Lithium Americas Corp. LAC and Albemarle Company ALB each interact in exploration, growth, mining, processing and manufacturing of lithium. Albemarle can be a number one producer of highly-engineered specialty chemical compounds geared to satisfy buyer necessities throughout a broad vary of finish markets, together with petroleum refining, client electronics, power storage, building and automotive.

12 months up to now, Lithium Americas shares have risen 77.4%, and Albemarle shares have surged 47.6%. Let’s dig deeper into the basics of each firms to find their strengths and weaknesses.

12 months-to-Date Value Efficiency

Picture Supply: Zacks Funding Analysis

The Case for Lithium Americas Inventory

Lithium Americas is creating the Thacker Move lithium mine in northern Nevada, house to the world’s largest identified measured lithium useful resource and reserve. The undertaking is operated by way of a three way partnership wherein Lithium Americas holds a 62% stake and serves as undertaking supervisor, whereas Basic Motors Firm GM owns the remaining 38%. The corporate is working to convey Section 1 of Thacker Move into manufacturing and is aiming for a deliberate output of 40,000 tons per yr of battery-grade lithium carbonate.

Building on the Thacker Move undertaking is transferring ahead. The corporate expects to complete mechanical building of the Section 1 processing plant by late 2027. Engineering work was greater than 80% full as of Sept. 30, 2025, and is on monitor to exceed 90% by the tip of the yr. Finishing detailed engineering early helps scale back dangers associated to the undertaking’s schedule and finances.

The corporate has additionally signed buy agreements for key long-lead gear, infrastructure and providers wanted to construct the processing plant, in addition to for growth and mining actions at Thacker Move. As of Sept. 30, 2025, about $430 million was already dedicated.

Nevertheless, Lithium Americas has but to generate revenues from operations and depends on fairness and different financings to fund operations. LAC’s omnibus waiver, consent and modification (OWCA) mortgage settlement can restrict its operational flexibility, constrain strategic choices and pressure actions unfavorable for shareholders. Whereas the OWCA enabled the primary $435 million DOE mortgage advance, issuing required warrants and assembly ongoing circumstances launched monetary, accounting and tax uncertainties.

Future mortgage attracts rely on strict compliance with DOE necessities, and any failure may scale back accessible funding or set off defaults, which may pressure instant reimbursement and jeopardize the Thacker Move undertaking. Declining earnings estimates additionally solid a pall on the corporate’s prospects.

The Case for Albemarle Inventory

Albemarle is strategically executing its tasks geared toward boosting its world lithium conversion capability. It stays centered on investing in high-return tasks to drive productiveness. Wholesome buyer demand, capability enlargement and plant productiveness enhancements are supporting its volumes.

ALB noticed larger gross sales volumes in its Power Storage unit within the third quarter of 2025 on document manufacturing from its built-in conversion services. The Salar yield enchancment undertaking in Chile has achieved a 50% working price. The ramp-up on the Meishan lithium conversion facility in China can be progressing forward of schedule.

Furthermore, Albemarle is taking aggressive cost-saving and productiveness actions within the wake of tumbling lithium costs. The corporate expects to ship roughly $450 million in value and productiveness enhancements in 2025, having surpassed its preliminary goal of $300-$400 million. ALB is taking actions to keep up its aggressive place, together with the initiation of a complete assessment of value and working construction, optimization of the conversion community and discount of capital expenditure. It has lowered the full-year 2025 capital expenditures outlook to round $600 million.

Albemarle stays dedicated to driving shareholder worth by leveraging wholesome money flows and powerful liquidity. On the finish of the third quarter of 2025, ALB had liquidity of round $3.5 billion, together with money and money equivalents of round $1.9 billion. Its working money move was round $893.8 million for the primary 9 months of 2025, up 29% from the prior-year interval. ALB expects to generate free money move of $300-$400 million in 2025, pushed by robust money conversion, decrease capital spending and productiveness measures.

