Oracle’s ORCL relationship with OpenAI has develop into a unending supply of market angst, because the tie-in reminds a lot of questionable vendor-financing practices from the late Nineties. Tied to Oracle’s OpenAI publicity are questions in regards to the firm’s monetary well being and its capacity to fund its information heart growth plans.

The December 10th quarterly launch, which was, at greatest, combined, added to Oracle’s woes. Oracle missed consensus income and margin expectations and raised its capital expenditure (capex) outlook. The inventory’s unfavorable response to this quarterly launch contrasted with the prior quarterly launch in early September, when the inventory jumped by greater than a 3rd.

When buyers usually consider the large Tech gamers, like Microsoft MSFT or Alphabet GOOGL and even Oracle, they instinctively assume fortress stability sheets and ungodly quantities of working money flows. These assumptions are misplaced within the case of Oracle, because it has been relying currently on the debt markets to fund its ever-rising information heart buildout-related capital expenditures.

Oracle’s capex outlay totaled $21.2 billion in fiscal yr 2025 (FY ends in Might), up from $6.7 billion in FY 2024. The corporate generated $20.8 billion of free money move in FY 2025, that means it was free money move unfavorable for the yr. The expectation for the present yr (FY 2026) is that Oracle’s $50 billion capex finances is roughly double the quantity of working money flows it’s anticipated to generate. In truth, Oracle will most probably be free money move unfavorable in fiscal yr 2027 as effectively, which signifies that it might want to faucet the debt market to fund its capex finances.

The chart under gives an summary of Oracle’s debt load and the comparable measure for Microsoft. Lengthy-term debt as a share of the corporate’s whole capital is just not the one, nor even one of the best, measure of balance-sheet leverage, however it’s a easy and simply understood indicator of monetary flexibility.

Picture Supply: Zacks Funding Analysis

We should always remember the fact that Oracle isn’t in any monetary misery, because it at present has an ‘funding grade’ credit standing from the score businesses. That mentioned, its credit standing of BBB (from S&P) is the bottom rung of investment-grade credit standing.

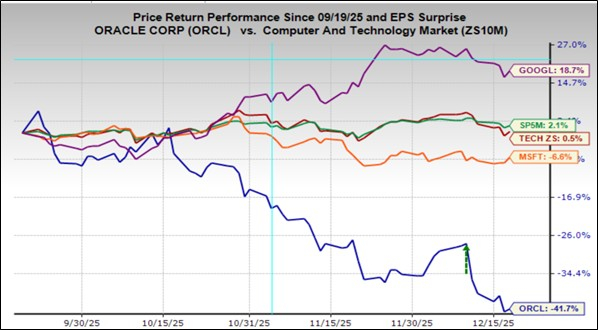

We’re all aware of the market’s issues in regards to the broader ‘AI commerce’, which ranges from the ‘bubble narrative’ at one excessive to affordable questions in regards to the monetization of AI investments on the different.

The chart under exhibits the three-month efficiency of Oracle shares relative to Alphabet, Microsoft, the Zacks Tech sector, and the S&P 500 index.

Picture Supply: Zacks Funding Analysis

The continuing points in Oracle shares should not a mirrored image of these AI issues, because the chart above clearly exhibits, however relatively a operate of the aforementioned OpenAI publicity and issues about its monetary well being. We might have seen way more solidarity from Microsoft and Alphabet with Oracle within the above interval had the overriding concern been the ‘AI commerce’.

One key efficiency metric that took heart stage within the Oracle story is Remaining Efficiency Obligations (RPO), which reached $523 billion this quarter, up $455 billion from the previous quarter. For reference, the comparable quantity for Microsoft reached $392 billion within the firm’s newest quarterly report.

Consider this key efficiency metric as Oracle’s backlog or future revenues had jumped by an eye-popping $317 billion within the previous quarter. The bearish narrative on Oracle notes that $300 billion of the previous quarter’s $317 billion RPO development was attributable to OpenAI.

It’s this elevated stage of buyer focus threat, coupled with Oracle’s comparatively stretched monetary well being, that has been weighing on the inventory currently.

A good evaluation of the evolving Oracle story is that whereas there’s undoubtedly extra uncertainty and threat related to its RPO (or backlog) getting transformed into future revenues, notably say relative to Microsoft or Alphabet, it’s however a key factor of the corporate’s development profile and its standing as a important participant within the rising AI world.

In different phrases, nobody needs to be below the impression that this can be a second coming of Enron or different such doubtful characters from our collective previous.

The chart under gives a 10-year comparability of Oracle valuation relative to Microsoft, utilizing the ahead 12-month P/E a number of. As you’ll be able to see right here, Oracle shares broke away from their traditionally discounted valuation to Microsoft solely in Might 2025, however have now reversed all of these positive factors.

