- AA’s Earnings Shock Historical past

- Earnings Whispers for AA

- Elements Driving Alcoa’s Efficiency

- AA Worth Efficiency

- Three-Month Worth Efficiency

- Alcoa’s Valuation Stays a Tailwind

- Worth-to-Earnings (Ahead 12 Months)

- Funding Thesis

- Ought to You Purchase AA Now?

- #1 Semiconductor Inventory to Purchase (Not NVDA)

Alcoa Company AA is scheduled to launch fourth-quarter 2025 outcomes on Jan. 22, after market shut. The Zacks Consensus Estimate for earnings is presently pegged at 95 cents per share on revenues of $3.24 billion.

Fourth-quarter earnings estimates have elevated 18.8% over the previous 60 days. Nevertheless, the bottom-line projection signifies a lower of 8.7% from the year-ago quantity. Additionally, the Zacks Consensus Estimate for quarterly revenues signifies a year-over-year decline of seven%.

AA’s Earnings Shock Historical past

Picture Supply: Zacks Funding Analysis

Alcoa has a powerful earnings shock historical past. The corporate’s earnings outpaced the Zacks Consensus Estimate in every of the trailing 4 quarters, the typical shock being 39.3%. Within the final reported quarter, it delivered an earnings shock of 86.7%.

Earnings Whispers for AA

Our confirmed mannequin predicts an earnings beat for the corporate this time round. The mixture of a constructive Earnings ESP and a Zacks Rank #1 (Sturdy Purchase), 2 (Purchase) or 3 (Maintain) will increase the chances of an earnings beat. You possibly can uncover the very best shares earlier than they’re reported with our Earnings ESP Filter.

Alcoa has an Earnings ESP of +0.53% because the Most Correct Estimate is pegged at 96 cents per share, larger than the Zacks Consensus Estimate of 95 cents. It sports activities a Zacks Rank of 1 at current. You possibly can see the whole checklist of right now’s Zacks #1 Rank shares right here.

Alcoa Worth and EPS Shock

Alcoa price-eps-surprise | Alcoa Quote

Elements Driving Alcoa’s Efficiency

A rise in demand for merchandise within the electrical and packaging finish markets in North America and Europe, is anticipated to have benefited Alcoa’s Aluminum phase within the fourth quarter. Additionally, continued progress on the San Ciprián and the restart of the Spain smelter are prone to have aided the phase’s gross sales. For the fourth quarter, the Zacks Consensus Estimate for the Aluminum phase’s whole gross sales is pegged at $2.45 billion, indicating a 29% rise from the year-ago reported quantity.

Alcoa’s Alumina phase is anticipated to have benefited from a rise in manufacturing on the Australian refineries and the rising recognition of its Sustana line of merchandise. Nevertheless, the phase’s outcomes are anticipated to place up a weak present attributable to decrease shipments of alumina arising from the curtailment of the Kwinana refinery and decreased buying and selling exercise. The consensus mark for the Alumina phase’s whole gross sales is pegged at $1.32 billion, indicating a 46% decline from the year-ago quantity.

Nonetheless, synergistic features from partnerships and acquisitions made by the corporate are anticipated to have boosted its efficiency. In March 2025, Alcoa and IGNIS EQT entered right into a three way partnership settlement to renew and enhance the manufacturing capability of its San Ciprian web site. In August 2024, Alcoa acquired Alumina Restricted. This acquisition bolstered its place as a pure-play and upstream aluminum firm worldwide.

Additionally, Alcoa’s efforts to extend smelter and refinery capability are prone to have supported its leads to the to-be-reported quarter.

Nevertheless, the escalating price of gross sales attributable to larger enter prices poses a risk to Alcoa’s backside line. Additionally, given the corporate’s in depth geographic presence, its operations are topic to world political dangers and overseas alternate headwinds. A stronger U.S. greenback is prone to have damage AA’s abroad enterprise within the to-be-reported quarter.

AA Worth Efficiency

Alcoa’s shares have surged 54.2% up to now three months in contrast with the Zacks Metallic Merchandise – Distribution business’s 49.9% development. The corporate’s shares have additionally fared higher than the S&P 500’s enhance of 4.2%. Its friends, Constellium SE CSTM and Ryerson Holding Corp. RYI have gained 38.9% and 24.9%, respectively, in the identical interval.

Three-Month Worth Efficiency

Picture Supply: Zacks Funding Analysis

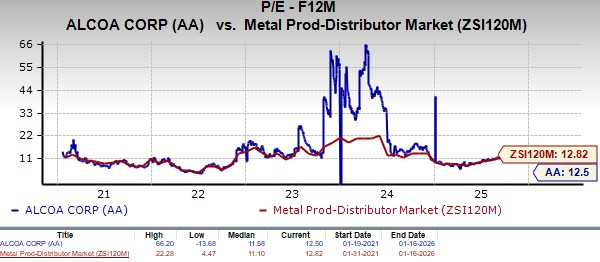

Alcoa’s Valuation Stays a Tailwind

AA’s valuation affords upside potential. The inventory is buying and selling at a ahead 12-month price-to-earnings (P/E) ratio of 12.50X, barely decrease than the business common of 12.82X.

Compared with Alcoa’s valuation, its friends, Constellium and Ryerson Holding, are buying and selling larger. Constellium and Ryerson Holding are buying and selling at 12.94X and 21.56X, respectively.

Worth-to-Earnings (Ahead 12 Months)

Picture Supply: Zacks Funding Analysis

Funding Thesis

With a complete and diversified product portfolio, Alcoa has been benefiting from the rising recognition of lighter and energy-efficient electrical autos, recycled aluminum and rechargeable batteries. The corporate’s strategic collaborations and energy within the electrical and packaging markets bode properly for its fourth-quarter earnings.

Its price noting that in June 2025, the U.S. administration elevated tariffs on imported aluminum to 50% as a measure to right commerce imbalances and enhance the home business. The transfer has elevated aluminum costs, thereby benefiting home producers like Alcoa which is prone to drive itss efficiency within the quarters forward.

Ought to You Purchase AA Now?

Strong momentum throughout finish markets, accretive acquisitions and synergistic features from partnerships place Alcoa favorably for robust fourth-quarter outcomes.

With a constructive analyst sentiment and sturdy development prospects, Alcoa is well-positioned to ship sustained development and shareholder worth. We imagine that AA inventory is a perfect candidate for an investor’s portfolio addition.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unimaginable demand for information is fueling the market’s subsequent digital gold rush. As information facilities proceed to be constructed and continually upgraded, the businesses that present the {hardware} for these behemoths will develop into the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to benefit from the subsequent development stage of this market. It focuses on semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is precisely the place you wish to be.

See This Inventory Now for Free >>

Alcoa (AA) : Free Inventory Evaluation Report

Constellium SE (CSTM) : Free Inventory Evaluation Report

Ryerson Holding Company (RYI) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.