Lamb Weston Holdings, Inc. (LW) reported stable second-quarter fiscal 2026 outcomes, whereby each prime and backside traces beat the Zacks Consensus Estimate. Whereas web gross sales elevated, earnings decreased from the year-ago interval’s actuals.

LW’s adjusted earnings had been 69 cents per share, beating the Zacks Consensus Estimate of 67 cents. The lower of 5% was on account of lowered adjusted gross revenue, partially offset by decreased adjusted promoting, normal and administrative (SG&A).

Lamb Weston Worth, Consensus and EPS Shock

Lamb Weston price-consensus-eps-surprise-chart | Lamb Weston Quote

Web gross sales amounted to $1,618.1 million, beating the Zacks Consensus Estimate of $1,593 million. The highest line elevated $17.2 million 12 months over 12 months.

LW’s Quarterly Outcomes: Key Metrics & Insights

On a constant-currency foundation, gross sales had been flat, as stable 8% quantity development was outweighed by an 8% drop in value/combine. Quantity development was pushed by buyer wins, share good points and retention, notably in North America and Asia. The lower in value/combine displays continued buyer assist by means of pricing and commerce actions, together with the carryover impression of fiscal 2025 pricing, inside a extremely competitiveglobal marketenvironment. Our mannequin steered a quantity enhance of 5.3% within the quarter.

Adjusted gross revenue fell $15.6 million from the prior 12 months, touchdown at $327.9 million, with weaker value/combine serving as the primary drag. We anticipated adjusted gross margin contraction of 100 bps.

Adjusted SG&A bills fell $7.8 million 12 months over 12 months, totaling $145.1 million, supported by cost-savings measures, partially offset by increased compensation and advantages accruals.

Adjusted EBITDA decreased $8.5 million 12 months over 12 months, reaching $285.7 million. This decline was on account of lowered adjusted gross revenue and fairness technique funding earnings, partially offset by decrease adjusted SG&A.

LW Supplies Q2 Insights by Section

Web gross sales for the North America section, which covers prospects in the USA, Canada and Mexico, had been flat, reaching $1,069.5 million in contrast with the prior-year quarter. Quantity rose 8%, pushed by current buyer contract wins, share good points and broad-based development throughout channels.

The value/mixture of the section fell 8%, reflecting the carryover impression of fiscal 2025 value investments, ongoing buyer assist by means of value and commerce, and unfavorable channel combine.

The North America section’s adjusted EBITDA elevated by $18.6 million to $287.8 million. The rise was pushed by elevated volumes, lowered manufacturing prices per pound and adjusted SG&A, reflecting advantages from price financial savings measures and improved working efficiencies. These advantages had been partially offset by continued value and commerce assist for purchasers.

Web gross sales for the Worldwide section, which incorporates all prospects exterior North America, grew 4% to $548.6 million, together with a positive $22.6 million from international forex translation. At fixed forex, web gross sales decreased 1%. Quantity grew 7%, pushed by energy in Asia and with multinational chain prospects.

The value/mixture of the section declined 8% on account of continued pricing and commerce actions to assist prospects in a aggressive market setting, in addition to an unfavorable combine.

Worldwide section adjusted EBITDA decreased by $21.4 million to $27.2 million. The lower was primarily attributable to elevated manufacturing prices per pound, together with elevated mounted manufacturing unit burden on account of decrease utilization of worldwide manufacturing amenities and start-up prices related to the brand new manufacturing facility in Argentina. These increased prices had been partially offset by advantages from price financial savings measures and elevated gross sales volumes.

Lamb Weston’s Monetary Well being Snapshot

The corporate ended the quarter with money and money equivalents of $82.7 million, long-term debt and financing obligations (excluding the present portion) of $3,648.9 million and complete shareholders’ fairness of $1,754.4 million.

The corporate generated $530.4 million as web money from working actions for the 26 weeks ending Nov. 23, 2025, whereby capital expenditures amounted to $155.7 million.

Within the second quarter of fiscal 2026, Lamb Weston returned $51.6 million to its shareholders by means of money dividends and repurchased $39.6 million of widespread inventory below the share repurchase program, representing 617,623 shares. Roughly $308 million stays licensed and obtainable for repurchases below this system.

On Dec. 17, 2025, administration authorized a 3% enhance within the quarterly dividend, elevating the dividend to 38 cents per share. The dividend is payable on Feb. 27, 2026, to its shareholders of file as of the shut of enterprise on Jan. 30.

What to Anticipate From LW in FY26?

The corporate nonetheless expects web gross sales at fixed forex within the vary of $6.35 billion to $6.55 billion and adjusted EBITDA of $1.00 billion to $1.20 billion. Capital expenditures are anticipated to complete roughly $500 million.

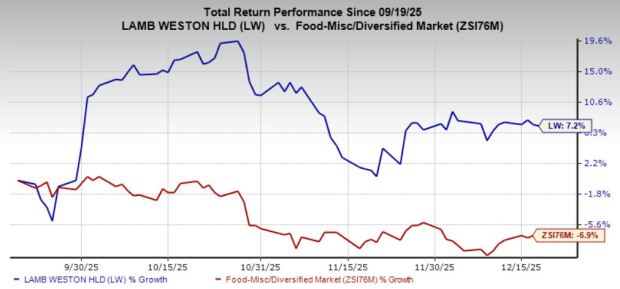

LW’s Share Worth Efficiency

Shares of this Zacks Rank #4 (Promote) firm have gained 7.2% up to now three months in opposition to the business’s 6.9% decline.

Picture Supply: Zacks Funding Analysis

Shares to Take into account

United Pure Meals, Inc. (UNFI) distributes pure, natural, specialty, produce and traditional grocery and non-food merchandise in the USA and Canada. At current, United Pure flaunts a Zacks Rank of 1 (Sturdy Purchase). You may see the whole record of at this time’s Zacks #1 Rank shares right here.

The consensus estimate for United Pure’s present fiscal-year gross sales and earnings implies development of 1% and 187.3%, respectively, from the year-ago figures. UNFI delivered a trailing four-quarter earnings shock of 52.1%, on common.

Village Farms Worldwide, Inc. (VFF) produces, markets and distributes greenhouse-grown tomatoes, bell peppers, cucumbers and mini-cukes in North America. It sports activities a Zacks Rank #1. Village Farms delivered a trailing four-quarter earnings shock of 155.6%, on common.

The Zacks Consensus Estimate for Village Farms’ present fiscal-year earnings signifies development of 165.6% from the prior-year ranges.

The Vita Coco Firm, Inc. (COCO) develops, markets and distributes coconut water merchandise below the Vita Coco model identify. COCO at present flaunts a Zacks Rank #1. Vita Coco delivered a trailing four-quarter earnings shock of 30.4%, on common.

The Zacks Consensus Estimate for Vita Coco’s present fiscal-year gross sales and earnings implies development of 18% and 15%, respectively, from the year-ago figures.

Zacks’ Analysis Chief Picks Inventory Most Prone to “At Least Double”

Our specialists have revealed their High 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. In fact, all our picks aren’t winners however this one may far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our High Inventory to Double (Plus 4 Runners Up) >>

Vita Coco Firm, Inc. (COCO) : Free Inventory Evaluation Report

United Pure Meals, Inc. (UNFI) : Free Inventory Evaluation Report

Lamb Weston (LW) : Free Inventory Evaluation Report

Village Farms Worldwide, Inc. (VFF) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.

the S&P 500 name")