Picture Supply: Zacks Funding Analysis

This 10-year historical past exhibits that Oracle shares have commanded as excessive as 66% premium (September 2025) to Microsoft share to a 55% low cost (November 2020), with a 10-year median of 28% low cost. The inventory is at present buying and selling at an 18% low cost to Microsoft shares (23.6X for Oracle vs. 28.7X for Microsoft).

The decrease low cost relative to historical past is sensible when seen within the context of Oracle’s rising standing as a key participant within the rising AI world. Oracle bulls would seemingly argue that there isn’t a justification for the ‘new Oracle’ to commerce at a reduction to Microsoft going ahead, however its stability sheet vulnerability.

Tech Earnings Outlook

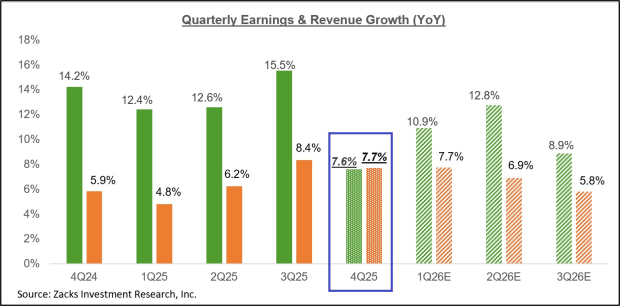

The chart under exhibits the earnings and income development outlook for the Zacks Tech sector on a quarterly foundation, the place we spotlight expectations for 2025 This fall within the context of what the sector achieved within the previous two quarters and what’s anticipated within the following three quarters.

Picture Supply: Zacks Funding Analysis

The Tech sector has been important to driving mixture earnings development for the final 9 quarters (since 2023 Q3), and the above chart exhibits that it’s anticipated to proceed enjoying that function within the coming durations as effectively.

Please notice that the Tech sector has been persistently having fun with optimistic estimate revisions over the previous yr, and we noticed the identical pattern at play for the reason that begin of 2025 This fall in October. In truth, had it not been for optimistic revisions to Tech sector estimates, mixture This fall earnings estimates for the S&P 500 index can be modestly down for the reason that begin of October.

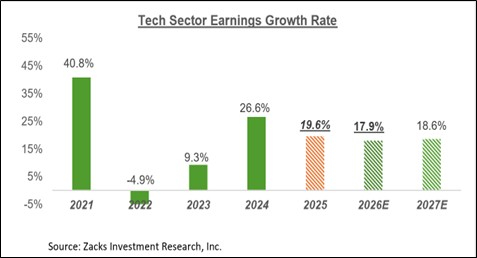

The chart under exhibits the sector’s earnings development image on an annual foundation.

Picture Supply: Zacks Funding Analysis

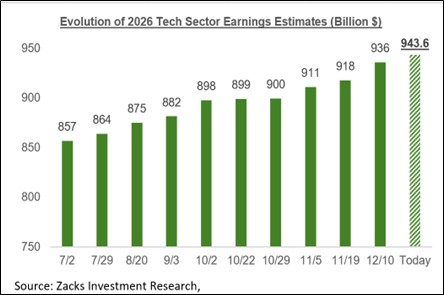

The optimistic revisions pattern that we referenced for the Tech sector within the context of 2025 This fall earnings estimates could be very a lot in place for full-year 2026 estimates as effectively, because the chart under exhibits.

Picture Supply: Zacks Funding Analysis

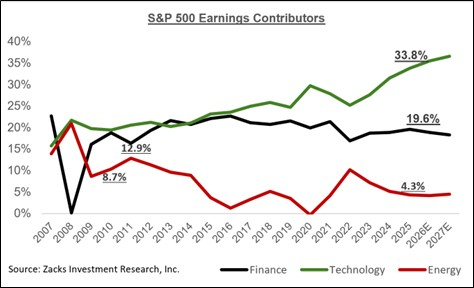

The Tech sector is just not unusual; it accounts for almost a 3rd of S&P 500 earnings, because the chart under exhibits.

Picture Supply: Zacks Funding Analysis

Earnings Outlook for the Magazine 7

The Magazine 7 group is mostly seen as mega-cap Tech gamers. Nonetheless, within the Zacks sector classification system, two of the Magazine 7 gamers should not a part of the Zacks Tech sector; we place Amazon within the Zacks Retail sector and Tesla within the Zacks Auto sector. Each of those sectors are Zacks improvements, because the ‘official’ Customary & Poor’s business classification doesn’t have stand-alone sectors for the retail and auto areas.

