S&P 500 took a dive 75min earlier than the opening bell, retail enthusiastically purchased into PCE and UoM knowledge launch, and costs then settled little modified on the pre-flush stage. What‘s obvious from checking the hourly on each ES and NDX this week? A collection of upper highs and better lows – outstanding resilience in per week that began with BTC selloff early Monday.

Friday was a nasty day for crypto too, but Nasdaq held significantly higher as soon as once more. Magazine 7 shares are appearing much less uniform as a bunch, and the yearly winners (NVDA and earlier mentioned GOOGL) clearly present up – I might spotlight additional mentioned banking sectors too.

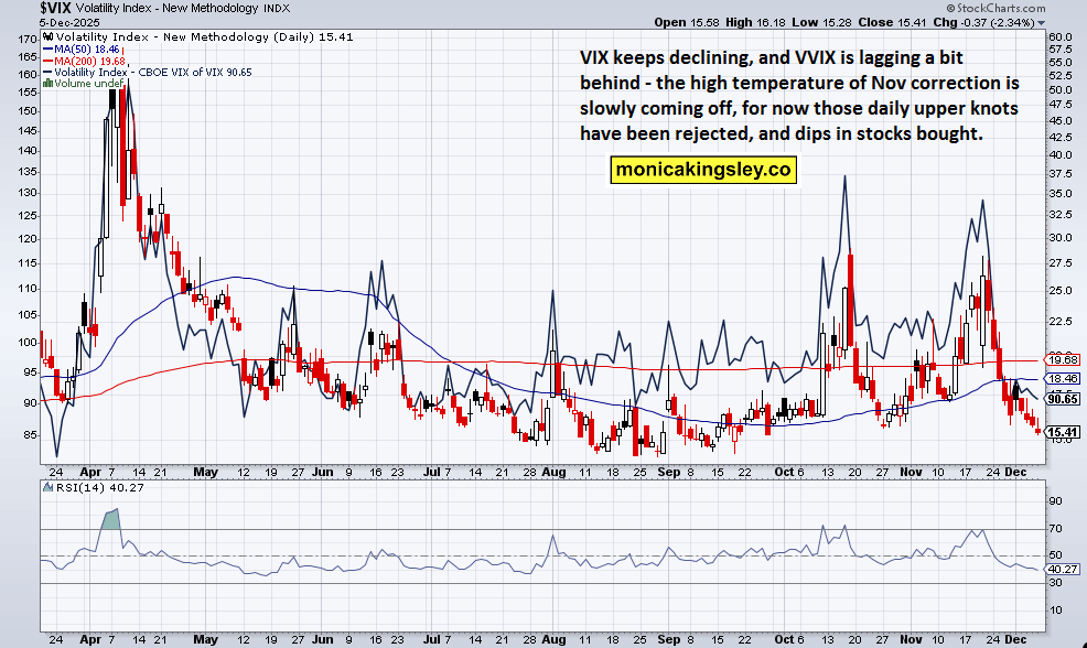

With the standard Santa Claus rally expectation, we should ask whether or not there may be adequate breadth available in the market to assist such a feat – and whether or not Powell subsequent week giving us a broadly anticipated hawkish minimize, can be sufficient for shares to go on… have a look at ORCL and AVGO earnings too.

Friday‘s dynamic to spotlight is the poor knowledge expectation, so readily purchased, and when the information got here, they weren‘t almost sufficient that unhealthy to sink the 500-strong index.

Look additionally at retailers‘ efficiency, try additionally DG, and UoM knowledge – with main indicators for companies being higher than for manufacturing, that tells us as a lot as there may be to say about that recession threat… or for the „contagion“ of rising Japanese yields that have been unable to sink Nikkei, not to mention shares around the globe… nuff mentioned.