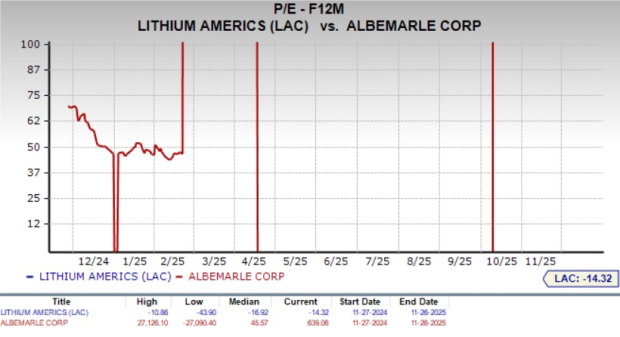

Valuation of LAC & ALB

From a valuation standpoint, Lithium Americas is buying and selling at a ahead price-to-earnings (P/E) of damaging 14.32X, nearer to its imply of damaging 16.52X over the past 5 years. ALB is buying and selling at a ahead P/E of 639.06X.

Picture Supply: Zacks Funding Analysis

How Do Zacks Estimates Examine for LAC & ALB?

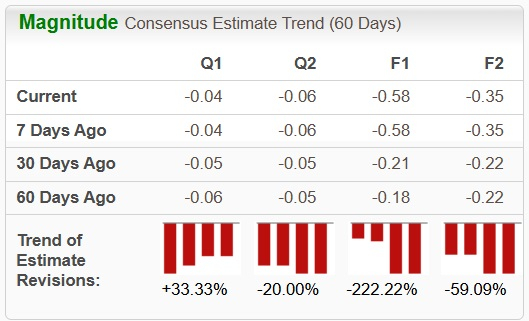

The Zacks Consensus Estimate for LAC’s 2025 EPS implies a year-over-year decline of 176.2%. The consensus estimate for loss for 2025 and 2026 has widened over the previous 30 days.

Picture Supply: Zacks Funding Analysis

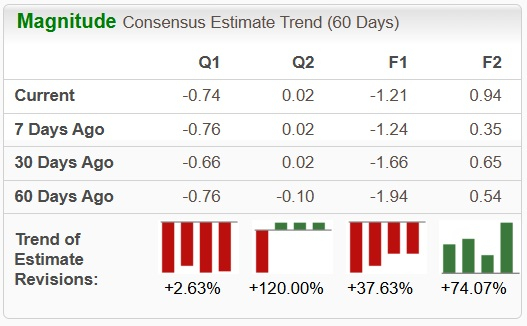

The Zacks Consensus Estimate for ALB’s 2025 EPS implies year-over-year progress of 48.3%. The loss per share estimates for 2025 have been narrowed over the previous 30 days, whereas the EPS estimates for 2026 have elevated.

Picture Supply: Zacks Funding Analysis

Conclusion

Whereas Lithium Americas holds a promising long-term asset in Thacker Move, the undertaking stays years away from manufacturing and continues to face funding, regulatory and execution dangers. The corporate remains to be pre-revenue, depending on exterior financing and constrained by mortgage circumstances that might restrict flexibility or jeopardize progress if unmet. The corporate has a damaging EPS progress projection and widening loss estimates for 2025.

Quite the opposite, Albemarle is already a worldwide chief in lithium and specialty chemical compounds, supported by established operations, rising manufacturing volumes and a diversified income base. Its strategic capability expansions, aggressive cost-saving initiatives and stronger liquidity place present resilience amid risky lithium costs. Albemarle can be producing substantial working and free money flows and reinvesting them in progress whereas sustaining shareholder worth. Its EPS estimates for 2025 recommend year-over-year progress.

Albemarle emerges because the stronger inventory relative to Lithium Americas as a result of it combines operational maturity with monetary stability, benefits that LAC has but to develop.

LAC & ALB each carry a Zacks Rank #3 (Maintain). You’ll be able to see the entire record of at the moment’s Zacks #1 Rank (Robust Purchase) shares right here.

Quantum Computing Shares Set To Soar

Synthetic intelligence has already reshaped the funding panorama, and its convergence with quantum computing may result in essentially the most important wealth-building alternatives of our time.

As we speak, you’ve gotten an opportunity to place your portfolio on the forefront of this technological revolution. In our pressing particular report, Past AI: The Quantum Leap in Computing Energy, you may uncover the little-known shares we imagine will win the quantum computing race and ship huge good points to early traders.

Basic Motors Firm (GM) : Free Inventory Evaluation Report

Albemarle Company (ALB) : Free Inventory Evaluation Report

Lithium Americas Corp. (LAC) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.