for Vale’s 2025 earnings of $2.07 per share signifies year-over-year progress of 13.7%. The Zacks Consensus Estimate for Vale’s 2026 earnings is $2.08 per share, which tasks a 0.4% rise. Each the EPS estimates for Vale for fiscal 2025 and financial 2026 have been revised upward prior to now 60 days.

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

BHP Group & Vale: Worth Efficiency & Valuation

In a yr, BHP inventory has appreciated 36.7%, lagging Vale, which has gained 92.2%.

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

BHP is buying and selling at a ahead price-to-sales a number of of three.17X, whereas VALE’s ahead gross sales a number of sits at 1.63X.

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

BHP or VALE: Which is a Higher Choose?

BHP and Vale are each well-positioned for sturdy long-term progress, backed by resilient iron ore operations. A supportive commodity worth backdrop and rising earnings estimates additional assist the shares. Nonetheless, a beautiful valuation and a stronger one-year worth efficiency strengthen the funding case for Vale.

Traders looking for publicity to the iron mining house would possibly take into account VALE to be the extra favorable possibility right now.

Each VALE and BHP at present sport a Zacks Rank #1 (Robust Purchase). You possibly can see the entire checklist of immediately’s Zacks #1 Rank shares right here.

Zacks’ Analysis Chief Picks Inventory Most Prone to “At Least Double”

Our specialists have revealed their Prime 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. After all, all our picks aren’t winners however this one might far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our Prime Inventory to Double (Plus 4 Runners Up) >>

BHP Group Restricted Sponsored ADR (BHP) : Free Inventory Evaluation Report

VALE S.A. (VALE) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.