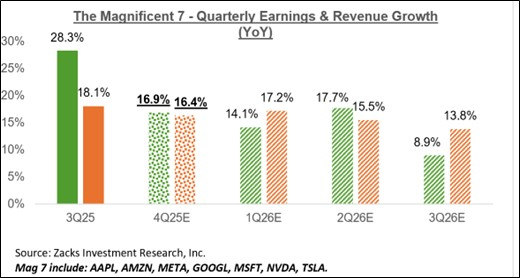

For 2025 This fall, the Magazine 7 group is anticipated to supply +16.9% earnings development on +16.4% larger revenues, because the chart under exhibits.

Picture Supply: Zacks Funding Analysis

The chart under exhibits the Magazine 7 group’s earnings and income development image on an annual foundation.

Picture Supply: Zacks Funding Analysis

As you’ll be able to see above, the group’s 2026 earnings are at present anticipated to be up +16.6%, adopted by +18% in 2027.

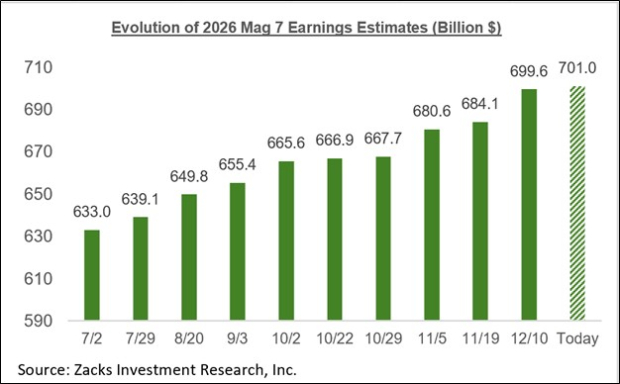

The vital issue to remember is that the Magazine 7 earnings outlook is steadily enhancing, because the chart under exhibits.

Picture Supply: Zacks Funding Analysis

Please notice that the Magazine 7 group is on observe to usher in 26.4% of all S&P 500 earnings in 2026, up from 23.2% of the whole in 2024 and 11.7% in 2019. Relating to market capitalization, the Magazine 7 group at present carries a 34.6% weight within the index.

2025 This fall Earnings Season Scorecard

Final week’s Oracle earnings report was for the corporate’s fiscal quarter ending in November, which we and different analysis organizations depend as a part of the December-quarter tally. Oracle is hardly alone on this respect, and quarterly outcomes from the likes of FedEx, Nike, Adobe, and others fall in the identical class. Via Friday, December 19th, now we have seen such This fall outcomes from 18 S&P 500 members.

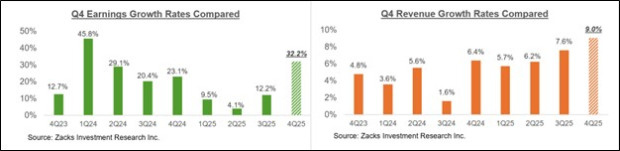

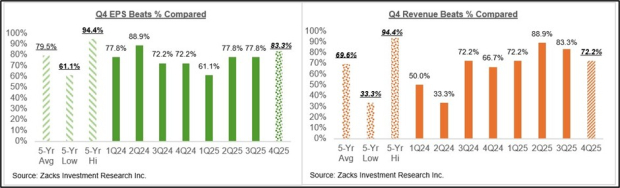

Complete earnings for these 18 index members are up +32.2% from the identical interval final yr on +9% larger revenues, with 83.3% beating EPS estimates and 72.2% beating income estimates.

The comparability charts under put the This fall earnings and income development charges from these firms in a historic context.

Picture Supply: Zacks Funding Analysis

The comparability charts under present the This fall EPS and income beats percentages in a historic context.

Picture Supply: Zacks Funding Analysis

The Earnings Large Image

The chart under exhibits present This fall earnings and income development expectations for the S&P 500 index within the context of the previous 4 quarters and the approaching three quarters.

Picture Supply: Zacks Funding Analysis

The chart under exhibits the general earnings image on a calendar-year foundation.

Picture Supply: Zacks Funding Analysis

For an in depth view of the evolving earnings image, please try our weekly Earnings Tendencies report right here >>>>This fall Earnings: Tech Anticipated to Stay Progress Driver

Zacks’ Analysis Chief Picks Inventory Most Prone to “At Least Double”

Our specialists have revealed their High 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. In fact, all our picks aren’t winners however this one might far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our High Inventory to Double (Plus 4 Runners Up) >>

Microsoft Company (MSFT) : Free Inventory Evaluation Report

Oracle Company (ORCL) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.