- AIZ’s Enticing Valuation

- AIZ Is an Outperformer

- AIZ’s Development Projection Encourages

- Optimistic Analyst Sentiment for AIZ

- Common Goal Worth for AIZ Suggests Upside

- Assurant’s Favorable Return on Capital

- Key Factors to Word for AIZ

- Wealth Distribution

- Closing Tackle AIZ

- Quantum Computing Shares Set To Soar

Shares of Assurant, Inc. AIZ closed at $240.85 on Wednesday, close to its 52-week excessive of $243.76. This proximity underscores investor confidence. It has the components for additional value appreciation.

The inventory is buying and selling above the 50-day and 200-day easy transferring averages (SMA) of $225.33 and $207.85, respectively, indicating strong upward momentum. The SMA is a extensively used technical evaluation device to foretell future value developments by analyzing historic value information.

Earnings of Assurant grew 16.6% within the final 5 years, higher than the trade common of 10.2%. Assurant has a strong historical past. The insurer has a strong observe file of beating earnings estimates in every of the final 4 quarters, with a median being 22.74%.

Picture Supply: Zacks Funding Analysis

AIZ’s Enticing Valuation

Assurant shares are buying and selling at a reduction in contrast with the Zacks Multi-line Insurance coverage trade. Its ahead price-to-book worth of two.11X is decrease than the trade common of two.71X, the Finance sector’s 4.3X and the Zacks S&P 500 Composite’s 8.5X. The insurer has a Worth Rating of A.

Shares of The Vacationers Firms, Inc. TRV and Cincinnati Monetary Company CINF are buying and selling at a a number of larger than the trade common, whereas NMI Holdings Inc NMIH shares are buying and selling at a reduction.

Picture Supply: Zacks Funding Analysis

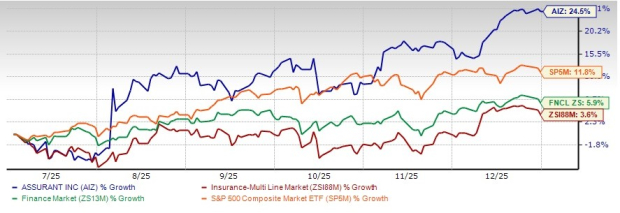

AIZ Is an Outperformer

Shares of Assurant have risen 24.5% within the final six-month interval, outperforming the trade’s progress of three.6%. In the identical timeframe, the Finance sector and the Zacks S&P 500 Index have elevated 5.9% and 11.8%, respectively.

Picture Supply: Zacks Funding Analysis

With a market capitalization of $12.15 billion, the typical quantity of shares traded within the final three months was 0.3 million.

AIZ’s Development Projection Encourages

The Zacks Consensus Estimate for Assurant’s 2025 earnings per share (EPS) signifies a year-over-year improve of 17%. The consensus estimate for revenues is pegged at $12.80 billion, implying a year-over-year enchancment of seven%.

The consensus estimate for 2026 EPS and revenues signifies a rise of 8.3% and 5.5%, respectively, from the corresponding 2025 estimates.

Optimistic Analyst Sentiment for AIZ

Two of the 5 analysts masking the inventory have raised estimates for each 2025 and 2026 over the previous 30 days. Thus, the Zacks Consensus Estimate for 2025 and 2026 earnings has moved north 0.4% and 0.3%, respectively, over the previous 30 days.

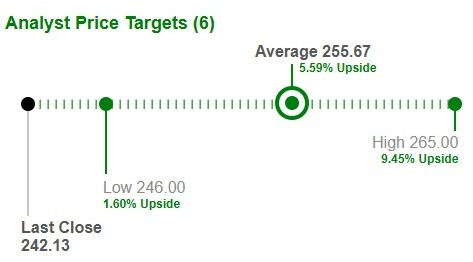

Common Goal Worth for AIZ Suggests Upside

Primarily based on short-term value targets supplied by six analysts, the Zacks common value goal is $255.67 per share. The common suggests a possible 5.5% upside from the final closing value.

