December’s CPI report confirmed inflation is secure however not essentially bettering in the best way markets and the Federal Reserve could choose. Nonetheless, when excluding the risky classes of meals and power, core client costs rose on the slowest tempo since March 2021, with a 0.2% month-to-month uptick and a couple of.6% yearly enhance.

When together with all classes, CPI was up 0.3% during the last month and a couple of.7% yearly, with larger meals costs standing out particularly, registering a 0.7% month-to-month uptick and a 3.1% annual enhance. Though inflation has remained above the Fed’s most well-liked goal of two%, Core CPI cooled greater than most economists anticipated.

That mentioned, listed here are two shares which might be intriguing after December’s CPI report and one which will have to be averted for now.

Picture Supply: U.S. Bureau of Labor Statistics

Automobiles.com & Carvana May Profit from Decrease Used Automobile Costs

Though used vehicles and vehicles costs remained 1.6% larger during the last yr, they noticed the most important drop amongst all gadgets, excluding meals and power, with a 1.7% unadjusted month-to-month lower and a 1.1% month-to-month drop on a seasonally adjusted foundation. Contemplating this may occasionally draw extra patrons into the used automobile market, Automobiles.com CARS and Carvana CVNA may very well be beneficiaries as two of the most important on-line marketplaces for used vehicles within the U.S.

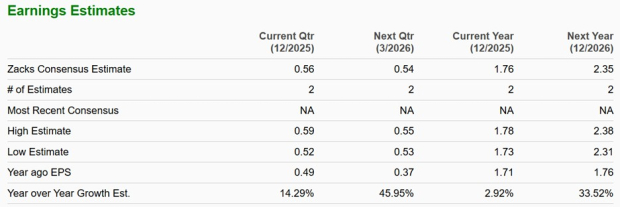

Automobiles.com’s inventory stands out with a sexy value of $12 a share and an inexpensive ahead earnings a number of of simply 5X. Beginning to make the case for being undervalued, Automobiles.com inventory presently lands a Zacks Rank #3 (Maintain).

Management adjustments and insider promoting have pressured Automobiles.com’s inventory, and whereas investor uncertainty stays excessive, CARS may very well be set for a pleasant rebound if the corporate begins to satisfy its intriguing EPS targets. To that time, Automobiles.com’s EPS is projected to leap one other 33% in fiscal 2026 to $2.35, but it surely has been susceptible to lacking quarterly earnings expectations, though the risk-to-reward is tempting.

*Automobiles.com might be reporting its This fall 2025 outcomes on Thursday, February 26th.

Picture Supply: Zacks Funding Analysis

Carvana, however, has been extra constant in hitting its lofty progress targets because the self-described “fastest-growing used automobile retailer.” Changing into one of many main platforms for purchasing and promoting vehicles, Carvana inventory has skyrocketed a thoughts boggling +6,000% within the final three years.

At over $450 a share and 64X ahead earnings, CVNA is much from low cost however has justified a premium with FY25 EPS now anticipated to come back in at $5.49, a 245% enhance from $1.59 in 2024. Moreover, FY26 EPS is projected to leap one other 33% to $7.31.

It’s additionally noteworthy that Carvana’s PEG ratio is close to 1X, with a mark at this stage or decrease, suggesting a inventory may very well be undervalued when contemplating its long-term progress charge because the denominator to the P/E ratio. CVNA lands a Zacks Rank #3 (Maintain) after hovering one other +30% within the final three months.

*Carvana is scheduled to report This fall 2025 outcomes on Wednesday, February 18th.

Picture Supply: Zacks Funding Analysis

December CPI Highlights Tyson Meals’ Struggles

Notably, meat, poultry, and fish costs have been up almost 7% YoY, attributed to a 16% uptick in beef and veal prices, which rose 1% month-to-month. Decrease livestock has the worth of floor beef edging towards $7 per pound, and better meals costs don’t mechanically translate into larger income for packaged-food firms or meat processors.

To that time, Tyson Meals TSN is a main instance because the meat producer has been grappling with deeper losses inside its beef phase on account of extreme cattle shortages and escalating enter prices. When cattle provides are tight, Tyson pays extra for livestock, however can’t absolutely move these prices to shoppers.

This will likely finally result in higher long-term shopping for alternatives as soon as Tyson strikes previous the meat scarcity, however TSN presently lands a Zacks Rank #4 (Promote) as EPS revisions may development decrease and are already modestly down during the last quarter for FY26 and FY27 EPS estimates have retracted once more within the final 60 days.

Picture Supply: Zacks Funding Analysis

Simply Launched: Zacks Prime 10 Shares for 2026

Hurry – you’ll be able to nonetheless get in early on our 10 prime tickers for 2026. Handpicked by Zacks Director of Analysis Sheraz Mian, this portfolio has been stunningly and persistently profitable.

From inception in 2012 via November, 2025, the Zacks Prime 10 Shares gained +2,530.8%, greater than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed via 4,400 firms lined by the Zacks Rank and handpicked the very best 10 to purchase and maintain in 2026. You’ll be able to nonetheless be among the many first to see these just-released shares with monumental potential.

Carvana Co. (CVNA) : Free Inventory Evaluation Report

Automobiles.com Inc. (CARS) : Free Inventory Evaluation Report

Tyson Meals, Inc. (TSN) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.