Picture Supply: Zacks Funding Analysis

Assurant’s Favorable Return on Capital

Return on fairness within the trailing 12 months was 18.6%, higher than the trade common of 15%. This highlights the corporate’s effectivity in using shareholders’ funds.

Additionally, the return on invested capital (ROIC) has been growing over the previous few quarters as the corporate raised its capital funding over the identical timeframe, reflecting AIZ’s effectivity in using funds to generate earnings. ROIC within the trailing 12 months was 12.2%, higher than the trade common of two%.

Key Factors to Word for AIZ

Assurant’s deal with rising fee-based, capital-light companies, which account for 52% of segmental revenues, bodes nicely for progress. Administration estimates that the contribution from the identical will proceed to develop in double digits over the long run.

Inside Linked Residing, AIZ continues to assist long-term progress by way of the event of progressive choices for companions. U.S. Linked Residing is poised for strong progress, significantly throughout the cell safety enterprise, driving on progressive choices, buyer expertise experience and improved relationships with cell carriers and cable operators.

Owners’ top-line progress, extra favorable loss expertise from prior-period improvement on claims, progress in insurance policies in-force and better common premiums inside lender-placed, in addition to progress throughout numerous specialty merchandise, ought to drive higher outcomes at International Housing. For 2025, AIZ expects International Housing adjusted EBITDA, excluding reportable catastrophes, to ship robust progress.

International Way of life progress is anticipated to be pushed by Linked Residing, supported by progress in international cell system safety and a brand new monetary providers program, together with inorganic and natural progress methods. For 2025, International Way of life adjusted EBITDA is projected to extend from progress in Linked Residing and International Automotive.

The insurer stays targeted on ramping up the Linked Residing platform, deploying progressive services, and including new partnerships. These initiatives are anticipated to double the margins of Linked Residing to eight% over the long run.

Wealth Distribution

Assurant has a strong capital administration coverage. It expects to deploy capital to fund investments, mergers and acquisitions. In November 2024, the board permitted a dividend hike of 11%, which is the twentieth consecutive yr of improve. As of Sept. 30, 2025, $168.3 million in combination value at buy remained unused below the repurchase authorization.

For 2025, AIZ expects to return $300 million to shareholders by way of share repurchases, on the high finish of the $200 million to $300 million anticipated vary from the start of the yr. For the fourth quarter of 2025, AIZ expects the next stage of section dividends given the enterprise’s means to generate significant money flows.

Closing Tackle AIZ

Deal with capital-light companies, Owners progress and Linked Residing progress throughout the cell safety enterprise ought to favor Assurant’s outcomes. Increased return on capital, favorable progress estimates and engaging valuations ought to proceed to profit the insurer over the long run.

Coupled with a formidable dividend historical past, strong progress projections, favorable ROE and optimistic analyst sentiment, the time seems proper for potential buyers to wager on this Zacks Rank #2 (Purchase) insurer. You possibly can see the whole checklist of at present’s Zacks #1 Rank (Sturdy Purchase) shares right here.

Assurant additionally has a VGM Rating of A. Shares with a positive VGM Rating are these with probably the most engaging worth, greatest progress and most promising momentum in contrast with friends. Its spectacular dividend historical past in addition to engaging valuations are different positives. Again-tested outcomes present that shares with a VGM Rating of A or B, when mixed with a Zacks Rank #1 or 2, provide the perfect alternatives within the worth investing area.

Quantum Computing Shares Set To Soar

Synthetic intelligence has already reshaped the funding panorama, and its convergence with quantum computing might result in probably the most important wealth-building alternatives of our time.

At the moment, you have got an opportunity to place your portfolio on the forefront of this technological revolution. In our pressing particular report, Past AI: The Quantum Leap in Computing Energy, you will uncover the little-known shares we imagine will win the quantum computing race and ship huge positive factors to early buyers.

The Vacationers Firms, Inc. (TRV) : Free Inventory Evaluation Report

Cincinnati Monetary Company (CINF) : Free Inventory Evaluation Report

Assurant, Inc. (AIZ) : Free Inventory Evaluation Report

NMI Holdings Inc (NMIH) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.